We are adding ConAgra Foods (CAG) to the Hedgeye Consumer Staples Best Ideas list as a LONG.

We don’t believe there is another Consumer Staples name that has been more of a chronic underperformer than CAG. CAG has underperformed the S&P 500 by 38% of the last 20 years. Over the past 5, 3 and 1 years the stock has outperformed the S&P 500, up 13%, 13% and 28%, respectively. A significant part of the recent outperformance is due to the announcement of the new CEO and Jana taking a significant stake in the company.

ConAgra operates at margin levels well below the competition. A lot of this has to do with the businesses they are in, Private Label, Frozen and some lower end center-of-store items. But there is upside here. The new CEO spoke to upgrading the brands appearance through package design and improving the quality of the food, both of which will go a long way to helping the company attain higher price points at retail.

Recently, the disaster Ralcorp acquisition has finally led to Jana taking a significant position (with board representation). In February 2015, the CAG Board announced that it hired Sean M. Connolly as its new CEO. The new CEO’s resume and industry contacts are the right combination to reshape this company into a premier food company once again. The alignment of the CEO, Board and activist shareholder forms a strong combination to take control of a struggling company to create significant upside for shareholders.

ISSUES THE COMPANY IS FACING

- Leveraged balance sheet –Over the last five years, the company’s failed acquisition of Ralcorp and its generous dividend and share repurchase program has increased the debt on the balance sheet.

- Too shareholder friendly –The Company has paid out 78% of operating cash flow in dividends and share repurchases.

- Under invested in the business – Over the last eight years the company has seen a steady decline in capital spending as a % of sales.

- Significantly lower margins than competition –the company has a lot of upside as they improve the quality of their portfolio over time.

- Little international exposure – The Company has not invested in its international operations.

SHAREHOLDER MEETING SETS THE STAGE

Given the poor performance of this company over the last 20 years, another boiler plate restructuring will not give investors much confidence. The company needs a bold program that will shake the company down to its core foundation. The divestiture of the Ralcorp Private Brands business is just the beginning to this turnaround story. At the annual shareholders meeting on Friday, CEO Sean Connolly spoke briefly about the changes to come. He spoke to sweeping changes across the company from the structure to how they work. He gave little details at the annual meeting, saying that the company plans to tell employees the details first, and if everything goes well, that will be by the end of this week.

Reading between the lines of his statements, big changes are coming.

He went on to say “will Illinois have a presence in our future, likely yes, will Omaha have a presence in our future, absolutely yes.” Illinois is where their consumer foods business is headquartered and Omaha is where the majority of their R&D and Quality operations are located. Sean went on to say, “Lamb Weston will continue to play an important role in our retail business.” Additionally, he spoke to accelerating the business internationally, (mainly China) where they serve predominately quick service restaurant chains.

Some of the key words from his comments at the annual meeting:

“Embrace bold change”

“Bold action”

“More focused company”

“Disciplined and focused”

“Pledged to be transparent”

“To stay competitive we must change”

HEDGEYE VIEW OF WHAT IS NEXT

We don’t know exactly what CAG will decide to do, except for the fact that the sale of the private brands business is well underway. In our opinion, there is little risk of this deal not going through given the relative quality of the business, and the distressed asset price that it will most likely go for. Rumored acquirers at this point include Treehouse (THS) and former owners Post Holdings (POST). Given POST’s balance sheet right now and other acquisitions there are still working on integrating, we view them as an unlikely acquirer. Treehouse looks to be in the lead from our vantage point as they would be able to reap a lot of synergy and scale benefit.

It’s clear that job cuts are coming next, how deep they will go is unknown. There are plenty of case studies from their fellow CPG companies that the consulting companies working with them know what works most effectively. Some form of zero-based budgeting (ZBB) will most likely be implemented as well.

Now, for the rest of the portfolio.

