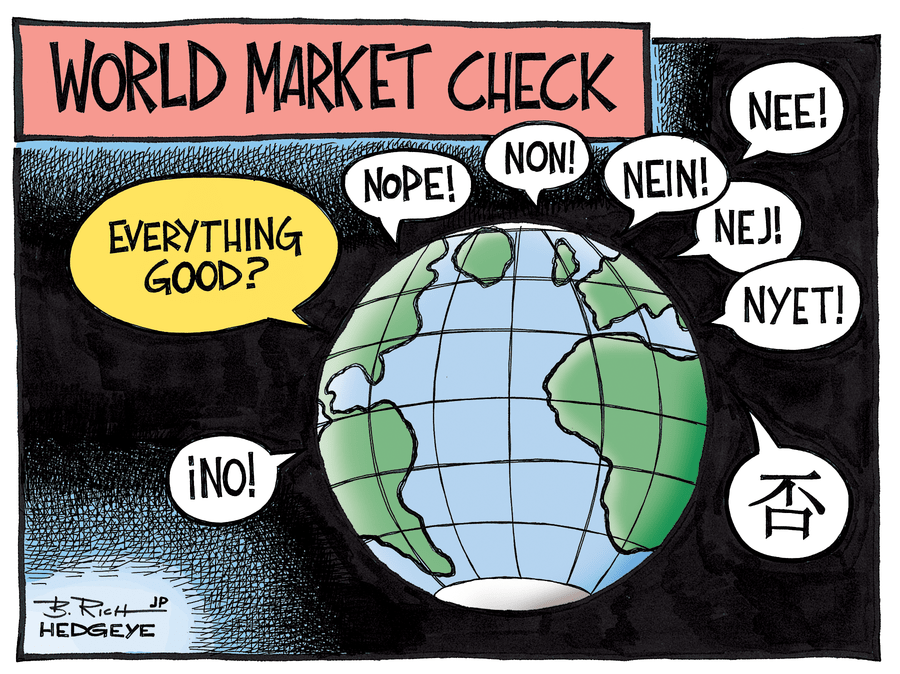

Biotech stocks (IBB) moved into full-blown crash mode on Friday. The sector is down-22% from its July peak. It’s now down another -3% this morning.

* * * * *

These former high-fliers have officially joined China, Germany, Spain, Oil, Emerging markets, etc, etc in what has become the most visible, slow-moving-train-wreck I have witnessed in High Beta in my career.

(Oh. Nearly forgot. Latin American Stocks (MSCI) are down -27.3% in last 3 months.)

In related news, our fearless IMF prognosticators just cut their global growth forecasts (again) as macro markets continue to crash.

> Houston, we have a problem…

> Wall Street, we have a problem…

> Beijing we have a problem…

> Frankfurt, we have a problem…

> Madrid, we have a problem...

* * * * *

Editor's Note: This is an abridged, brief excerpt from our morning research. Incidentally, we made the contrarian, global growth slowing macro call and its related market implications. Click here to learn more about it and how you can become a subscriber to our world-class research.