We are removing KKD from the LONG bench. The company reported a very challenging quarter last week and provided little guidance that suggests that the issues they face are one time in nature.

RECENT NOTES

9/01/15 MCD | ALL DAY BREAKFAST IS OFFICIALLY LAUNCHING ON 10/6

8/28/15 ZOES | Entering the Big Leagues

8/24/15 SBUX | DO THE NEW FOOD OFFERINGS DRIVE INCREMENTAL TRAFFIC?

RECENT NEWS FLOW

Friday, September 11

KKD | Announced it has signed a development agreement with Fraliment S.R.L to open 12 Krispy Kreme shops in Bolivia over the next five years (click here for article)

CMG | Linked to salmonella outbreak in Minnesota (click here for article)

LOCO | Continued south Texas expansion with new location in New Pharr (click here for article)

SBUX | Mobile order and pay to be rolled out nationally to all locations by the end of September (click here for article)

Wednesday, September 9

KKD | Reported 2Q16 results, earnings per share ex-items was $0.15 versus FactSet estimates of $0.18. Revenue came up short of estimates as well, reporting $127.3mm versus consensus of $131.2mm. Same-store sales were +2.3% versus consensus of +2.6%, due to this poor performance management lowered full year EPS guidance down to $0.76 - $0.80 versus previous guidance of $0.80 - $0.85 (click here for press release)

MCD | Announced it will fully transition to cage-free eggs in the U.S. and Canada over the next 10 years (click here for article)

JMBA | Increases share repurchase program to $45mm (click here for article)

Tuesday, September 8

PLAY | Dave and Buster’s reported a great 2Q15, led by an 11.0% same-store sales built up by 12.1% increase in walk-in sales and a 2.2% increase in special events sales. Due to the strong numbers management is raising guidance, total revenues are now expected to be $844mm to $853mm versus previous range of $822mm to $831mm (click here for article)

PBPB | Announced a $35mm share repurchase program (click here for article)

DNKN | Named Michael Shutley Vice President, Federal & State Government affairs (click here for article)

SECTOR PERFORMANCE

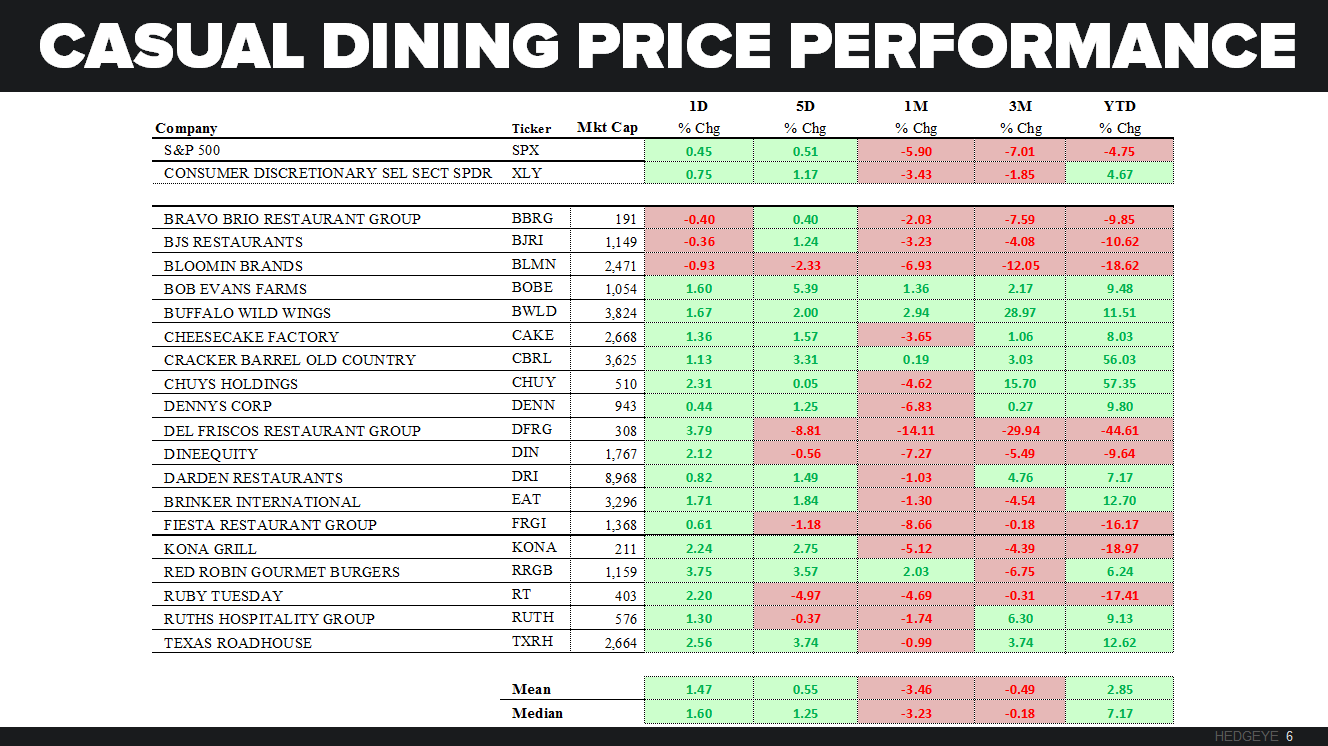

Casual Dining and Quick Service stocks that we follow widely outperformed the XLY last week. The XLY was up +1.2%, top performers on a relative basis from casual dining were BOBE and TXRH posting an increase of +4.2% and +2.6%, respectively, while SHAK and PBPB led the quick service group this week up +13.4% and +7.8%, respectively.

QUANTITATIVE SETUP

From a quantitative perspective, the XLY looks bearish from a TRADE and TREND perspective, TRADE support is 73.19.

CASUAL DINING RESTAURANTS

QUICK SERVICE RESTAURANTS

Keith’s Three Morning Bullets

Bets continue to mount on a Dovish Fed meeting…

- USD – US Dollar Index closed on its low for the wk (-1.1% on the wk) and is seeing follow through selling this morning vs. both Euros and Yens – what’s most interesting about this to me is that on 30-day correlation, SPX has a POSITIVE correlation to USD of +0.8 (meaning a Dovish Fed could be bad for stocks)

- JAPAN – Down Dollar is definitely bad for Japanese Stocks – that INVERSE correlation has not changed; Yen +0.3% took another -1.6% out of the Nikkei overnight – it’s -12.5% in the last month with the US Dollar -2.7% (and Yen +3.8%)

- UST 2yr – yield tested a “breakout” above 0.75% for the 6th time in 6 months last wk… and failed; back down to 0.71% on Dovish Fed spec this morning and, with Fed Fund Futures this low, I still think the Fed could train wreck macro markets if they tighten

SPX immediate-term risk range = 1; UST 10yr Yield 2.13-2.24%

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst