Below are our analysts’ updates on our thirteen current high conviction long and short investing ideas. Please note that if nothing material has changed in the past week which would afffect a particular idea, our analyst has made a note of this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or les

IDEAS UPDATES

TLT | EDV | GLD

The yield on the benchmark 10-year U.S. Treasury note touched a one-week low Thursday before Janet Yellen delivered her speech in Amherst, MA later that evening where she reaffirmed that a majority of the monetary policy committee was in favor of raising rates in 2015.

That was good for a +4 basis point move. Pretty weak.

Question: Do you believe her?

Did you believe her when she planned to raise rates in June?

Is the U.S. economy still showing signs of a cyclical slowdown? Yes. If you, like us, remain skeptical on the said policy path from our omnipotent central planners, and you believe growth continues to slow, then we respectfully submit that you sit on your GLD and TLT allocations.

Relax. Breathe.

On a related economic note, this week's telling durable goods orders reading, which typically shows strength early cycle and weakness late cycle (leading indicator), slowed for the seventh consecutive month in August.

Durable goods, business investment, net exports and goods inflation remain in discrete deceleration while the labor market (jobless claims), continue to show late-cycle strength.

Leading Indicators (Bad) + Lagging Indicators (Good) = #LATECYCLE

As we’ve highlighted, Initial Jobless Claims have been the most consistent, lead labor market indicator for the economic cycle with peak improvement occurring approximately seven months ahead of the economic cycle peak and coincident with or slightly ahead of the equity market peak.

On Friday, GDP, CORE Inflation, and personal consumption were all upwardly revised in their Q2 third revisions:

- The Q/Q SAAR GDP print was revised to 3.9% for Q2 vs. +3.7% prior

- Personal consumption was also revised up to +3.6% from +3.2% prior

- Core PCE revised up to +1.9% from +1.8% prior

Remember that because consensus navel-gazes on the Q/Q SAAR GDP number, the Q3 GDP has to comp on top of +3.9%. Tough. Our GDP expectations for Q3 remain in a range of +0.1%-+1.5% on diffucult Q3 comps (YY of course). That's a far cry from current consensus expectations.

Whichever way you want to slice it, Q3 GDP comps are difficult. And, once the data comes out, we think expectations will be downwardly revised again.

In other words, wait for yet another Fed punt on a 2015 hike.

ZBH

To view our analyst Tom Tobin's original report on Zimmer Biomet CLICK HERE

We've noted previously a study demonstrating a 6-fold increase in knee replacement surgery for the newly insured compared to a matched continuously insured population. We assumed the Society of Actuaries assessment of Knee Replacement case volume was correct, applied their reported case rate per 1000 member months to the ACA's newly insured, and derived number for knee replacement surgeries among the newly insured.

The growth contribution appears to be significant. The impact increased over the course of 2014 as enrollment ramped, peaked in 1Q15, and appears likely to slow if utilization rates of the newly insured (0.22 cases per 1000 member months) revert to baseline (0.03 cases per 1000 member months).

GIS

1Q16 RESULTS

Constant-currency comparable net sales increased by 2% in 1Q16, while comparable volume was up 1%. General Mills reported total company net sales in 1Q16 of $4.21B coming in slightly under consensus estimates of $4.25B. Embedded within the overall company top line miss is a top line beat within the U.S. Retail segment, which reported sales of $2.53B versus consensus estimates of $2.51B.

While we dig into some key details below, performance in the U.S. has consistently been a source of concern for investors and management. The fact that the U.S. segment has outperformed expectations is a big deal. Adjusted gross margin increased 290 basis points due to net price realization and cost cutting initiatives. Due to Project Catalyst, their corporate cost cutting program, SG&A declined 6%. Cost cutting initiatives have been serving GIS well, reporting EPS of $0.79 ex-items beating consensus estimates of $0.69 by $0.10.

U.S. RETAIL― 1Q16 net sales for the U.S. Retail segment (USRO) rose 4% to $2.53B, Annie’s contributed 3 points of the net sales growth. The most encouraging performance in this segment is the growth of cereal, facing an easy comparison of -9%, cereal was up 6% in this quarter. Facing easy comparisons for the next two quarters, coupled with improvements to the segment, we are expecting the positive numbers to continue. The segment experienced a segment operating profit increase of 38% due to lower promotional spending versus a year-ago and a decrease in SG&A expenses and supply chain costs related to Project Catalyst and Century.

WHAT WE LIKED

CEREAL

We have been the cereal market bulls since our Black Book presentation on GIS.

Our view has always been that cereal is not in a secular decline, it is merely at a point of maturity. Manufacturers had previously been complacent with the cereal market for too long, innovation deteriorated and sales followed suit. Since this realization, the three big players in the market (GIS, K, & POST) have been investing in the category both on advertising and product improvements. General Mills is starting to see an uptick in their performance. We predict they will be the biggest beneficiary of a stronger category.

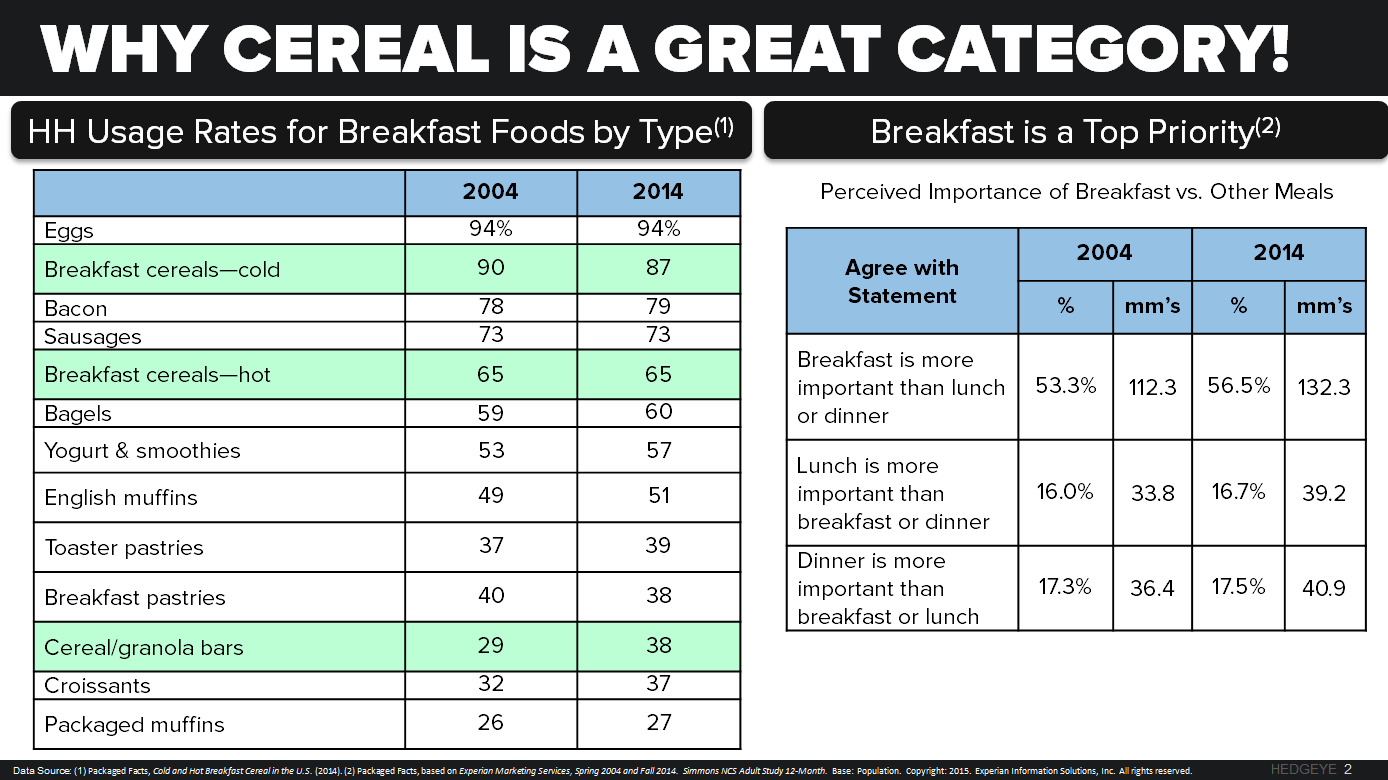

Our team also notes that the YOY monthly change in Breakfast Cereal Employment, compared to GIS cereal reported net sales YOY quarterly growth and cereal category retail sales all bode well for the future of cereal, as employment in this sector has been picking up steadily.

Please note the table below which shows data collected by Packaged Facts. It shows usage rates of breakfast cereal as well as the importance of breakfast. Strong employment numbers coupled with innovation such as gluten-free Cheerios, removal of artificial colors and flavors and sugar reduction; lead us to continue to believe the cereal category can return to growth.

RH

To view our analyst's original report on Restoration Hardware: CLICK HERE

Restoration Hardware opened its fourth Baby & Child store Friday in Greenwich, CT. This is proof that the 22,000 square foot Greenwich (opened in May of 2014) store is too small. And it also marks the first time we've seen RH swap out a Legacy Store for a Design Gallery in a market and then supplement the new footprint with an additional concept -- in this case it's Baby & Child.

Image source: Greenwich Time

Our analysis suggests that the Greenwich market could support a 65,000 square foot store. In other words, the current store, while in a great location, and at a significant ROI, could and should be much bigger versus how it exists today in order to capture the market opportunity and properly display the company's expanding category portfolio.

Instead of swapping out the door (the current Greenwich Design Gallery has extremely favorable rent economics -- especially given the prime location) for a bigger store, like we saw in West Hollywood and will see in Houston, RH is adding square footage across the street. The new door at 4,800 sq. ft. is taking over space vacated by Gap Kids (the RH Legacy Store the company closed last year was 5,500 sq. ft.).

More than anything, we think this is a very bullish statement on the success of the Greenwich market. The company would not be opening a Baby & Child concept unless the Design Gallery was crushing it in year one.

Between Baby & Child, RH Modern and RH Teen (which could both merit their own doors), and the addition of Kitchens still TBD, we think we'll see a lot more of this. As in, Legacy Store closures as new Design Galleries open up will be lower than most expect.

ZOES

Zoës Kitchen fared much better this week.

In case you missed it, shares were up approximately 9%.

We continue to be very bullish on ZOES long-term prospects due to the company's strong fundamentals, superior brand positioning, great growth prospects and strong early-stage average unit volumes and return.

Outside of the company’s strong performance, it's worthwhile to mention that Mediterranean dieting and the trend of healthy eating overall are growing increasingly more popular by the day. ZOES having sole ownership over this category, provides it a great long-term advantage to reap the benefits of this growing trend.

WAB

To view our analyst's original note on Wabtec: CLICK HERE

Fresh off his successful, longstanding bearish call this week on Caterpillar (it has underperformed the market by over 60% since his first short presentation on the name) our Industrials Sector Head Jay Van Sciver reiterates his short call on Wabtec.

Below is a key excerpt from a note he sent out earlier this week outlining his concerns for the company:

Faster Rail Networks Require Less Equipment

As rail congestion picked up in 2014, the slower speeds tended to pull equipment on to the track. Now that speeds are picking back up, we expect that equipment to be pushed back out. One can think of it as turning existing assets more quickly, or as analogous to the velocity of money vs. inflation. This is an important negative for WAB, as they sold parts and equipment to US Freight rails as equipment was sucked onto the network, while parts and equipment sales will likely fall below trend as that equipment comes back off.

LNKD

Hedgeye Internet & Media analyst Hesham Shaaban has no material update this week. To view his original report on LinkedIn: CLICK HERE

Shaaban reitereates that we remain long LinkedIn heading into the company's next earnings release in late October. We are still expecting a clean beat and raise, which we expect will be a positive catalyst for the stock, especially given the current dearth of good Internet longs.

PENN

Penn National Gaming continues to be our favorite Regional Gaming stock.

As Sector Head Todd Jordan notes, "PENN should benefit from the release of state gaming figures over the next few weeks. Recall that August was weaker than many thought. While we predicted this particular slowdown, our model is showing a sharp September rebound.

September revenues should rebound and serve as a catalyst for the stock going into Q3 earnings. On the research side we have not altered our views of PENN’s long term growth story. We continue to see more upside from current price levels.

MCD

To view our original note on McDonald's: CLICK HERE

McDonald’s clearly continues to be well-liked by our Restaurants research team and is a near perfect fit into our macro team’s current "style factor" preferences. This stock is high cap with a low-beta, coupled with a company turnaround story that is currently well underway. We believe this stock will do well through this tumultuous time in the market.

As previously mentioned, the company has all day breakfast starting on October 6. We anticipate this development as not only driving increased visits from existing customers, but also new customers that maybe don’t wake up early enough to get breakfast by 10:30am (or simply just people that enjoy eating breakfast items outside of the morning!)

New McDonald's CEO Steve Easterbrook has taken an internal activist approach to reorganizing this company. We believe we will see strong, positive signs of it all working during the 3Q15 call on October 22nd.

FL

This past Thursday, Nike reported the best and most impressive quarter in its 35 years as a public company. Whenever any company’s performance is so mind numbing – both on an absolute basis and relative to expectations – one has to wonder if there’s room to go. Is this the time to peel some off, or sell outright?

The stock closed Thursday at a $99.2bn market cap. It flirted with $100bn only twice before. But Friday it will hit the triple digits, and the question is whether it will fall below $100bn ever again.

Interestingly enough, the only negative in the quarter was a high level of inventories in the U.S. This will be nothing more than a hiccup for Nike, but it should absolutely slow growth, or impact margins for Retailers like Foot Locker, Hibbett, and Finish Line. We saw that manifested today in FINL where the sales to inventory spread at -8% was the worst spread we’ve seen in almost two years. That’s never a positive gross margin event.

FNGN

Earlier this week, Financial Engines announced that it is making its investment advisors available by phone to all 401(k) participants, whether those participants use the company’s advisory services or not. This is essentially a leverageable marketing tool for FNGN; the change will provide the company with direct access to customers who have the potential to convert from only having their assets on the FNGN platform to having FNGN manage their portfolios.

Advisors now have the opportunity to directly convey their value to customers and to make the case for FNGN fully managing the participants’ portfolios. We expect this to cause an increase in the conversion rate, which, as shown in the chart below, has already been rising.