From Sean’s commentary during the shareholder meeting we would say for now, commercial foods is safe. But he left the door open for Naperville, Illinois being less than important to the company in the future. We believe there is going to be a pruning of the portfolio. Our suggestion would be to divest lower tier non-strategic brands from the portfolio to focus energy and capital on the most important ones. When looking at their portfolio there is not much to get excited about, center-of-store, frozen aisle type items. But there is still value there brands like Healthy Choice, Marie Callender’s, Hunt’s, Alexia, etc. still hold great value. This company clearly needs to focus on frozen and possibly expand within that aisle. Shed some can businesses like Ro Tel and Ranch Style that are not on-trend and aren’t top tier brands but could still hold some value to potential buyers.

If management wanted to go big, they could get creative and do a Reverse Morris Trust (RMT). In this scenario we believe you would have to spin off the frozen assets or possibly the whole consumer foods segment and merge with a company like Pinnacle Foods (PF) or B&G Foods (BGS). This would be the most tax efficient and also the most transformative.

We believe the days of value destruction are over at CAG. There is significant room for margin improvement at CAG and we believe that the combination of a new CEO with an aggressive core shareholder creates a stock we want to own in this market. In the coming weeks we will expand on our thesis and where the biggest opportunities are.

ANALYST RATINGS

Only 36% of the analysts have a buy on CAG! Seems as though everyone is waiting to see what happens next. Given the confidence we have on how the turnaround will unfold, the time to go LONG is now.

SHORT INTEREST

Short interest is slightly above its five year average of 1.6%, currently at 1.8%.

