We remain SHORT small-cap hamburger chains SONC, WEN and JACK. Expectations (and valuations) for those companies are not aligned with reality. SONC gave us a look at what happens to high-expectation stocks with even a slight miss and guidance that suggest 2-year sales trends will slow significantly. (Click HERE for our recent note on SONC)

Part of our LONG thesis on MCD, includes that the company will not be ceding anymore market share, especially with the “value” based customer. It’s our belief that all three domestic chains have benefited from MCD being a poorly managed company.

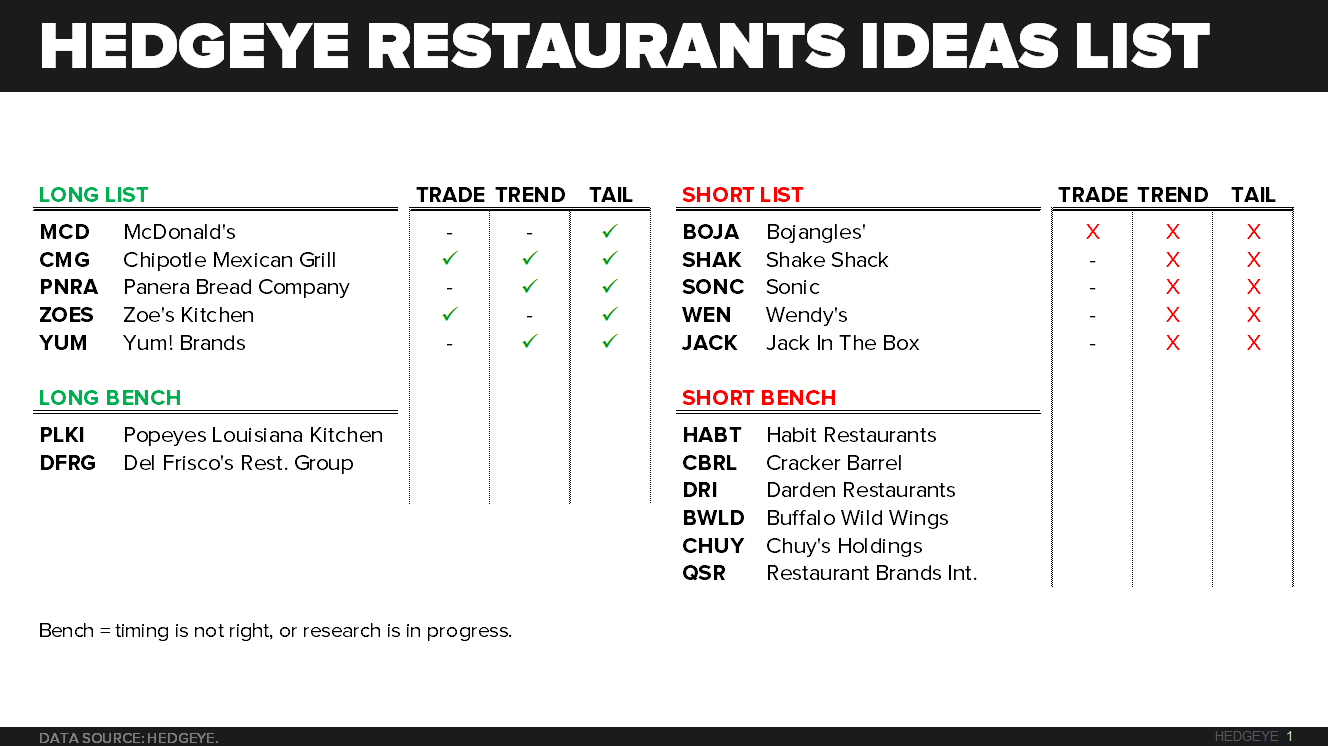

We specifically did not mention Restaurant Brands International (QSR) on this list because of the global nature of the Burger King business and the strong Tim Hortons brand. That being said the Burger King’s business in the U.S. will also be negatively impacted by a stronger McDonald’s. We also see the Burger King system having a very difficult time adjusting to higher minimum wage. The combination of low average unit volumes, excessive discounting and significantly higher debt levels at the franchisee level are all significant impediments to future profitability.

We are now adding QSR to the short bench, with an eye on taking it to the next level.

WHAT $15 MINIMUM WAGE MEANS FOR QUICK SERVICE RESTAURANTS

The move to $15 minimum wage will be a crushing blow to small independent Quick Service Restaurant (from this point forward, QSR will pertain to Quick Service Restaurant) operators and will be a negative for “asset light” franchisor stocks.

This note is not a political statement about what a “fair wage” is, it’s just math. And math is simple. To be blunt, without major structural changes, most small independent QSR operators will go bankrupt at $15 minimum wage. To avoid bankruptcy, the options are limited. Operators can raise prices and risk a decline in traffic and or the more likely scenario is to cut labor too drastically to maintain profitability.

The bottom line is that the QSR industry already operates on low margins and can’t afford to see labor costs increase by 50% or more.

As the CEO of CKE Restaurant, Andy Puzder's, says “if you increase wages in such a ‘draconian fashion,’ it takes away from the ability of businesses to absorb the increase in pricing and forces them to use labor more efficiently or resort to automation, resulting in the loss of jobs.”

You can read Mr. Puzder’s WSJ op-ed piece HERE

In the table below we run thru a hypothetical (but close to reality) scenario analysis of a typical QSR restaurant doing average unit volumes of $1.2 million, $1.4 million and $1.6 million. As you can see in the table on the left, the industry already operates under very thin margins.

On the right side of the slide, is the impact on profitability of taking minimum wage up to $15 per hour. What this analysis does not contemplate is the Andy Puzder scenario of pricing a significant reduction in the number of jobs and the impact of new technology (automation) on profitability.

We did a separate analysis for MCD since it has average unit volumes significantly higher than other competitors. Even MCD is not immune from a significant decline in profitability and franchisees only cover the royalties by a modest amount.

While this is devastating personally for crew workers and franchisees, the franchisors are not immune to the impact. Given significantly higher labor costs, a store averaging $1.4 million would need to increase volumes by 55% to $2.175MM in order to return the labor margin back to where it started. Since this is impossible to do, operators will be required to seek alternative strategies to run the restaurant.

As we see it the impact is twofold. First, marginally profitable stores will be closed, and second, even the profitable stores will not be able to pay the required royalties.

Bottom line, at $15 minimum wage, the TAIL thesis for being short the high multiple, highly leveraged, “asset light” darling restaurant stock becomes very clear. First, the recurring cash flows (royalty payments) begin to dry up. Then, over time massive leverage on the balance sheet of these companies becomes the noose around the neck and they will probably have to deal with franchisees going bankrupt. If $15 minimum wage becomes a reality, the descent is just beginning for these stocks, and it will be an ugly landing.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst