The increased stock market volatility is overshadowing fundamentals in the Consumer Staples space. Consistent with the Hedgeye Macro Team’s view of the overall market, style factors are currently playing a big role in performance and will likely be a factor as 3Q15 comes to a close. According to the Hedgeye Macro Team, the style factors that should continue to get you paid into the quarter-end are:

- Low-Beta, Big Cap (Equities)

- Long Duration Government Bonds

- U.S. Stocks That Look Like Bonds

In the Consumer Staples space the proof is in the numbers. In the consumer staples sector large cap/low-beta names, for the most part, have been some of the best performing companies. Consistent with this thesis on the LONG side we like GIS and LNCE. Unfortunately, our WWAV long is painful, but the HAIN SHORT feels much better.

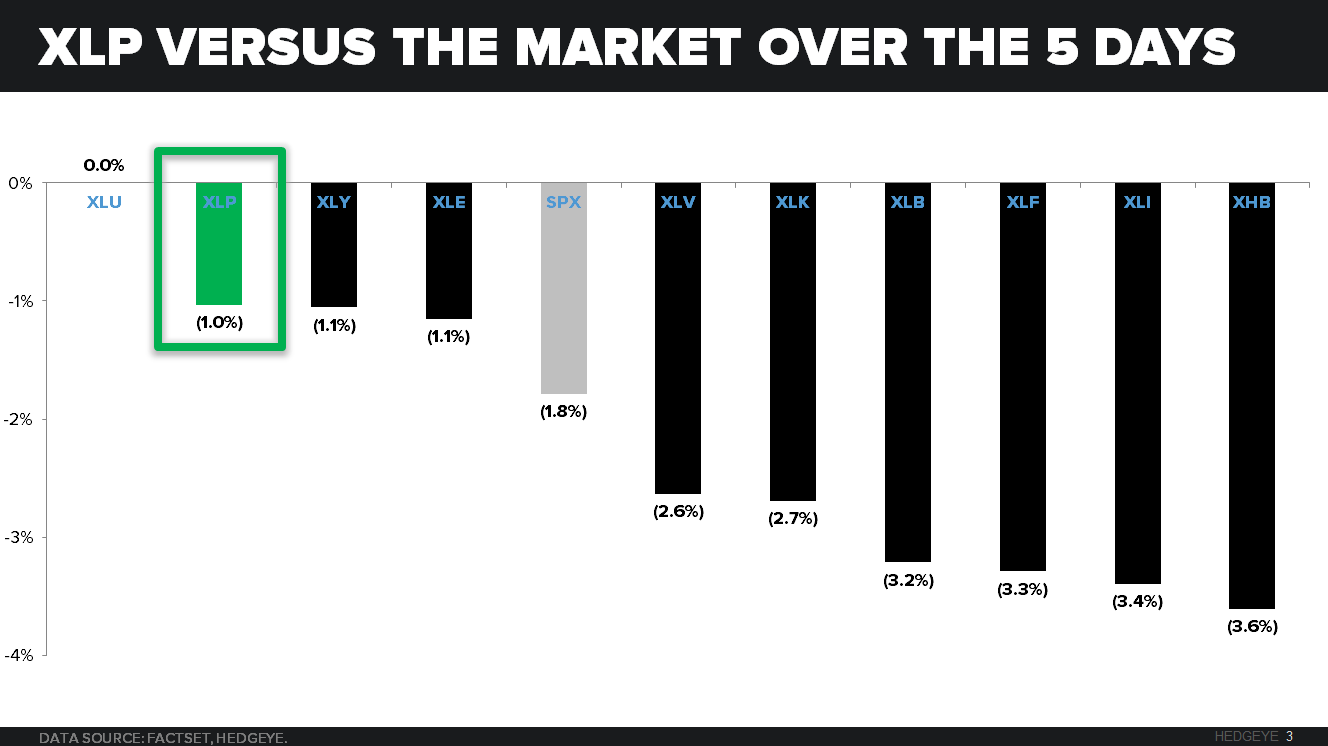

In a flight to safety environment, Consumer Staples will likely continue outperforming. Year-to-date, Consumer Staples has outperformed the S&P 500 by 260bps. Over the last five days, as you see below, the XLP has outperformed the entire market except for XLU.

While on a relative performance the XLP is outperforming the stock market as whole, stocks still look expensive. The XLP is currently trading at 11.38x EV / NTM EBITDA, well above its five year average of 9.77x.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst