“Sleeping is no mean art: for its sake one must stay awake all day.”

-Friedrich Nietzsche

I’m going to make a bold prediction: This will not be the best Early Look of the year.

Clever linguistic acrobatics are a rested man’s game and I haven’t slept since Tuesday as @HedgeyeFIG and I were busy prepping to bring the housing research thunder on our 4Q Themes call yesterday.

(Incidentally, we’ve had a pretty $$$ run in housing calls over the last 7-qtrs - if you’d like the detail on our attempt to maintain the analytical momo in 4Q, email )

Plus it’s Friday – Jobs Friday no less – and risk rarely rests. And since I'm both head housing drummer and lead domestic econ vocalist for our Global Macro Boy Band, I’ll play the next gig.

… Ya gotta Macro Like You Mean It!

Back to The Grind …

As we highlight probably every month, we haven’t figured out a way to consistently model and convictedly forecast a point estimate on the monthly payroll figure – so we don’t.

The current price/quant signals and our TREND view on domestic fundamentals generally drives our positioning into the number and we simply take what BLS gives us on jobs day and respond accordingly.

But since the collective investor fascination this morning will be guessing on the over/under on everyone else’s guess on the rand() function that is the NFP print, we’re tasked with observing and assimilating the machinations of a restless market on its most manic day of the month.

Keith will be captaining the real-time macro strategy session on Fox Biz this morning before the @Hedgeye Macro Show if you’d like to tune in.

Since we don’t know what the payroll number will be, let’s focus on some stuff we do know:

- Trend = Less Good: No matter how you parse either the NFP or ADP employment numbers, the trend has been slowing: 3M ave < 6M ave < 2015 ave < 2014 ave. Was it inevitable that we slow off the 2H14 pace of +273K/mo. Yes, but less good is less good.

- The Late Late Show: October will mark the 77th month of the current expansion (the mean & median over the last century are 59-months and 50-months, respectively). Do expansions following financial crises and balance sheet recessions run longer in period and lower in amplitude (i.e. long and muddling). Yes, while we’re late cycle, the duration of the expansion is not surprising. Do conventional expansions and bull markets die of old age and without focused central bank tightening. Not typically but this, of course, is not a typical cycle (financial crisis, unprecedented global central bank intervention, negative global demographic trends, global over-leverage, global liquidity trap conditions, etc.)

- RoC | Past Peak: From a rate of change perspective NFP peaked in February at +2.343% YoY. Re-breaching that growth rate to the upside is not going to happen. It’s just math meeting realism. The M/M change in NFP would have to be +602K for that to happen. What does that mean? Not much in the very immediate-term, at least based on historical precedent. As the Chart of the Day below illustrates, payrolls run into the law of large numbers as an expansion matures with peak rate-of-change in NFP occurring ~2yrs ahead of the peak in the cycle. Cycles take time to play out – let it breathe. And, as noted above, typical business cycle oscillations in the post-war period are only loose analogs for the post-crisis expansion.

- ISM Mfg: The employment sub-component in the ISM manufacturing survey for September came in at 50.5 – flirting the contraction line for the 2nd time in 6-months. Again, is the ongoing softness in the manufacturing sector surprising with slowing global growth, strong dollar (↓ export demand) and cratering energy sector capex? Not really, but that doesn’t mean it doesn’t matter. And (next bullet) …

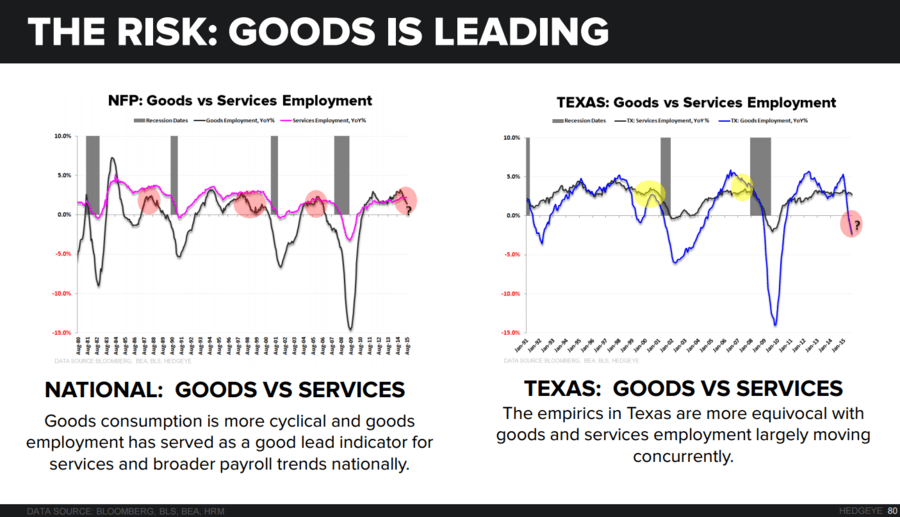

- Good vs. Services: Because consumption of and investment in durable goods is more cyclical than nondurable/services consumption and carries a higher elasticity to macro conditions, the employment trend in the goods producing sector tends to front-run negative inflections in the broader labor market. Employment growth in the goods sector has been in discrete deceleration – slowing from +3.0% at the start of the year to just 1.36% as of August. Watch this trend – U.S. centric strategists can live in an “de-coupler’s” echo chamber, globally interconnected Macroeconomies cannot – at least not sustainably.

- What to Watch: The product of total employment, ave hours/wk and earnings/hr gives you aggregate income for the month and aggregate income determines the capacity for consumption (and, generally, the trend in actual household consumption). So long as income trends hold in a consumption economy, it will be hard for the domestic (real) economy to truly come off the rails – despite a worsening trade balance and flagging investment.

- Tea-Leafing the Internals: Most of the market angst centers on the read-through to policy. Here’s a rough playbook and the likely implications for a selection of data combinations:

- Big NFP gain, (still) no wage growth = slack still pervasive, Fed probably communicates a bullish interpretation of the data

- Lower Print, Accelerating wage growth = slack diminishing – Good in terms of approach toward full employment, but the Fed can’t hike (sustainably) into middling and declining payroll gains.

- Lower, (still) no wage growth = stall speed, Doves bunker down a bit, Dots pack their bags for a push out.

- More of Same (200K +/- & Middling Wage growth) = More of same on policy side. Global macro conditions remain a fulcrum for domestic policy.

- GDPNow … or Later: The Atlanta Fed GDPNow model – which has had the hot hand in recent quarters - currently sits at 0.9% for 3Q. Recall, the model gets increasingly accurate as quarter-end approaches and more data is incorporated. The skinny on the quarter is basically this: Consumption will remain pretty good while Net Exports, Investment and Inventories will continue to drag – and comps only get tougher.

- Rationalization Indicators: This is largely qualitative but my inbox has seen a notable influx of esoteric indicators of late. The increased trotting out of squirrely, netherworld “indicators” via sell-side distribution channels typically signals that data-mining and the “twisting facts to fit theories” exercise has escalated.

To summarize and conclude:

Next Verse, Same As the First: Inclusive of whatever the BLS delivers this morning: Slower-and-Lower-for-Longer remains the call.

You buy that theme opportunistically and with a Trend view – you don’t buy it at every time and price.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.98-2.19%

SPX 1

RUT 1067-1125

VIX 19.94-29.12

Oil (WTI) 43.64-47.21

Gold 1104-1155

Happy Friday. To Sundays, siesta’s and cerebral exfoliation,

Christian B. Drake

U.S. Macro Analyst