Our FMHQ (Friday Morning Housing Quant) tables present the state of the publicly traded homebuilders in a visually-friendly, quantitative format that takes about 60 seconds to consume.

Quick Quant Takeaways:

- This week we're adding Taylor Morrison (TMHC), TRI Pointe Group (TPH) and Standard Pacific (SPF) to our list of builders.

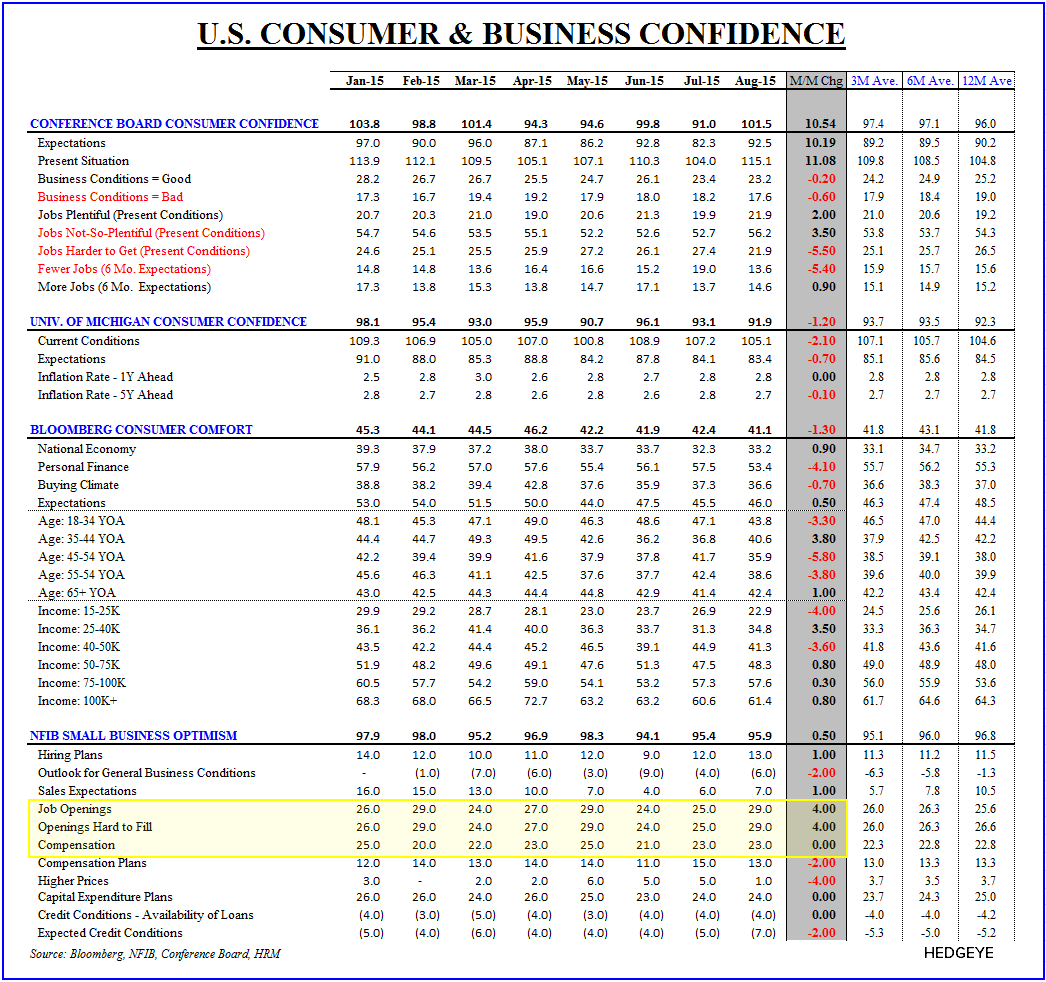

- Housing Macro: “Jobs Hard to Fill” | The domestic macro calendar was relatively light this week but we did get the NFIB small business confidence data for August. As a reminder, Small Businesses represent over 99% of total U.S. Employer firms and >60% of net private sector hiring on a monthly basis – and sentiment around the current and forward prospects for business activity are discretely related to hiring activity and labor compensation trends. Notably, the NFIB’s “Jobs Hard to Fill” sub-index rose +4pts sequentially to match its highest level in the post-crisis period. In the housing sector, as we highlighted last week, with both resi construction employment and hourly wages growing at approximately 2x the broader averages, tight labor conditions in the sector continue to manifest. The latest survey data from the Associated General Contractors (see AGC/WSJ figure below) lends further support to the tight supply view as a majority of firms are reporting difficultly in hiring employees across all the principal trades.

- Performance Roundup: The mean/median QTD returns for the 14 homebuilders in the tables below are -5.3% and -4.9%, respectively. This compares with the S&P 500 being down -5.4% QTD, so roughly in-line. The broader Housing complex, however, is flat to up +2.6% QTD based on the ITB, XHB and S15 Home Index. We think this comports with our call to de-emphasize the builders on a relative basis for 3Q in order to sidestep their seasonally weakest period. The best performance QTD continues to come from NVR (+15.5%) - one of the two builders we favored for 3Q15. The other was Toll Brothers, which is down -3.2% for the QTD. Hovnanian remains the worst performing builder this quarter (-24.4%), but has seen a big bounce in the last 5 days, rising +16.2% on earnings.

- Valuation: The cheapest names in the group currently are Meritage Homes (MTH) at 9.2x NTM earnings, Taylor Morrison (TMHC) at 9.6x and TRI Pointe Group (TPH) at 9.7x.

Joshua Steiner, CFA

Christian B. Drake