In short, the economy is slowing; the ag commodity complex prices are crashing; the herd is fat and growing and consumers are consuming less red meat. Therefore, the current set up for a crash in red meat is nearly perfect:

- Because beef is among the most expensive proteins.

- The strong dollar is hurting the export market for beef.

- U.S. per-capita beef consumption in 2015 will decline to 53.9 pounds per person, the lowest in government data that goes back to 1970.

- Cattle futures are in a free fall and could crash further and stay low for an extended period of time. As a result, the bubble in red meat prices are going to burst, and could be in a bear market for years.

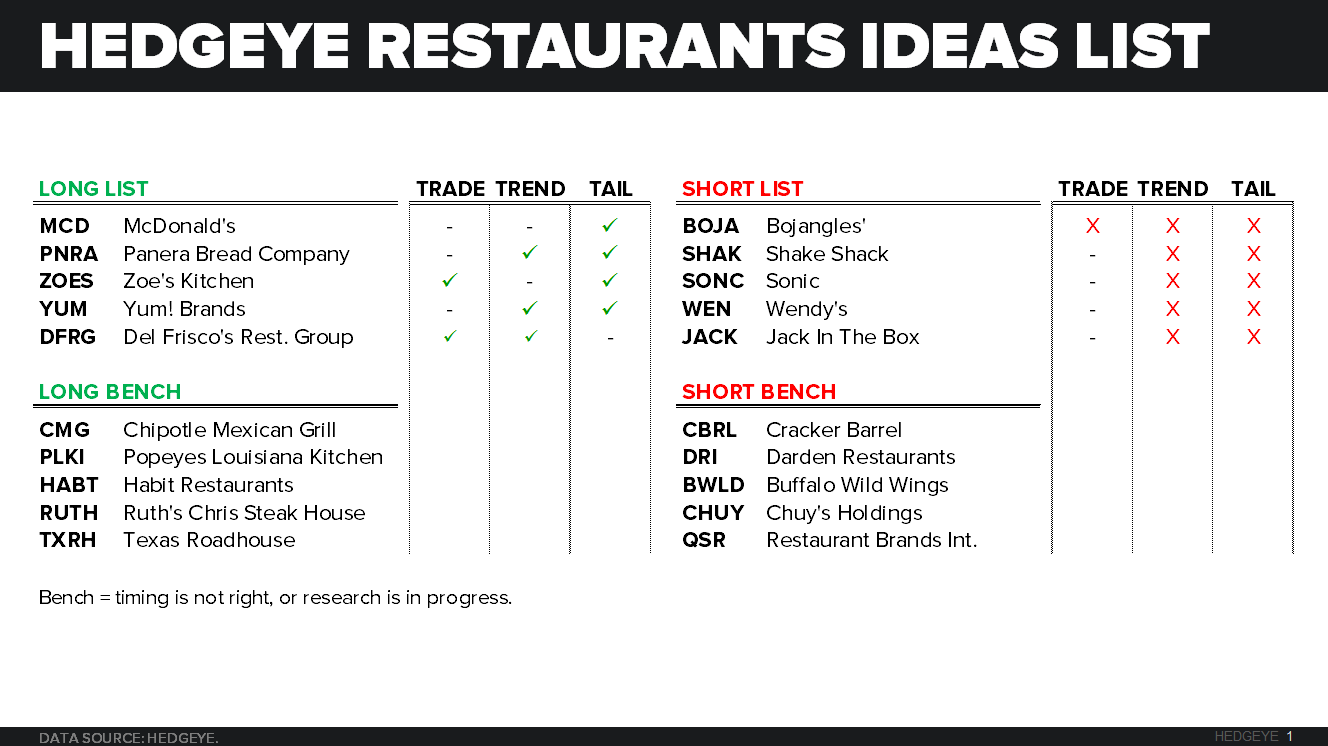

HEDGEYE LONG IDEAS - MCD, DFRG, YUM

ADDITIONS TO THE HEDGEYE LONG BENCH - RUTH, TXRH

OTHER BENEFICIARIES - SHAK, QSR, SONC, JACK, BLMN, HABT, WEN, RRGB

On Thursday, October 15th at 1:00 pm ET we are holding a Thought Leader call discussing the current crash in cattle prices and the long-term implications for the industry. On the call will be James G. Robb, Senior Agricultural Economist and Director, Livestock Marketing Information Center.

The call will focus on the following:

- Historical context to the current cattle market supply and demand dynamics

- The free fall in cattle prices

- The cattle life cycle and why the largest cattle herd expansion in history is now underway

- Why the “fat” inventory of cattle will continue to drive prices lower

- The ramifications of falling beef prices across the supply chain

- A time table for key industry events that could drive price down further

Purchasing over $1 billion of red meat, McDonald’s is one of the biggest beneficiaries of the lower beef prices. We are bullish on the MCD turnaround and now the company will likely be seeing a significant commodity tailwind in 2016-2017.

JIM ROBB BIO

Jim Robb is the Senior Agricultural Economist at the Livestock Marketing Information Center (LMIC) and for 18 years has served as the Director. He has written several hundred articles and newsletters on a variety of agricultural marketing and cattle industry topics. Jim is a regular speaker at conferences throughout North America and has given expert testimony to the US Senate Agriculture Committee.

Prior to joining the LMIC, Jim was an Agricultural Economist at the University of Nebraska. He also has worked in the agricultural banking sector. Jim received degrees in Agricultural Economics from the University of California-Davis and from Michigan State University.

The LMIC began in 1955 and is a unique cooperative effort that supports market education, research, and outlook. Currently, the Center includes 28 US Land Grant Universities, Utah State University was a founding partner. The Center also includes six USDA agencies, and several associate organizations.

Call details and materials to be provided next week.