VALUATION

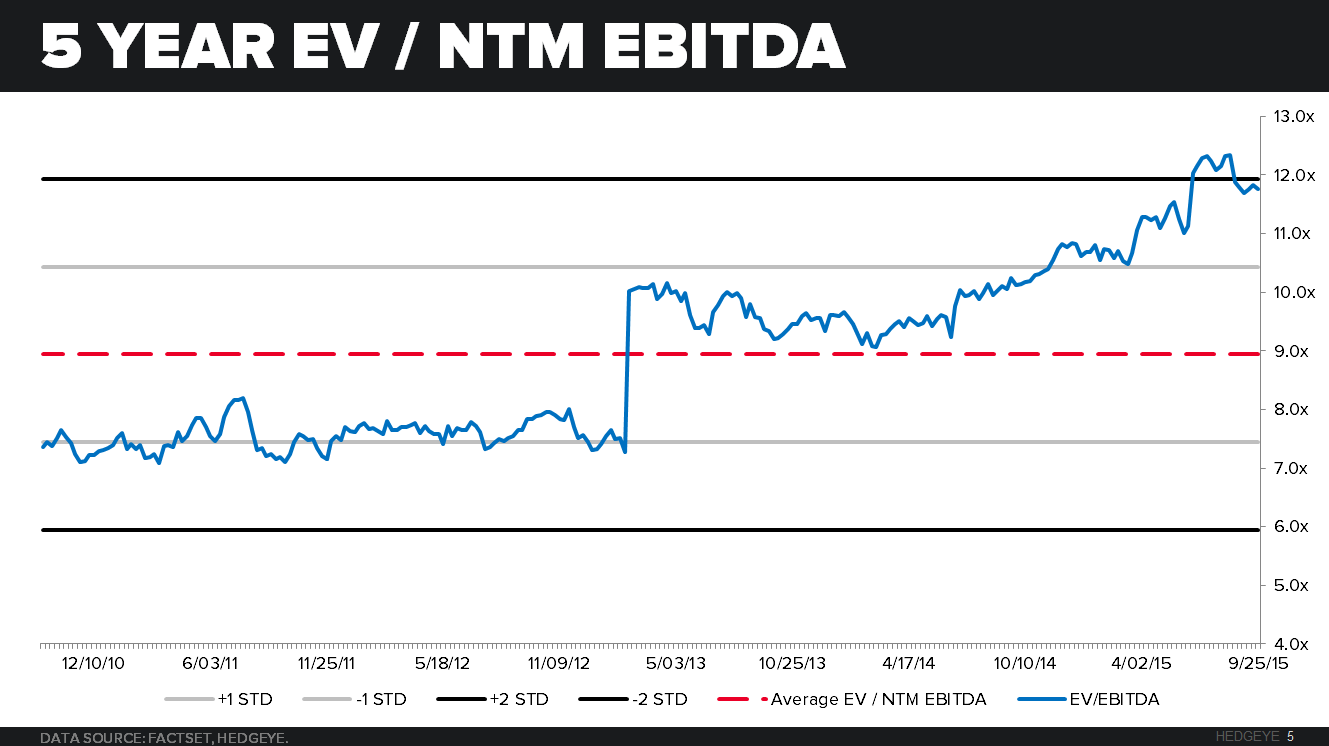

Below is the 5 year EV/NTM EBITDA chart. Although this company looks expensive, and has risen in valuation a lot over the last five years, it is still slightly undervalued compared to its peer set. We strongly believe that with the upcoming transformation this company will work into this valuation and beyond.

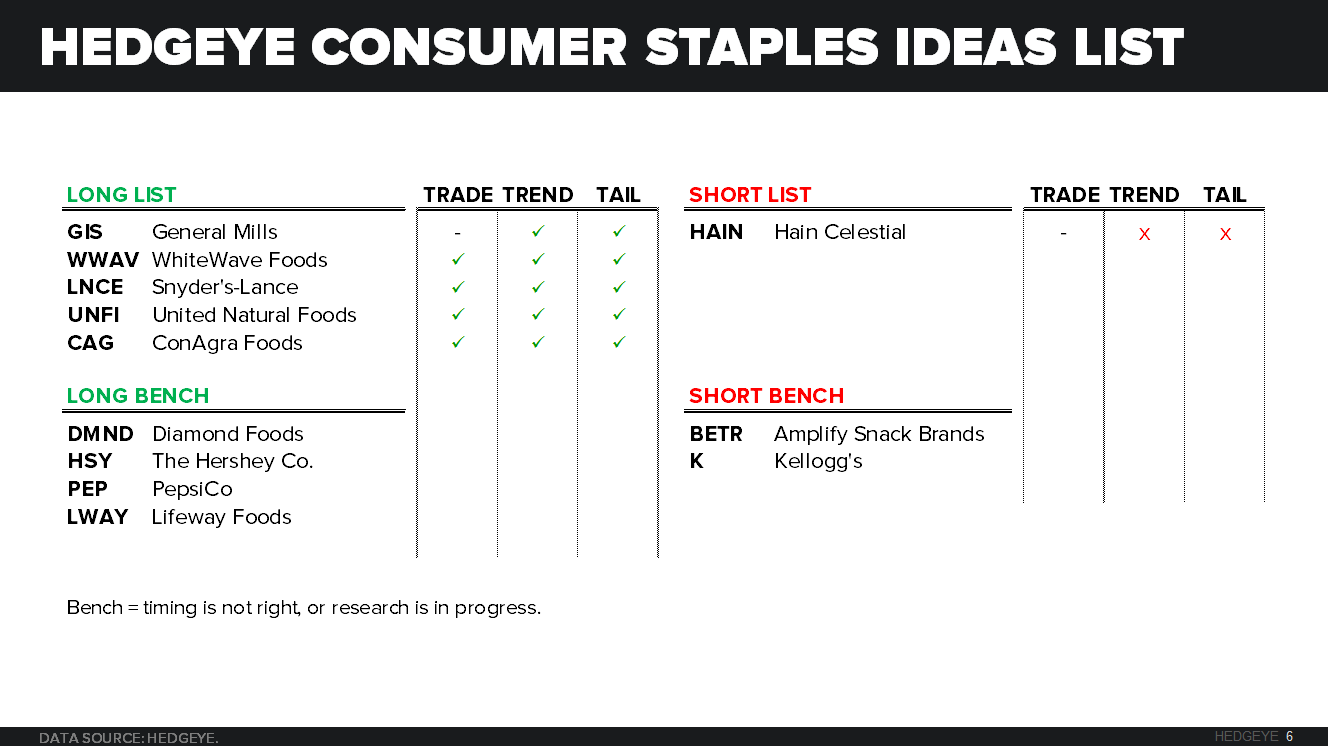

BEST IDEAS LIST

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst