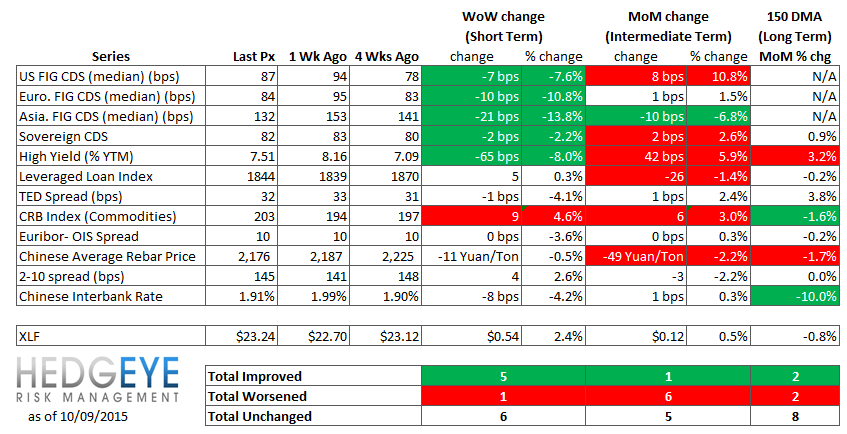

Key Takeaway:

The focus seemed to shift last week from the negatives of the U.S. jobs report the week prior to the positive effects from ongoing accommodative central bank policy. In other words, bad news once again became good news. With the Federal Reserve holding interest rates steady, CDS spreads tightened globally and the High Yield YTM fell -65 bps to 7.5%. Short-term readings in our heatmap below are mostly green. However, the intermediate term is the opposite with mostly negative warning signals, and long-term measures are mixed.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 5 of 12 improved / 1 out of 12 worsened / 6 of 12 unchanged

• Intermediate-term(WoW): Negative / 1 of 12 improved / 6 out of 12 worsened / 5 of 12 unchanged

• Long-term(WoW): Negative / 2 of 12 improved / 2 out of 12 worsened / 8 of 12 unchanged

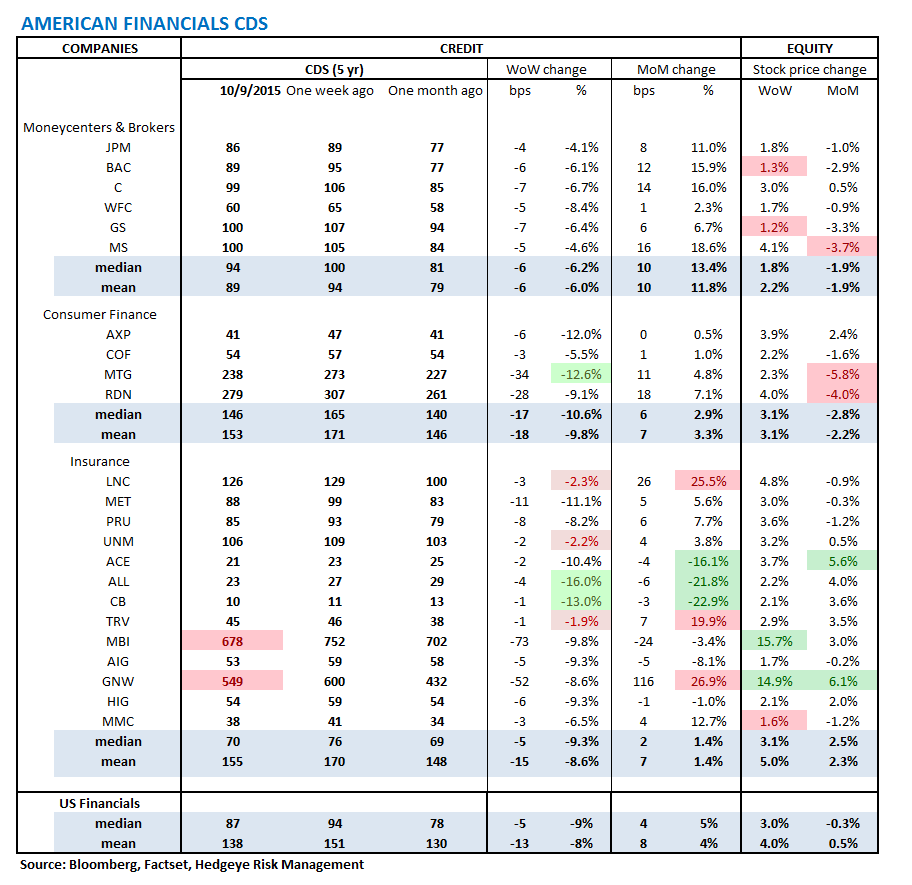

1. U.S. Financial CDS – Swaps tightened for 24 out of 27 domestic financial institutions. With the Federal Reserve holding interest rates steady at its September policy meeting, insurance against default for domestic financial institutions got cheaper; the median CDS spread tightened from 94 bps to 87 bps.

Tightened the most WoW: ALL, CB, MTG

Widened the most/ tightened the least WoW: SLM, SLM, SLM

Tightened the most WoW: CB, ALL, ACE

Widened the most MoM: GNW, LNC, TRV

2. European Financial CDS – Swaps mostly tightened among European financials last week, likely following the U.S.'s lead after Federal Reserve minutes showed rates being held steady for now.

3. Asian Financial CDS – Investors looked favorably on central bank policy last week with CDS spreads in Asia tightening, likely in reaction to both the U.S. Federal Reserve holding rates steady and a top Chinese central banker stating that the PBOC would allow the yuan exchange rate to be more flexible. In the past, China allowing its currency to depreciate has stirred fears of slowing economic growth; however, the focus last week seemed to be more on the positive effects of accommodative monetary policy.

4. Sovereign CDS – Sovereign swaps were flat to tighter on the week. Spanish sovereign swaps tightened the most, by -5 bps to 103.

5. Emerging Market Sovereign CDS – With commodity prices rising last week, emerging market swaps tightened across the board. Russian swaps tightened the most, by -51 bps to 320, followed by Turkish swaps, which tightened by -48 bps to 266.

6. High Yield (YTM) Monitor – High Yield rates fell 65 bps last week, ending the week at 7.51% versus 8.16% the prior week.

7. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 5.0 points last week, ending at 1844.

8. TED Spread Monitor – The TED spread fell 1 basis point last week, ending the week at 32 bps this week versus last week’s print of 33 bps.

9. CRB Commodity Price Index – The CRB index rose 4.6%, ending the week at 203 versus 194 the prior week. As compared with the prior month, commodity prices have increased 3.0%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was unchanged at 10 bps.

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index fell 8 basis points last week, ending the week at 1.91% versus last week’s print of 1.99%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

12. Chinese Steel – Steel prices in China fell 0.5% last week, or 11 yuan/ton, to 2176 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread widened to 145 bps, 4 bps wider than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

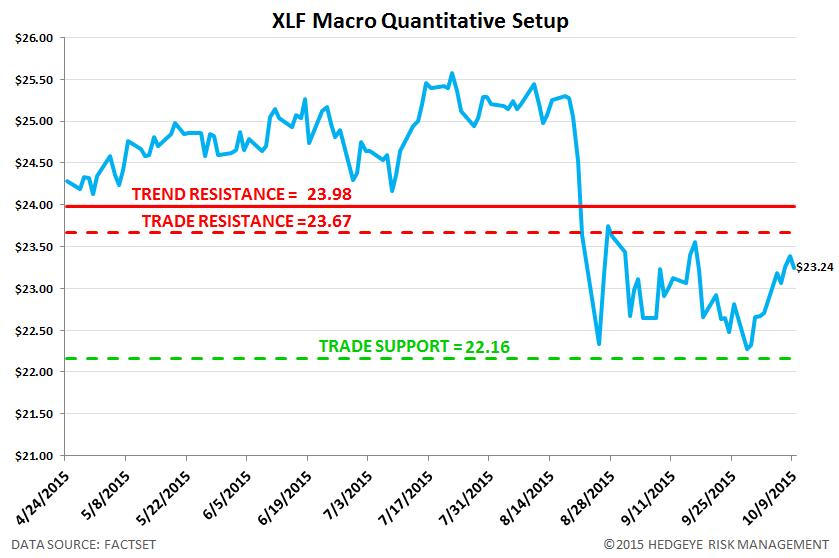

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 1.9% upside to TRADE resistance and 4.6% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT