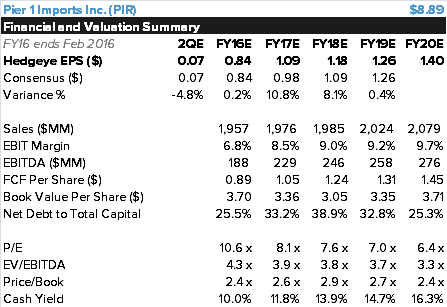

We’re not expecting a whole lot of positive news from PIR’s 2Q print (today after the close). EPS is a moving target, and guidance will be light. But when all is said and done we think that the results will show that the financial and operational inflection point for this beaten-down value stock is finally within reach. Are we concerned about a headline miss later today? Yes. We were well aware of these concerns when we added PIR to our Best Ideas list on August 31. Furthermore, we have yet to talk to anyone about this name that is not expecting an ugly quarter. Several analyst notes have already come out calling for a miss, and on top of that, short interest has raced up to 16% of the float – a four-year peak. We think they’ll ultimately be proved wrong.

A key consideration is that CFO Jeff Boyer will handle guidance for the first time after joining the company in late July. It’s not entirely clear how he will handle guidance…but we can’t imagine that he’ll want high targets his first year on the job. We’ve heard this concern from bears as well “new CFO will lower the bar”. Maybe we’d be concerned if the stock was up 20% over the past quarter, but we’re looking at quite the opposite – a 26% decline since the last earnings report in mid-June, and 12% over the past month. So will guidance be lower? Probably. But it’s very important to note that Boyer is likely to lower because he wants to, not out of necessity.

Why We Like It – PIR is a beaten-up, ugly value stock…there’s no two ways about it. But with the stock trading at just 0.5x sales – a level it hasn’t sustained in six years -- we think there are two primary questions to ask. 1) Are we going into a major recession? and 2) Is management going to do anything more destructive that would otherwise emulate a major recession? If you answer ‘No’ to both of those questions, then we think it’s a very good risk/reward to buy the stock with $3-$4 down and $20 upside.

Our Answers:

1) We have some major questions marks as it relates to the economy, but we’re not calling for an all-out recession.

2) This is a company that is no stranger to execution issues, but we don’t think that management is about to do anything more that would cause a downturn in the business (especially w/ new CFO taking the seat in late July). Quite the opposite, in fact. Consider this…

- Over the past three years, PIR gave up 5 points of margin as it played catch-up with its e-commerce business, which stood at only 1% of sales in 2013. Today it is pushing 17%. E-comm will continue to be a headwind as it grows to the mid-30s (about 130bps of dilution over 4 years), but the combination of merch margin recovery and store base rationalization should more than offset the dilution. We think that ~300bps of the margin recoverable.

- Interestingly enough, in our survey in this report, PIR’s categories ranked as the ones where consumers are most apt to switch sales online. If there is any company that should have invested in e-comm, it is PIR.

- We’ve had three straight years of elevated capex as the company built out e-comm capabilities. That rolls off this year, with asset consolidation (closing stores) and multi-year margin tailwinds takes RNOA from trough levels at 19% in FY16E to 31% by 2020. That’s a long tail, but even the slightest sign that we’ve found the bottom should make this stock rally.