“Never invest in something that eats while you are sleeping.”

-Dan Sullivan

Yesterday, I was at the kick off dinner of a joint conference put on by the Wall Street Journal and U.S. Chamber of Commerce called, “Accelerating America’s Middle Market.” When I mentioned I worked at a firm that was in the investment business, the quip above was passed on to me from the person seated to my right. Admittedly, it’s sage advice.

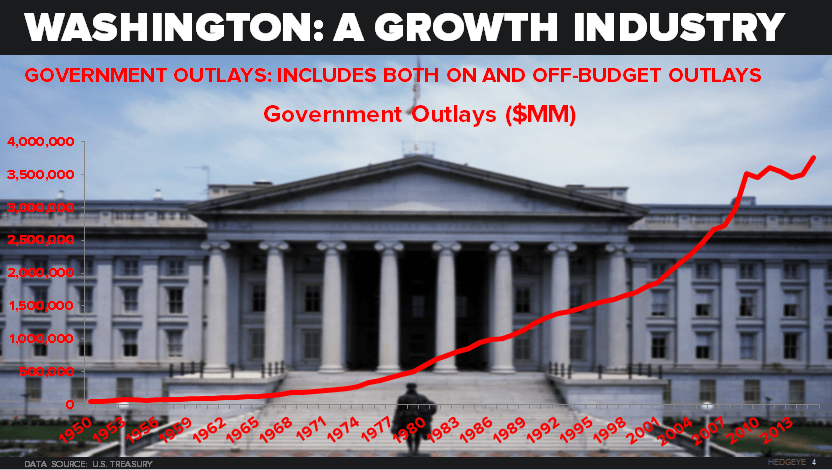

In the bubble that is Washington, no one seemed to notice the beat down that the stock market was taking yesterday. In part, this makes sense since the federal government is a growth industry, and in most years appears to have no real correlation to the real economy or stock market. In fact, since 1950 federal government outlays have declined on a year-over-year basis in only 5 of those 65 years. Over the entire period, as we’ve highlighted in today's Chart of the Day below, spending is up an astounding 87x.

At annual outlays of more than $3.5 trillion, an annual deficit of close to $500 billion, and outstanding debt of more than $18 trillion, it is pretty clear that the federal government eats while we are sleeping. And then eats some more. And more.

Back to the Global Macro Grind...

While I was in Washington hob-nobbing yesterday, Keith spent the a couple hours in the morning on Fox Business hosting the morning show with Maria Bartiromo. One of the interviewees during Keith’s segment was none other than former Florida Governor Jeb Bush. By most appearances, Jeb has the staying power (translation: money) to remain in the race for the Republican nomination, but his polling number are dreadful at best.

According to the most recent poll aggregates from Real Clear Politics, the top five contenders and their polling numbers are as follows:

- Trump – 23.4%;

- Carson – 17.0%;

- Fiorina – 11.6%;

- Rubio – 9.6%; and

- Bush – 9.2%.

Clearly, the electorate on the Republican side continues to increasingly support outsider candidates, who have no attachment to Washington or political jobs on their CVs.

On the Democratic side, Hillary Clinton still holds a sizeable lead over the field, a field at this point which only really contains Senator Bernie Sanders. Her lead may be short lived until current Vice President Joe Biden enters the race. We’ve also heard rumblings in our travels that Secretary of State John Kerry may throw his hat in the ring.

Despite being in the lead, Clinton is appearing more and more vulnerable. Her increased vulnerability is most evident in a recent Wall Street Journal and NBC news poll that shows Clinton basically in a dead heat when polled against Bush, Fiorina, and Carson. Meanwhile, Trump trails her by a good 10 points. This inability to get broad support and overcome his negatives may ultimately be what gets The Donald "fired" in his Oval Office quest.

As it relates to the markets, the most imminent catalyst coming out of Washington, DC is likely to occur in mid-December. While Speaker Boehner’s resignation has paved the way for the passing of continuing resolution to keep the government open (and spending your hard earned money), the resolution will expire around December 11th.

Ironically, or not, that is also about the time that the U.S. government will have surpassed the debt ceiling. Technically, the Treasury has already surpassed the debt ceiling and is using so-called “extraordinary measures” to fund the government. By mid-December, the Treasury will have surpassed its ability to use these measures to borrow money to fund the government, so it will have to go back Congress to extend the debt ceiling.

Inasmuch as the last few months and weeks have been volatile for stock markets, it appears that Washington is going to rear its ugly head again in the next few months with the debt ceiling being eclipsed, the continuing resolution to keep the government open having expired, and a new Speaker of the House in place. For those of you that are concerned about a premature rate hike by the Fed, this is just another reason for our view of lower for longer to hold into 2016.

Keith noted as much that this morning in his Direct from KM note to clients (email if you’d like to be added) when he wrote:

“10yr – the bond market either doesn’t believe Yellen on the DEC hike and/or is signaling that that would flatten the curve and slow growth faster – either way, next support = 2.04% and lower-highs of resistance continue at 2.17%.”

And as we like to say around Hedgeye, markets don’t lie, people do.

Before signing off and leaving you with a gloomy view of the world, I did want to highlight a stock that we are positive on with what we believe will be better than expected fundamentals . . . and the stock is the venerable Starbucks (SBUX). As our restaurants Sector head Howard Penney wrote yesterday:

“In addition to increasing throughput and efficiency of the store, this app is meant to help drive incremental traffic. In the chart below assuming flat 2-years trends, estimates for Americas traffic, would accelerate to 5% in 4Q15. This would be a significant positive for the company and likely make the consolidated traffic number look conservative. We believe with the new app launched nationwide, consensus estimates may turn out to be slightly conservative.”

The app Penney is referring to is Mobile Order & Pay (MOP). The video below outlines some of his proprietary research on why he is positive on the app and its ability to drive same store sales at SBUX.

https://app.hedgeye.com/insights/46584-is-mobile-order-pay-the-holy-grail-for-starbucks-sbux

Long SBUX and short DC anyone?

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.04-2.17%

SPX 1

VIX 23.03-28.76

USD 94.65-96.99

Oil (WTI) 43.75-47.65

Gold 1112-1155

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research