The expression “long in the tooth” is an idiom that refers to old people, particularly when their age makes them too experienced or too seasoned for a particular thing, event, or role. When people use this phrase they are generally implying that the subject is past his or her prime.

While the phrase usually refers to horses or people, we are suggesting that CMG is getting older and looks like it will experience some growing pains in the near future.

- Quality real estate is getting harder and more expensive to get

- Are the 2015 supply chain issues a one off experience?

- Slowing sales trends might not end in 3Q15

REAL ESTATE

We keep hearing from our sources that finding quality real estate sites is becoming a bigger issue for a number of restaurant companies. Part of the problem is the significant growth of the fast casual segment and the recent restaurant IPO boom that has put pressure on A rated locations. It goes without saying, it never ends well for restaurant growth stocks when faced with the ever-growing demand and shrinking supply of quality real estate sites. The majority of Fast Casual restaurant concepts have similar real estate requirements. Most concepts prefer to locate in high traffic shopping centers with good visibility. In most cases, these shopping centers have a mix of tenants, and many have language in their lease restricting the sale of similar products or food.

The real estate issue is an industry wide phenomenon, not just one facing CMG. That being said, if you are a burrito concept (or a better burger concept), and if there is another burrito/burger concept in the shopping center, the landlord will often be prevented from entering a second lease. Therefore, in popular locations, it’s not unusual to have an existing competitor on all four corners of a strong intersection.

There is no immediate issue pressuring CMG in 2015, but it’s likely that rents and availability will be a bigger issue in 2016.

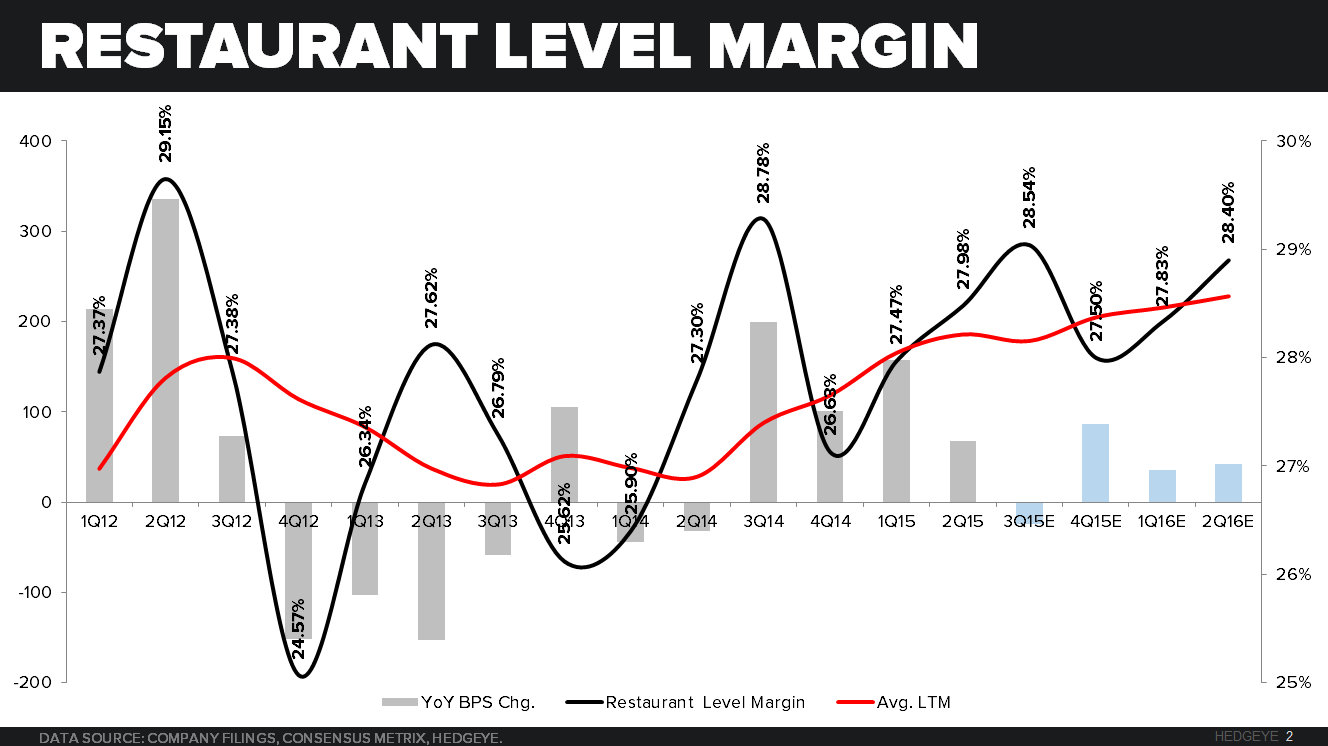

SUPPLY CHAIN ISSUES

The bigger CMG gets the harder it is going to be for them to adhere to their food with integrity mantra. The challenge is even greater when we come to grips with the notion that the company will likely outgrow the supply chain over the next couple of years. By 2017, CMG’s sales will account for 8% of all sales of non-GMO products at retail. Therefore, the bigger challenge for the company is building a supply chain that can feed the ever growing needs of the company. The Carnitas crisis of 2015, may just be the tip of the iceberg for the company.

What we find strange is, at the same time the company continues to punish (make fun of ) the same supply chain the company needs to be successful. Evidence of this can be seen in the CMG game called, Friend or Faux – click HERE to try it out. The essence of this game goes beyond attacking McDonald’s or another restaurant company; it goes after the entire supply chain of food products.

Has CMG gone too far, who is fighting back? In a recent article, “Chipotle Hypocrisy: American Antibiotics Bad, British Antibiotics Good” (ARTICLE HERE) is clearly calling out CMG’s business model and challenging some of the ways the company does business. It also put a spotlight on the supply chain issues and some of the complications the company faces as it gets bigger.

The supply chain puts CMG’s long-term same-store sales trends at risk. First, the obvious, supply of available product is a clear issue. Second, the more the company invites detractors to expose CMG’s issues, it will hurt the consumer perception of the brand.

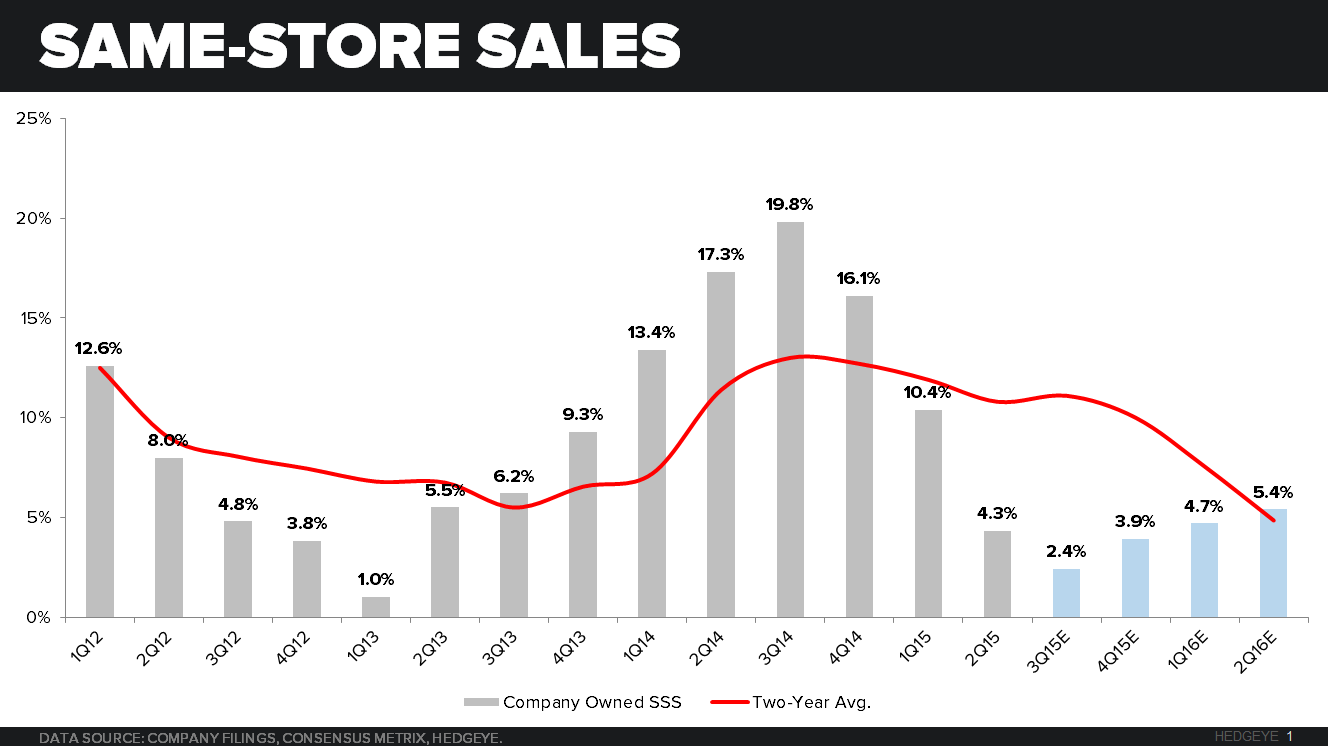

SLOWING SALES TRENDS

3Q15 COULD HAVE ITS ISSUES

It’s usually never a winning proposition to make a call on any given quarter, especially for CMG. That being said this quarter CMG is up against the most difficult quarter the company has experienced since coming public in 2006.

- 4% pricing is rolling off sequentially

- Comparing against 19.8% same-store sales; 6.3% pricing and 3.4% traffic

- The street is expecting a 30bps sequential acceleration in 2-year same-store sales. Management believes that the pork shortage may have impacted 2Q same-store sales by about 200bps.

- The 3Q15 2.4% same-store sales estimates suggest that CMG will see pressure on the labor line

- CMG should see a benefit from lower dairy costs

- The 2Q15 labor scheduling issue also impacted part of 3Q15

- Hourly labor rates continue to accelerate

BOTTOM LINE

CMG is a great company and has been on our Best Ideas list for the better part of two years. There is enough evidence that there is a small shift that will begin to impact valuation. So we are taking it off the best ideas list and putting it on the bench.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst