Key Takeaway:

Risk parameters remain decidedly negative over the intermediate term, but appear to have struck a balance between positive and negative in the shorter term and longer term.

Notable events last week included the US Jobs report, which saw only 173k jobs added in August, less than the 220k expected and China's downward revision to GDP for 2014 to 7.3% from 7.4%. On the flip side, expectations for Chinese stimulus created some optimism and junk bonds saw a small bounce . Additionally, the FOMC meeting announcement coming this week added further uncertainty to the mix.

We continue to highlight China as our biggest concern with Chinese steel prices continuing to fall.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 3 of 12 improved / 1 out of 12 worsened / 8 of 12 unchanged

• Intermediate-term(WoW): Negative / 2 of 12 improved / 5 out of 12 worsened / 5 of 12 unchanged

• Long-term(WoW): Negative / 2 of 12 improved / 2 out of 12 worsened / 8 of 12 unchanged

1. U.S. Financial CDS – Swaps tightened for 16 out of 27 domestic financial institutions with an average move of -1 bps tighter.

Tightened the most WoW: AXP, MS, MTG

Widened the most WoW: SLM, MET, ACE

Tightened the most WoW: CB, ACE, ALL

Widened the most MoM: SLM, WFC, MET

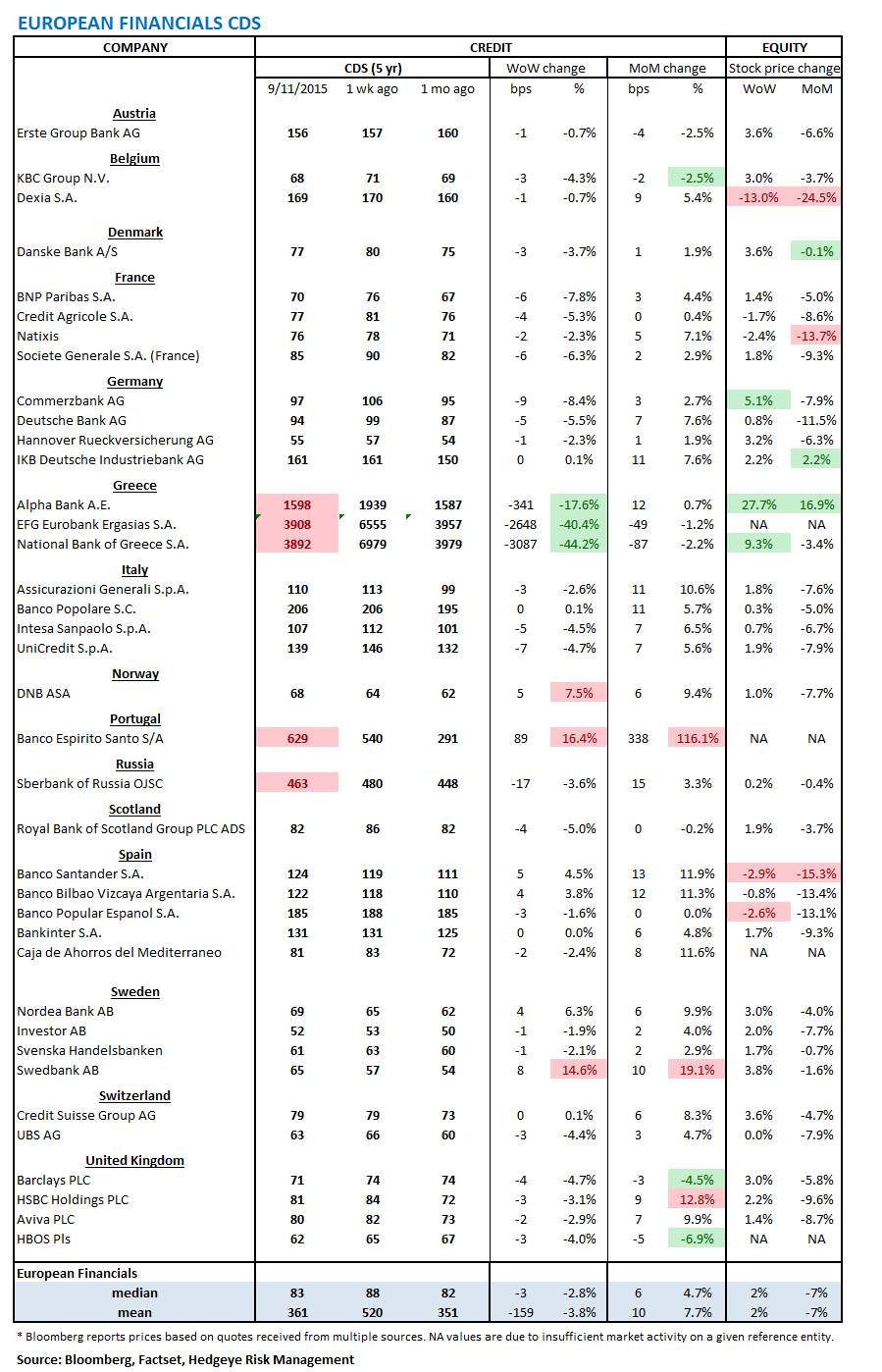

2. European Financial CDS – Swaps tightened for the most part in Europe last week. The median move was a -3 bps, while Greek bank CDS were outliers, tightening between -341 bps and -3087 bps.

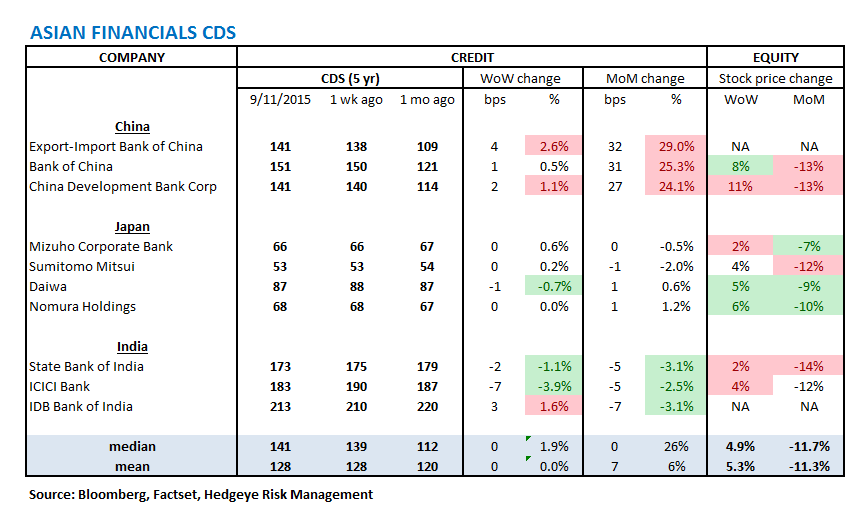

3. Asian Financial CDS – Swaps for Chinese banks widened between +1 bps and +4 bps last week as the country revised its 2014 growth rate down from 7.4% to 7.3%.

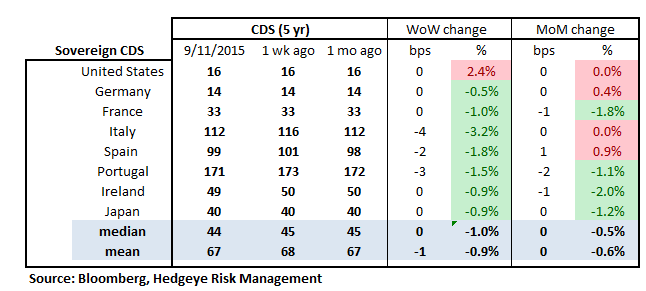

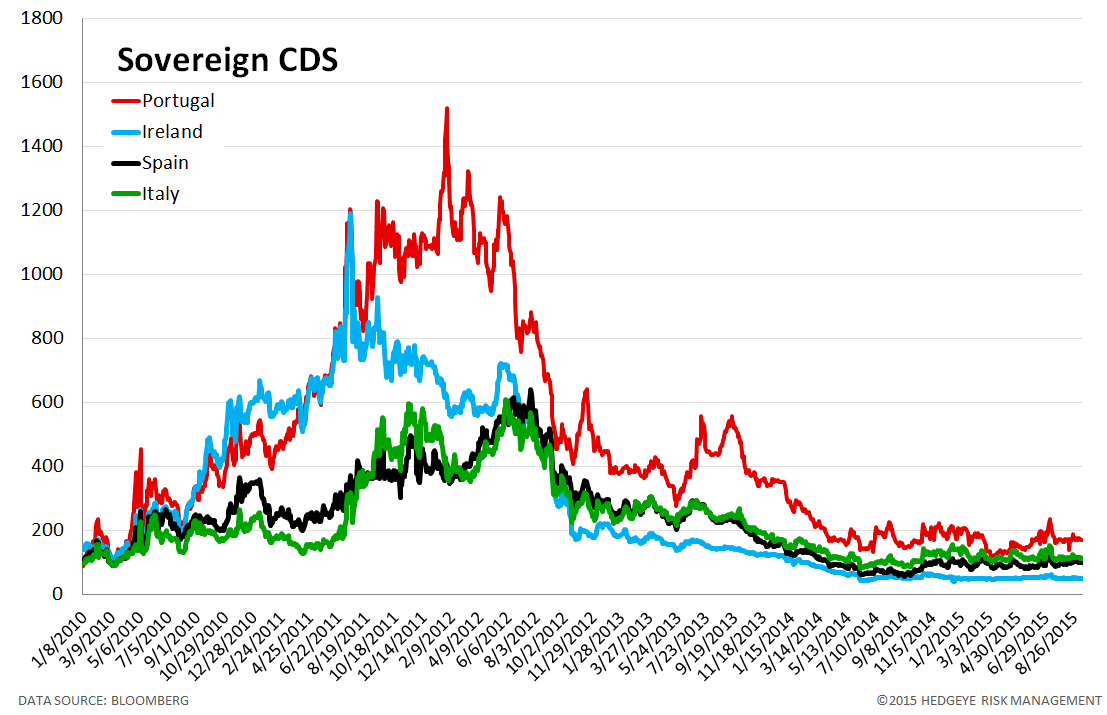

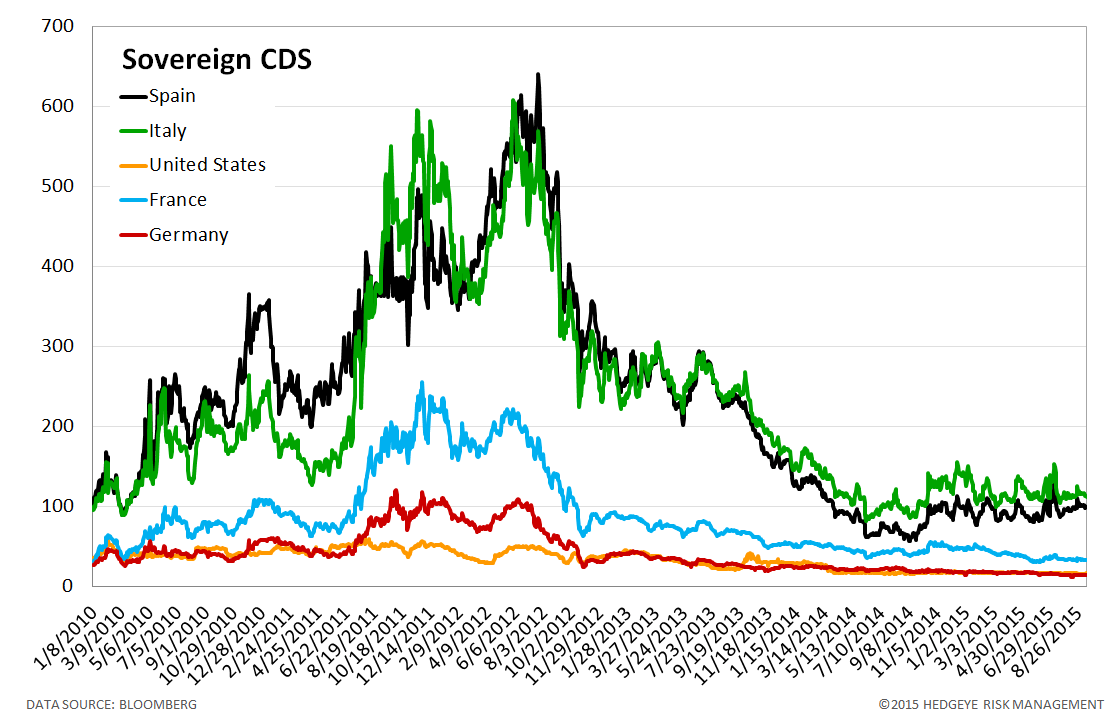

4. Sovereign CDS – Sovereign Swaps were flat to tighter last week. Italian sovereign swaps tightened the most, by -4 bps to 112.

5. Emerging Market Sovereign CDS – Emerging market swaps were mixed last week. Brazilian sovereign swaps widened by 16 bps to 395. Meanwhile, Russian swaps tightened by -15 bps to 370.

6. High Yield (YTM) Monitor – High Yield rates fell 7 bps last week, ending the week at 7.09% versus 7.15% the prior week.

7. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 5.0 points last week, ending at 1870.

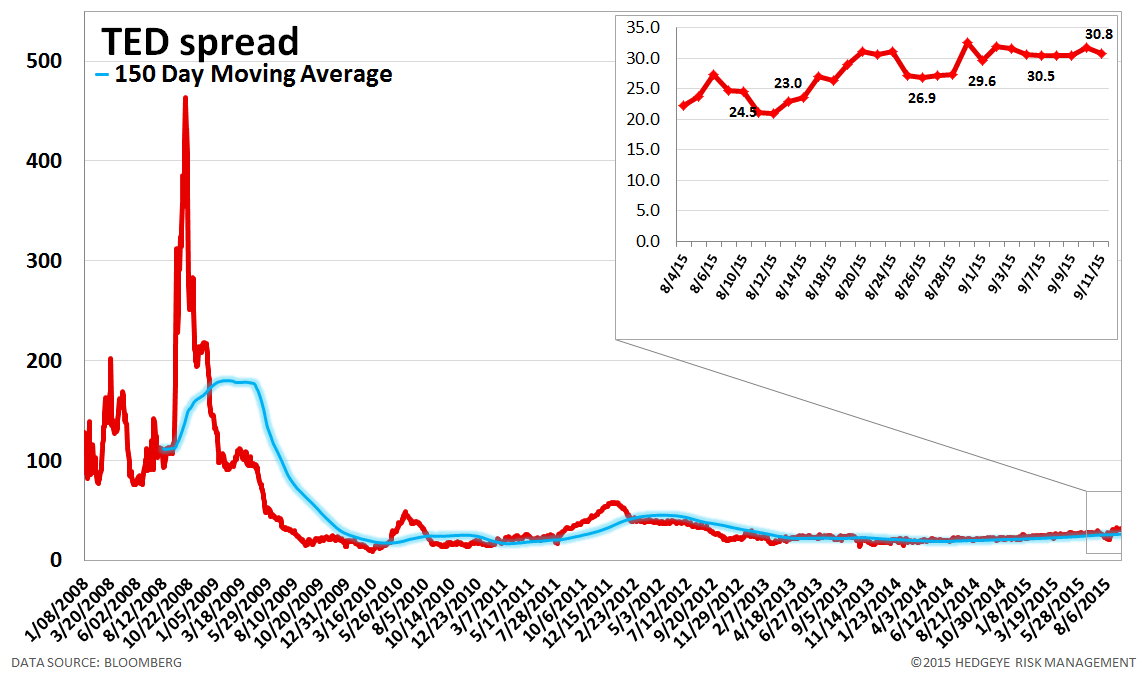

8. TED Spread Monitor – The TED spread was unchanged last week at 31 bps.

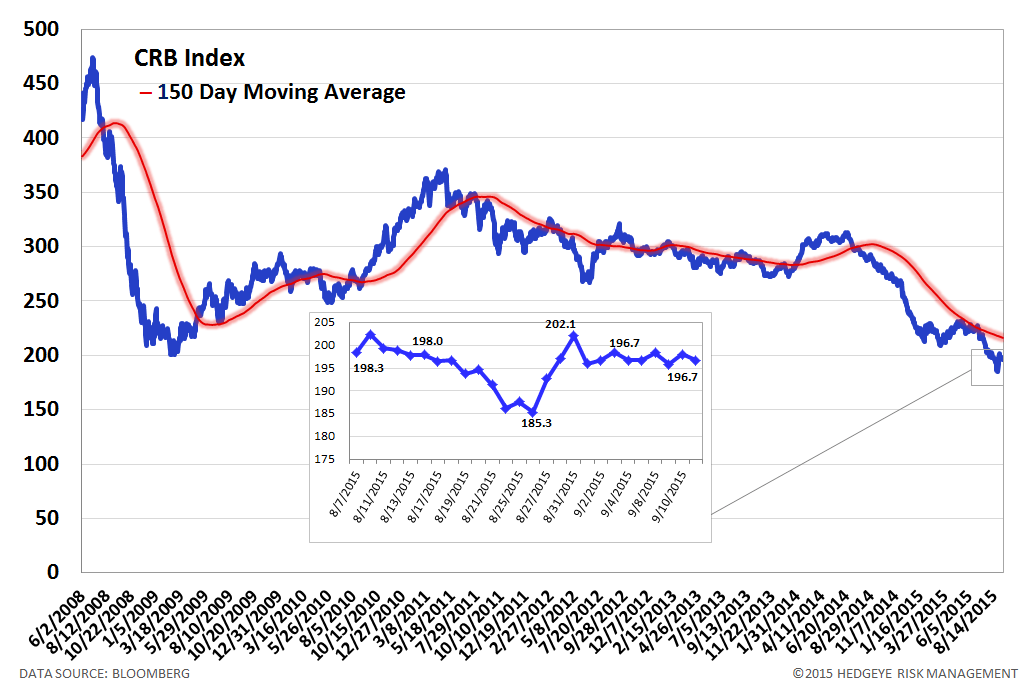

9. CRB Commodity Price Index – The CRB index was unchanged last week at 197. As compared with the prior month, commodity prices have decreased -0.6%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was unchanged at 10 bps.

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index fell 13 basis points last week, ending the week at 1.90% versus last week’s print of 2.03%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

12. Chinese Steel – Steel prices in China fell 1.5% last week, or 35 yuan/ton, to 2225 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread widened to 148 bps, 7 bps wider than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 2.7% upside to TRADE resistance and 4.5% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT