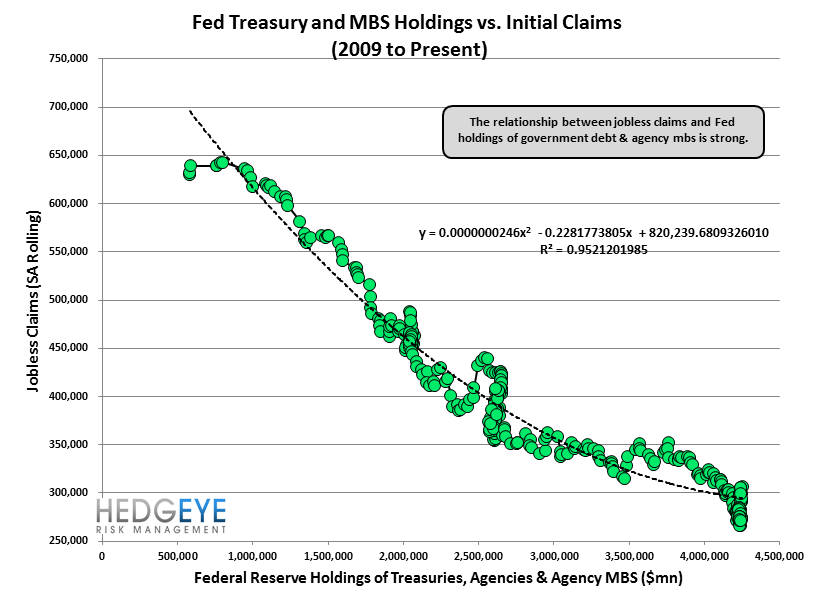

While durable goods, business investment, net exports and goods inflation remain in discrete deceleration alongside the retreat in global growth, the domestic labor market continues to tread a path of late-cycle improvement.

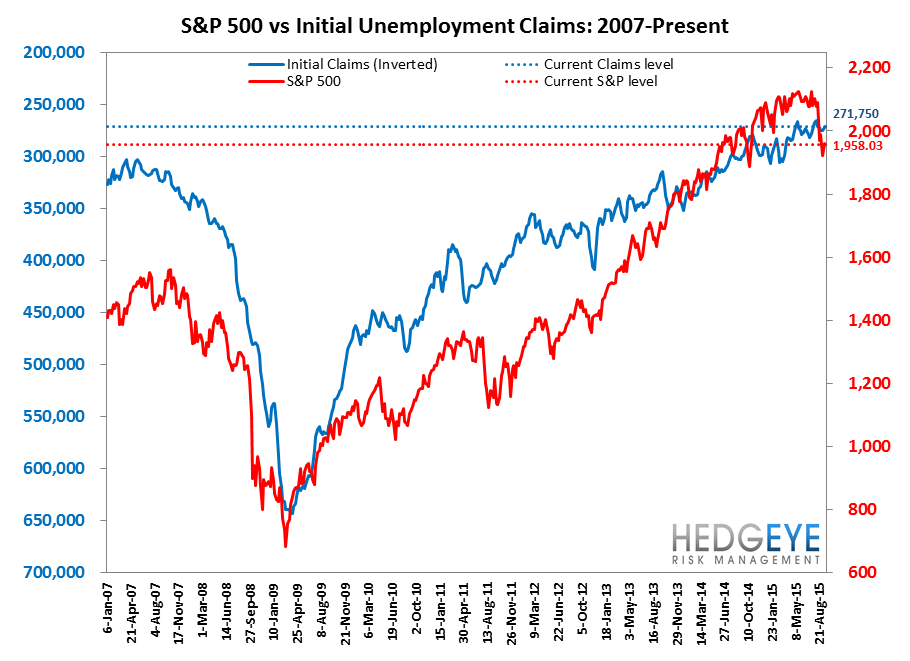

As we’ve highlighted, Initial Jobless Claims have been the most consistent, lead labor market indicator for the economic cycle with peak improvement occurring ~7 months ahead of the economic cycle peak and coincident with or slightly ahead of the equity market peak.

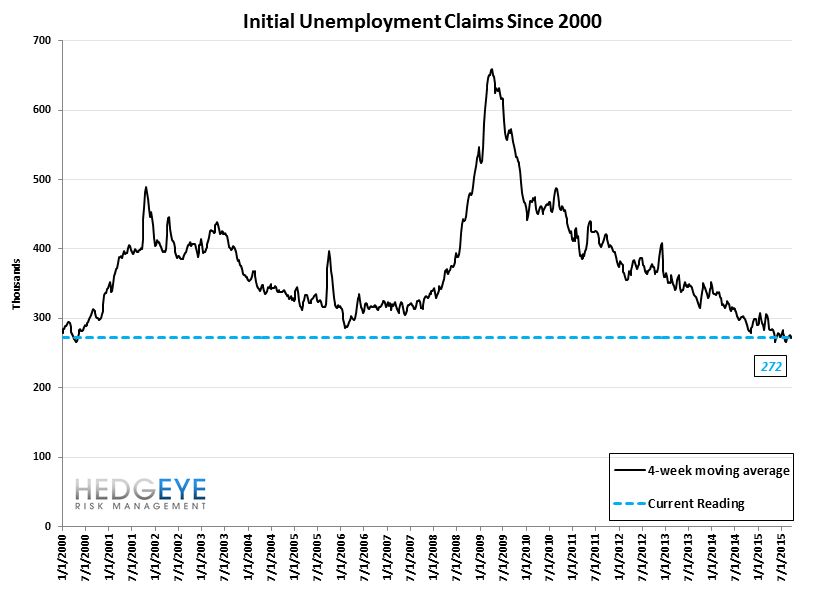

As it stands, rolling claims peaked 7-wks ago and while +267K in the latest week remains strong (and largely free of holiday related noise), from a rate-of-change perspective, growth will continue to converge towards 0% over the next couple months as we traverse trough comps. From there, monitoring marginal changes becomes a lower-intensity proposition as positive growth signals deterioration, at the margin.

In short, the labor market data remains trend consistent and somewhat of an insular island of strength and while there remains some modest runway left for further improvement, the late-cycle clock tick is getting louder.

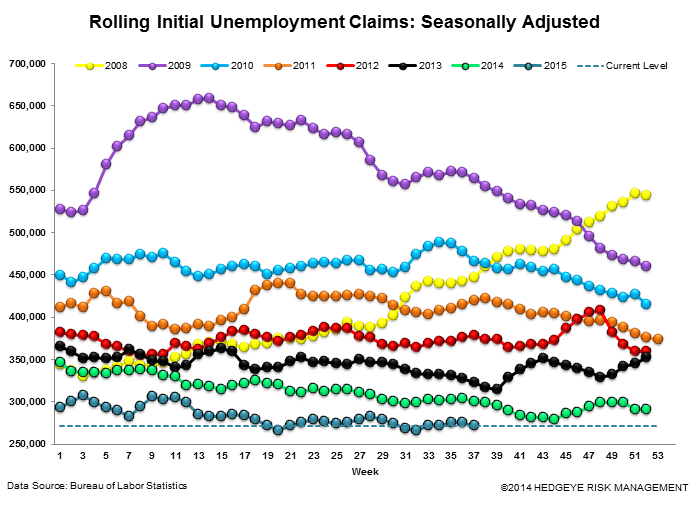

Looking across the energy states, indexed claims in the chart below increased week over week from 94 to 96 while the index for the whole country fell from 84 to 81 in the period ending September 12. The spread between the series increased from 10 to 15.

The Data

Initial jobless claims rose 3k to 267k from 264k WoW. The prior week's number was unrevised. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -0.75k WoW to 271.75k.

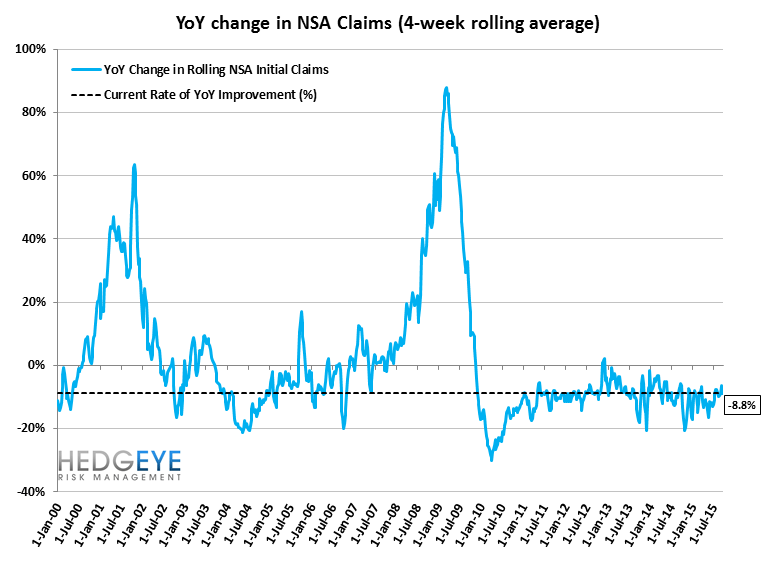

The 4-week rolling average of NSA claims, another way of evaluating the data, was -8.8% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -9.0%

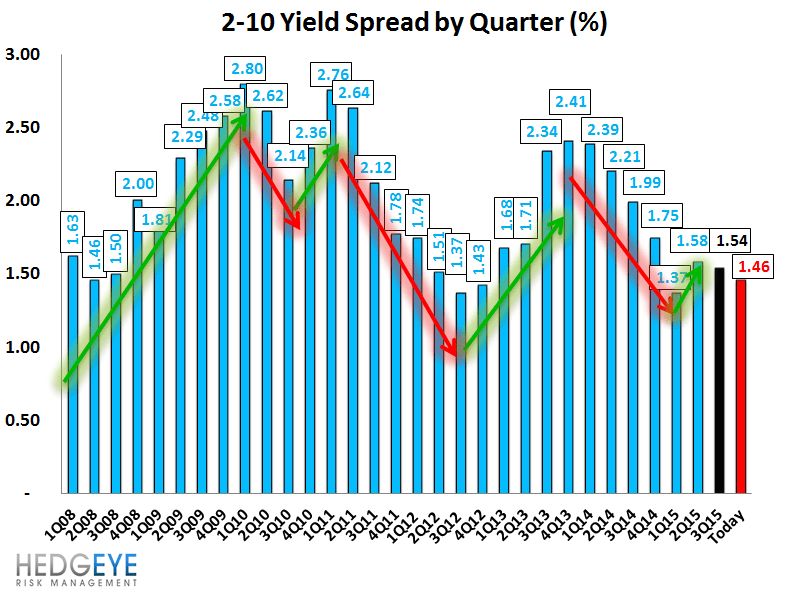

Yield Spreads

The 2-10 spread fell -3 basis points WoW to 146 bps. 3Q15TD, the 2-10 spread is averaging 154 bps, which is lower by -4 bps relative to 2Q15.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT