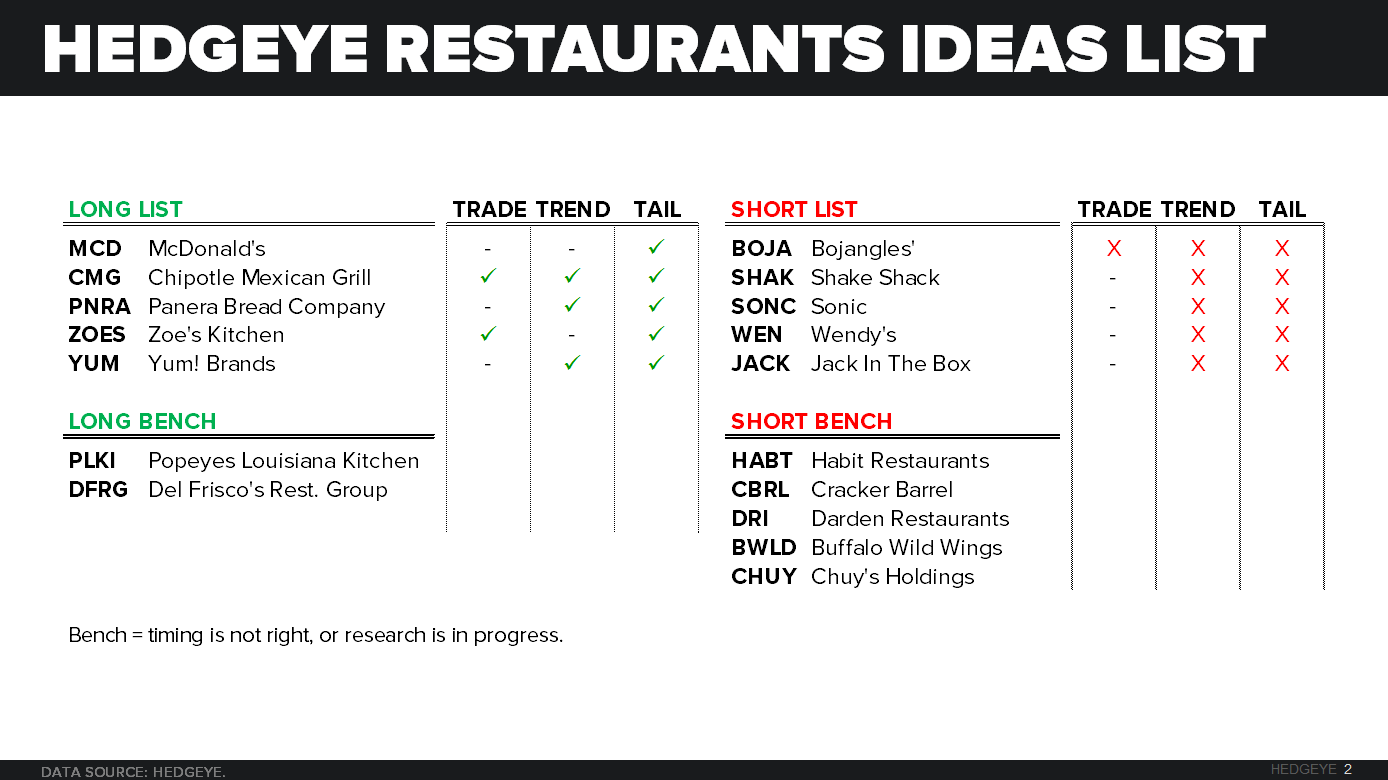

Sonic Corp (SONC) is on our Hedgeye Restaurants Best Ideas list as a SHORT.

On Monday September 14, 2015, SONC announced Same-Store Sales (SSS) growth for fiscal year 2015 of 7.3% as well as the date of their earnings call, which will be Monday, October 19, 2015.

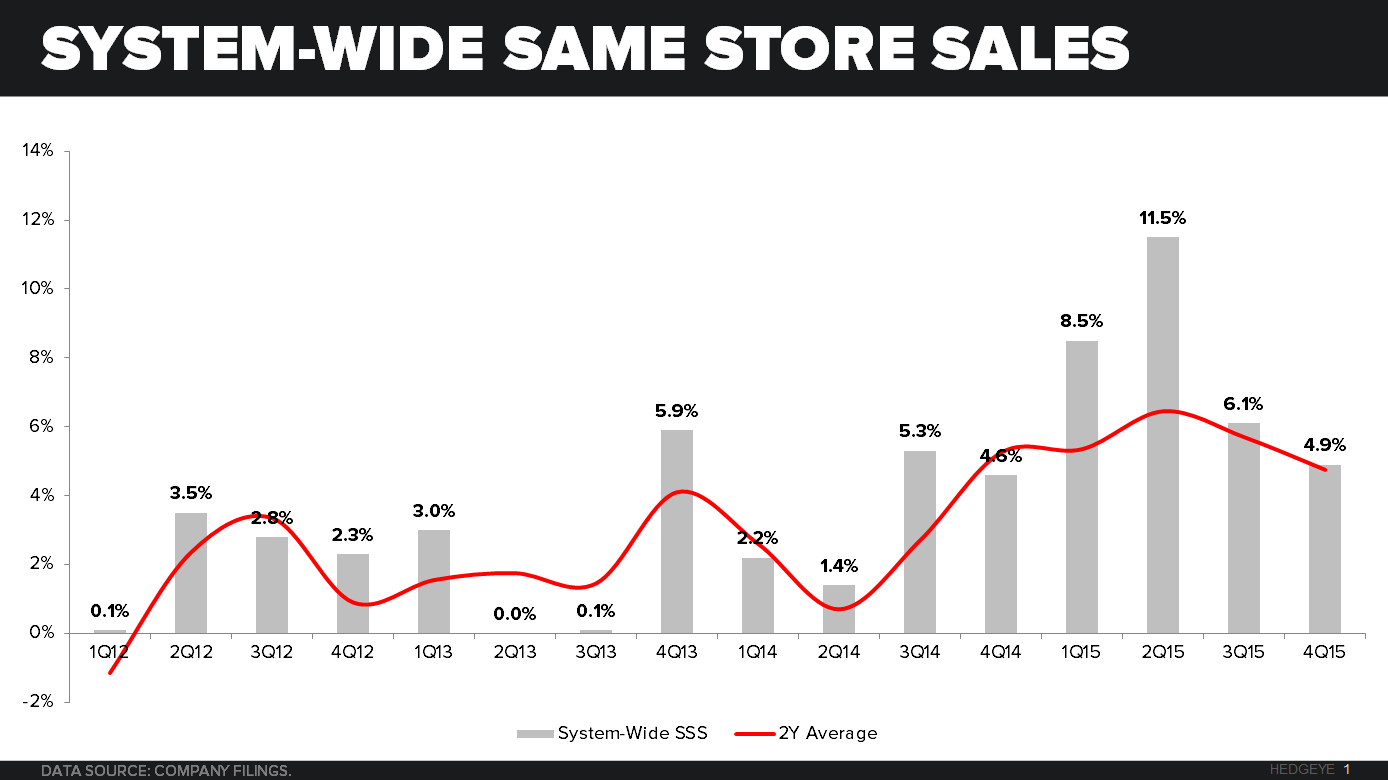

The company announced that system-wide SSS for 4Q15 were 4.9% versus consensus estimates of 5.5%. For the full fiscal year 2015 as previously stated system-wide SSS were 7.3% versus consensus estimates of 7.9%. The comp reflects 6.9% SSS growth at company drive-ins and 7.3% SSS growth at franchise drive-ins. These numbers show an initial slowdown from SONC’s recent strong performance, and as MCD regains its leadership position we expect this to become more apparent.

SONC is facing some tough comps in fiscal year 2016 especially in the first and second quarters. Management is expecting SSS growth for the system in the range of 2% to 4% for FY16 which aligns well with consensus estimates currently at 3.2% for the FY16. The company plans to open 50 to 60 new franchise drive-ins in FY16, in addition they have initiatives in place to improve margins by 75 to 125 basis points at their drive-ins.

Nothing from this release makes us feel less confident about our short position on the name. We believe that comps will erode over the next 12-18 months as MCD takes back market share that it has given up over the last few years.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst