“Without labor, nothing prospers.”

-Sophocles

Tragedy comes from the Greek word tragoidia. “It is a form of drama based on human suffering that invokes in its audience an accompanying catharsis (or pleasure) in the viewing.” (Wikipedia)

Sound like the US jobs market? Thankfully, I don’t need to channel my inner Greek Tragedian anymore to make a call that US Employment is A) #LateCycle and B) #Slowing. That’s now marked-to-market, in US Treasury Yield terms.

Both September Non-Farm Payrolls (NFP) and Private Payrolls (PP) slowed to their weakest rate-of-change growth rate of 2015. If your bottom-up work showed that August was slowing. Well done. They revised AUG to the lowest nominal NFP gain of the year too.

Back to the Global Macro Grind…

While I’m sure the Old Wall storytelling will be epic this morning on “why the jobs number wasn’t that bad” … and “stocks closed up on the day… the bottom is in…”, blah blah blah… allow me to re-interrupt with economic cycle-reality:

- The jobs number sucked… and labor data will continue to suck into year-end

- Both the US Dollar and Rates hit oversold lows Friday morning (yes, markets discount pending news)

- After signaling immediate-term TRADE oversold, stocks got squeezed off those morning lows too

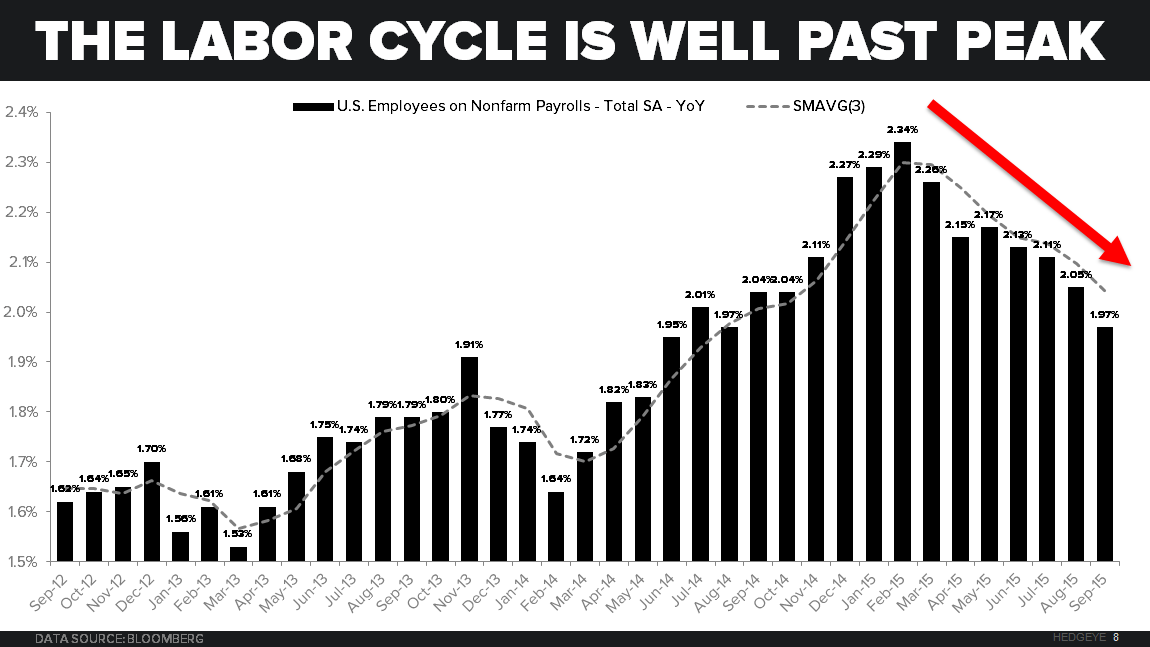

Sucked? Yes. See our Chart of The Day:

- SEP Non-Farm Payrolls slowed to 1.97% year-over-year vs. the cycle peak of 2.34% in FEB

- SEP #Slowing = 7th straight month of slowing and < 2% growth for the 1st time in 13 months

- NFPs of 136k and 142k (AUG and SEP, respectively) have crashed -32% from the NOV peak of 423k

Btw, if they didn’t suck, you wouldn’t have seen a re-test of the YTD lows for the SP500 (Friday pre 10AM) as the 10yr yield dove to 1.93%... But, but, but… if only everyone would have been positioned for this 3-6 months ago.

“So”, let’s take a step back and review what really happened week-over-week, within the context of the last 6 months:

- US Dollar Index -0.4% week-over-week and -1.6% in the last 6 months

- SP500 +1.0% week-over-week and -5.6% in the last 6 months

- Russell 2000 -0.8% week-over-week and -12.6% in the last 6 months

Oh, wow, Russell down with the US Dollar and US economy slowing. Imagine that. Over 80% of the Russell’s revenues are tethered to US domestic revenue expectations (*note: not “China”).

And on Down Dollar, Down Rates (2yr = 0.57%, 10yr 1.99%) – here’s how they achieved that SPY Up, Russell Down score:

- Basic Materials (XLB) +2.9% week-over-week (even though still -15.5% in the last 6 months)

- Energy Stocks (XLE) +2.5% week-over-week (even though still -17.8% in the last 6 months)

- Financials (XLF) -0.5% week-over-week, despite the “up tape” on Friday…

*note: more US domestic Financials exposure in the Russell than in the SP500

In other words, as #LateCycle growth expectations slow, Dollar Down = “reflation” of crashing prices and Rates Down = Financials Down. It’s really not that complicated. If you extend the analysis to International Equities:

- Dollar Down = Euro Up +0.2% wk-over-wk, and German DAX -1.4% on the wk (crashing -20.2% in the last 6 months)

- Dollar Down = Latam MSCI Equities +0.9% wk-over-wk (inline w/ SPY) but crashing -25% in the last 6 months

- Dollar Down = Brazilian Stocks (Bovespa) +4.7% wk-over-wk but still -11.6% in the last 6 months

Yeah. Dollar Down on Super #LateCycle US growth slowing is sweet. It stops things from crashing vs. #StrongDollar, and beats up on the things everyone who thought it was “mid-cycle slowdown” is long of!

Post the US equity market squeeze, the best news for High Beta, Small Cap, US Equity Bears (ugly style factors) is that Consensus Macro hedge funds that shorted low (after being levered long higher) covered some of those hedges Friday afternoon.

The net SHORT position (CFTC non-commercial) in SP500 Index + Emini futures and options contracts moved from a YTD highs in the 2 weeks prior to -194,392 (that’s almost 32,000 contracts of less bearish positioning, week-over-week).

While the politicized and alleged US “labor market strength” remains a great tragedy in American storytelling, it will be interesting to see how fund manager performance problems morph from begging for a “rate hike” to cheering on more easing.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.94-2.09%

SPX 1

RUT 1070--1141

USD 95.25-96.70

EUR/USD 1.11-1.14

Gold 1125-1155

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer