Below are our analysts’ updates on our thirteen current high conviction long and short investing ideas. If nothing material has changed in the particular name, the analyst has made a note of this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or les

IDEAS UPDATES

TLT | EDV | GLD

No rate hike.

Both of our macro team's calls, "slower-for-longer" and "lower-for-longer" were acknowledged by your central planners (downwardly revised GDP expectations on Thursday). The result…Treasury yields fall and gold catches a bid.

Gold went on to finish the week +3.1% while TLT reversed its losses from earlier in the week to finish +0.2% (EDV +0.55%). As growth and inflation continue to slow, Treasuries and cash are a safer allocation than rolling the bones in the equity market over the last month.

Some perspective. Since the August 19th FOMC dovish minutes release from the July meeting, the S&P 500 Index has lost -6.2%.

Bad news is bad news? This is new.

The scary thing for equity markets is that the Federal Reserve is having less and less of a “Save the Day!” affect. Central planners lose the power to ease when rates are already 0%. Market participants are questioning the Fed’s ability to arrest the gravity embedded in late-cycle slowing (sound like a familiar narrative?) In other words, the market finishing lower post- save-the-day-dovish turn is the new.

While both the Dollar (Down) and the US Stock Market (Up) have been discounting that the Fed would be forced to punt, that doesn't change the reason WHY they punted. Growth is slowing:

This week’s data:

- Industrial Production: +0.9% YY and -0.4% m/m for August (underwhelming)

- Capacity Utilization: negative Y/Y for the 4th consecutive month, printing -0.6% for August (Awful)

- Retail Sales: Slowed on a M/M and Y/Y basis (+0.2% M/M and +2.2% Y/Y) but accelerated on a 2Y basis (Underwhelming)

Slower (and Lower) For Longer remains our non-consensus call. It's nice to see that the Fed is finally starting to see what the #GrowthSlowing late-cycle data does.

- GROWTH: is #LateCycle and will be slower (again) in Q3 than it was in Q2

- INFLATION: misreported, yes – in the area code of the Fed’s 2% “target”, no

In the press conference recall that Yellen said the Fed won’t raise rates until “inflation is at 2%.”

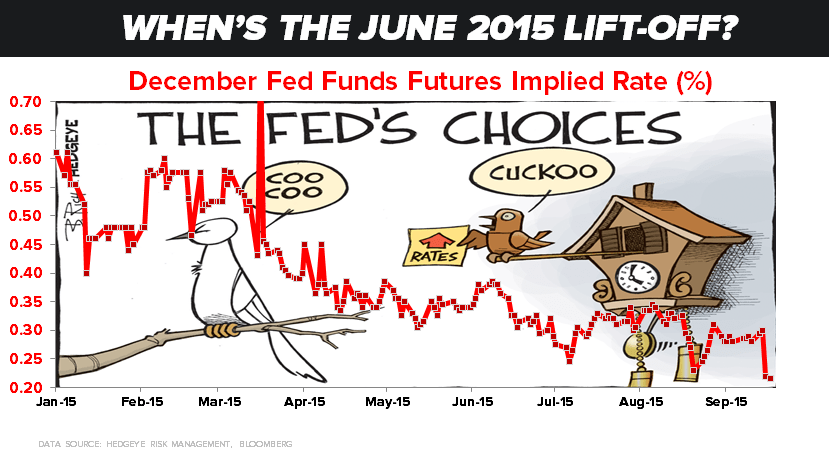

No September hike? What about December?

Our estimate for Y/Y% GDP for Q3 is a range of 0.1% to 1.5%. Even the Q/Q SAAR # that consensus hangs on will be comping against a 3.7% Q/Q SAAR GDP print (second revision). Good luck positioning for a rate hike. Prepare for the fade…. AGAIN.

Just take a look at the markets expectation for a rate cut. Here’s a chart of December federal funds futures (implied rate %):

ZOES

Zoës Kitchen has been tricky from an investment standpoint. Over the last three months, the stock has been hit alongside other small-cap universe names. However, in the spirit of Investing Ideas, we believe you have to take a long term approach to this name. We still remain very bullish on the concept here, the fundamentals, and we believe the dip represents an excellent buying opportunity for longer-term focused investors.

The company's management just presented at the Stifel Consumer Conference. Their presentation added further confirmation to our LONG stance. The company is growing the way a restaurant company should, with a strong beachhead in Texas, flanking out from there.

In the chart below you can see their current footprint and (more importantly) the white space available for future expansion.

ZBH

To view our analyst Tom Tobin's original report on Zimmer Biomet CLICK HERE

Our short in Zimmer Biomet is based on a number of interconnected themes and datasets. Eventually, a stock price will reflect a company’s ability to grow their revenue and profits and cash.

But a great theme or story is only that, a story about the future. And when you are in a debate about the future, the winner of the debate is the one with the stock working their way.

The wisdom of the markets is often accepted out of hand and accepted as proof of how smart you’ve been (or dumb). So, while our themes and data behind our ZBH short remain 99% identical to when we first presented the short idea six months ago, we certainly don’t think we should be raising the victory flag just because the stock went our way.

When we take a step back and ask what made our ZBH short work, the best explanantion has been the simplest one; the market went down. Because ZBH price and multiple is so highly correlated (found using Macro Monitor) with the S&P 500, we didn’t need our thesis to play out in order for us to win.

Janet Yellen explained on Thursday (what our macro team has been saying for months) that growth is slowing. Right or wrong, the market thinks this is bad news for ZBH. To what extent will be the next debate given that orthopedic demand can be driven by economic growth.

So, as our long term thesis on ZBH plays out in the coming years, we’ll be sensitive to our blind spots. But in the short term, we won’t turn away success either.

RH

To view our analyst's original report on Restoration Hardware: CLICK HERE

One of the most significant developments with Restoration Hardware right now is the return of Square Footage Growth.

Restoration Hardware went from over 100 stores pre-recession (and before having a defendable merchandise, real estate strategy, and an actual management team) to 67 in the latest quarter as it culled bad locations.

Square footage grew on occasion over that period in a given quarter, but has settled in around 850k. Starting in 3Q, we should see square footage growth ramp from a mid-single digit rate in 2Q to a number ~20%, then steadily march towards 35%+ in FY16.

Then we’ve got 20%+ square footage growth every year thereafter for at least five years based on our real estate analysis.

Fundamentally and financially, we’re about to see growth at RH go on a multi-year tear.

WAB

Our Industrials Sector Head Jay Van Sciver sent a stock report on his bearish Wabtec thesis to subscribers Friday afternoon. Click here to read the report.

FNGN

Our Financials Co-Sector Head Jonathan Casteleyn has no new, material update on Financial Engines this week. Below is his update from last week:

Financial Engines' fundamentals are solid as we expect strong 3Q15 net fund raising, a continuation from solid 2Q results, sourced by ongoing marketing campaigns in the quarter.

While market depreciation will be a drag (depending on exactly where beta returns shake out), we remind investors that the company is still in the seasonally strongest part of the year for AUM wins as marketing campaigns are most active in the middle two quarters historically.

Our research shows that the stock's return has been positive every 4th quarter calendar period since coming public with an average return of 22.6%. This stronger performance should carry through to the beginning of 2016 as the company prepares for the Wells Fargo catalyst (we calculate a $0.11 per share earnings opportunity as WFC starts to provide the firm's advisory services).

With a recent 2 standard deviation move in the company's valuation, but no fundamental change in our estimated $1.3 trillion in assets-under-contract (AUC) opportunity, we highlight mean reversion providing a rebound in the stock price.

LNKD

Our Internet & Media analyst Hesham Shaaban has no new, material update this week. Below is his most recent update from last Saturday. To view his original report on LinkedIn: CLICK HERE

We just received our first 3Q15 update to our LinkedIn tracker. This tool gauges the strength of the selling environment for LNKD’s salesforce. Our tracker is suggesting that the selling environment is not only improving, but doing so at an accelerating rate into 3Q15; suggesting that the organic guidance cut on LNKD’s last earnings release was not the result of any negative inflection in LNKD’s fundamental prospects.

We remain long LNKD into its next earnings release.

We’re expecting a clean beat and raise, which we expect will be a positive catalyst for the stock, especially given the current dearth of good Internet longs.

PENN

Penn National Gaming continues to be our favorite Regional Gaming stock.

Regional numbers for August have come in soft, but we predicted the August weakness. September revenues should rebound and serve as a catalyst for the stock going into Q3 earnings. On the research side we have not altered our views of PENN’s long term growth story. We continue to see more upside from current price levels.

GIS

Our Consumer Staples team led by Sector Head Howard Penney remains positive on General Mills heading into its critical 2Q15 earnings release and call next week.

We have been long GIS for the last six months and continue to have a favorable view of the company due to the following reasons:

- Sequential improvement in cereal

- Growth in Natural & Organic categories

- Snacking

- Cost cutting initiatives

- M&A activity

We will provide a more detailed update following next week's call.

MCD

To view our original note on McDonald's: CLICK HERE

McDonald’s remains one of our Restaurant teams Best Ideas on the LONG side. We continue to believe that 3Q15 will be the inflection point for the company’s turnaround and that we are going to be looking at a much different company 1-3 years from now.

Urgency has been instilled from the top down by new CEO Steve Easterbrook. He wants more speed and is encouraging people to get things done faster. The food and experience provided to the customer will greatly improve over the coming months as “Experience the Future” is implemented across the system. It won’t be instantaneous though, as MCD has a lot of work to do around changing the perception to bring back customers it may have lost.

Things like "All Day Breakfast," responsibly sourced ingredients, and bringing back the value proposition will all lead to increased sales and customer satisfaction.

This company is too big to be completely fixed overnight. That said, management has the right plans in place. We are confident in where they are headed.

FL

We reiterate our view that Foot Locker remains one of the top shorts in retail.

The company hosted an analyst day exactly six months ago, with a new CEO at the helm and ran through its long term growth targets. During the Ken Hicks (former CEO) era, the company was focused on taking capital out of the model, improving productivity and boosting returns. Now the model is positioned on store and comp growth with little margin leverage left to squeeze out.

Financial Plan: FL’s prior goals were all about dramatic improvements in productivity and occupancy leverage by way of pulling capital out of the model (closing stores, changing banners, and eliminating working capital). But now FL is guiding to the following…

- Net square footage growth of 2%+ and mid-single digit comp growth on top of that.

- Even with an uber-long-term target year of 2020, the goal is only to take Gross Margins 30-80bp above 2014 levels. That’s not even 10bps a year. The point is…gross margins are peaked.

- SG&A is expected to come down from 19.9% to 18-19%. That’s extremely aggressive. We’ve never seen a retailer sustain a sub-20% level of SG&A – especially not one that will need to spend aggressively on e-commerce, growth in a new concept (six:02), and broaden its international reach. We’ll assume that the company will, in fact, be spending in these areas. But it is banking on a mid-high single digit comp to drive its SG&A ratio lower. We’re not comfortable making that bet.