This unlocked research note was originally published September 10, 2015 by Retail Sector Head Brian McGough and his team. For the record, McGough's team added Lululemon (LULU) to its Best Ideas list on 6/15/14 at $37.61 and removed it on 3/24/15 at $63.30 for a 68.3% gain. If you are an institutional investor interested in learning more about how you can subscribe to our research please email sales@hedgye.com.

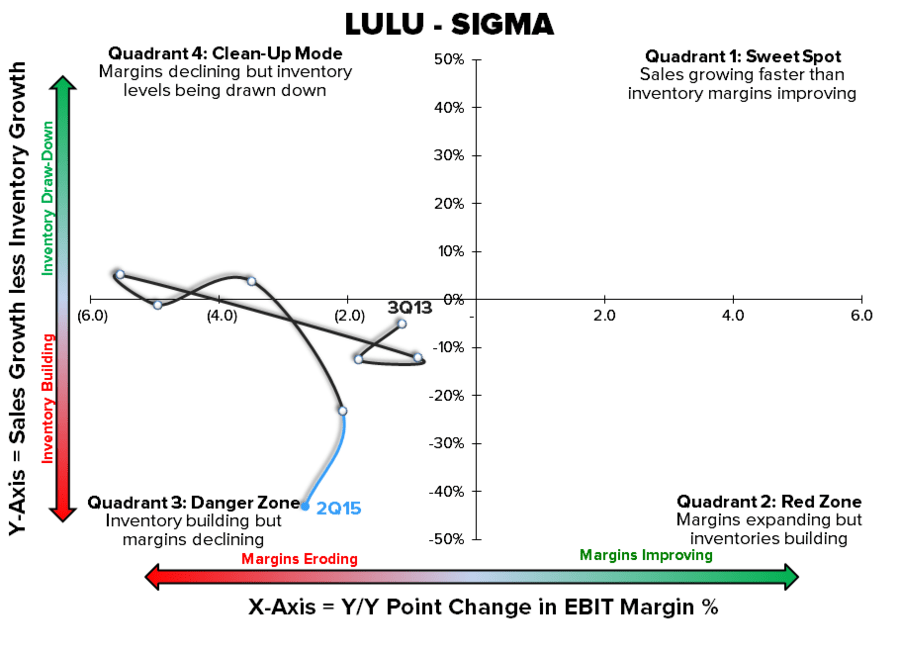

There’s one major reason why we think this LULU quarter was a huge let down -- and it’s not that inventories were up 23 days while Gross Margins missed by 200bps. Nor is it that LULU added $62mm in revenue year over year, but generated $1mm less in EBIT. It’s the reality that this company does not know what it wants to be. Virtually every statement out of management on the call had to do with near-term tactical branding, marketing and product plans. All that is fine. It matters on some level – and definitely matters to small scale moves in the stock in the coming quarters. But that’s what we call TREND (in HedgeyeSpeak that translates to 2-3 quarters out – the near-term modeling horizon). This is where LULU lives, unfortunately.

But LULU needs a change of address. This is an extremely powerful brand in a solid, yet increasingly competitive, space. LULU needs to not only be a great brand, but a great company. Then and only then will it be a great stock. We think management is coasting on the power of the brand, by tweaking a legacy operating plan, blindly opening stores, and hoping that nothing else goes wrong. Hope, however, is not a profitable growth process.

LULU needs to live in the TAIL (which we define as 1-3 years). What we need for real wealth creation with this stock is for a clear, concise strategy that insiders rally around and are paid handsomely to implement. People need to look to $4.00 in earnings power, and believe in it. It’s that same strategy that would result in its CEO standing up and saying things that will make Nike, UnderArmour and Athleta quake in their boots (which used to be the case) – not that they are using ‘Sports Psychology on the Pant wall’. Unfortunately, we truly think that LULU does not have a proactive process to grow its business.

Does The Company Have A Long Term Plan?

Somebody, please, ask virtually anyone in the company if they know their market share in stores and online within an hour’s drive of each store. [Note: our math shows it ranges from 2.5% (Long Island) to 26.7% (Burlington Vt) -- ping us if you want the data]. We don’t think they’ll tell you – because they probably don’t know.

How can a CEO stand up and give credible growth and profitability targets without knowing these basic building blocks? How can they articulate why they don’t have a wholesale model – something that could be a home run for LULU (i.e. sell where the consumer shops)? Even the CFO, who we have/had high hopes for, hasn’t created his own identity with the Street – as he’s following the same script of his predecessor who was pushed out.

All we get from the company as it relates to strategic initiatives are 1) Brand, 2) Community, 3) Innovation, and 4) Guest Experience. The only quantified metric is that LULU will return to a 55% gross margin – something that we don’t think is realistic without meaningful backing by the balance sheet (i.e. more capex to boost profitability). But more importantly, the market is highly unlikely to pay for a passive goal to return to peak profitability when LULU is in a different stage of its growth cycle.

This is a great Brand, for the time being. We really want to get behind this story due to the potential that can be unlocked. But without the backing of a great company – we think this stock is going anywhere but up. We’re glad we pulled the plug in March.