TICKERS: AWAY, CCL, NCLH, UBER

EVENTS

- Oct 8: Hedgeye Macau call 2:30pm

COMPANY NEWS

AWAY- HomeAway announced the acquisition of vacation rental startup Dwellable. Terms of the deal were not disclosed, but CEO Kirby Winfield said it was a positive outcome for investors. Dwellable raised just $2 million in funding — a pittance compared to other heavily-funded competitors in the online vacation rental arena.

CCL - Australia's P&O and Princess ships are set to be reshuffled to meet increased demand for local holidays at sea, Carnival Australia announced yesterday. Princess Cruises' 2,000-passenger Dawn Princess will move to the P&O fleet in May 2017, while Golden Princess will remain in Australian waters throughout 2017 (instead of returning to Japan) alongside Sun Princess and Sea Princess.

NCLH - Oceania Cruises will be offering 60 new itineraries across six continents for 2016/2017. Never-before-sailed ports of call for the line include Burnie, Tasmania; Ensenada, Mexico; Port Moresby, Papua New Guinea; and Harvest Caye, Belize. Sirena will debut in April and take on Mediterranean Itineraries before heading to the Caribbean and Pacific for the winter.

UBER - Uber is setting up shop in the Shanghai Experimental Free Trade Zone by incorporating a company called Shanghai Wubo Information Technology with registered capital of RMB2.1 billion (approx: $33 million). The company also announced it would invest up to RMB6.3 billion (approx: $991 million) to maintain its long-term and sustained development in China and is now preparing to apply to become a fully-licensed car-hire platform.

INDUSTRY NEWS

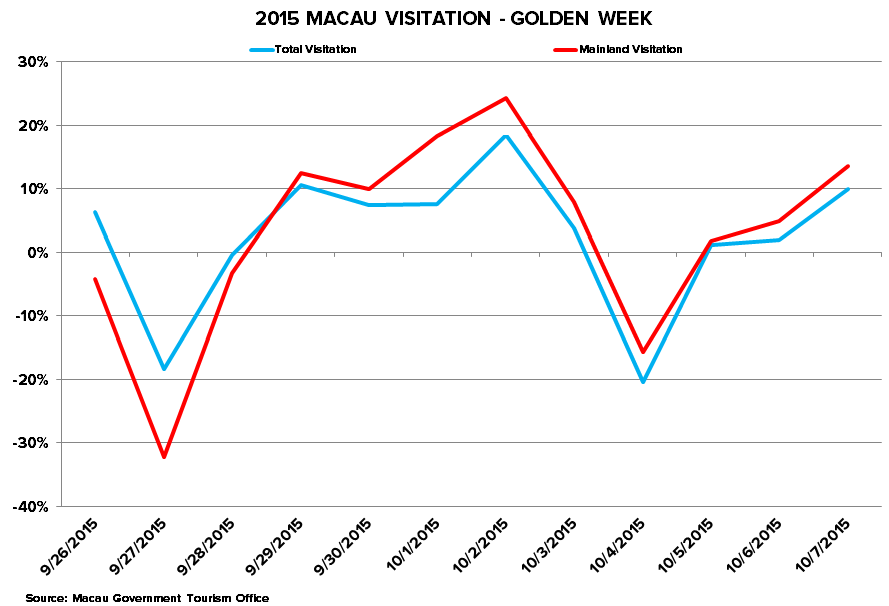

Golden Week Update- In the first six days of the National Day golden week of holidays in the mainland, Macau had 938,197 visitors, the Macau Government Tourist Office says. The office says mainlanders made up 85.2% of the visitors.

The total number of visitors was 8% higher than in the equivalent period last year and the number of mainlanders visiting was 6.3% higher.

Takeaway: Month to date GGR is still down YoY but we think the numbers will look much better than trend when we get them next week.

REGIONAL REVENUES (SEPT):

- Illinois SS GGR: -5.4% YoY

- PENN SS GGR: +0.6% YoY

- Ohio SS GGR: +5.3% YoY

- PENN SS GGR: +10.0% YoY

Takeaway: IL was a bit of a disappointment but the other states have come in strong, as we expected. PENN crushed it in its most important state (Ohio) and held up better than most in IL.