The company filed an 8K in conjunction with its presentation today. A couple quick thoughts…

1) No change in guidance. It’s pretty safe to say that if business has been trending down, or was negative in any way, shape, or form, then KATE would have been obligated to disclose that in this 8K. Given how the stock has been trading, this is critical.

2) The company gave additional information related to store count and square footage in the US vs. Int’l. This might sound like a ‘who cares’ event, but given the poor level of disclosure at KATE, it is a step in the right direction.

3) Similarly, the company provided new information as it relates to the size of Jack, and Saturday, as well as the top line impact of its efforts to improve Quality of Sale. Does any of this allow us to build a more accurate 2017 model for units, productivity or margins? No, but it offers up some clarity for people who are scratching their heads wondering why the company is beating on comp, and yet missing on the top line. It won’t matter anymore after the 4Q report. But should stem some of the volatility in results until then.

No Change to Our Thesis

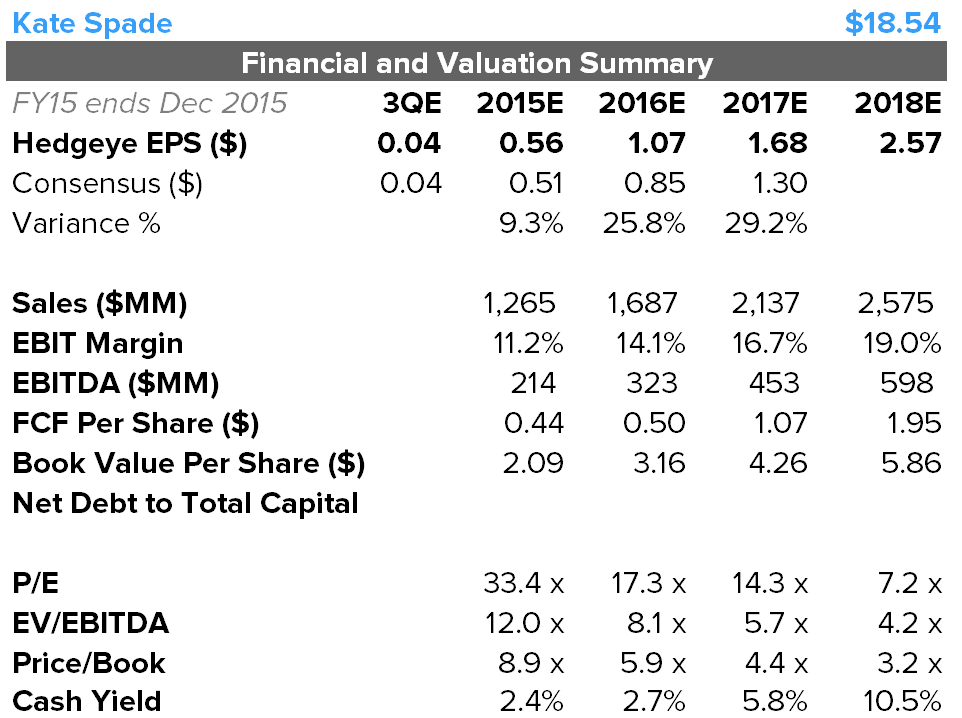

We Still think KATE’s top line will double and margins will go from 6.6% last year to the high teens in three years’ time. All in, we’re looking at better than $2.50 in earnings for a stock that can’t seem to stay above $20. The CAGR needed to get to $2.50-$3.00 is well north of 50%, and yet the stock is trading at a high teens multiple on next year’s $1.07. This is a company that hasn’t meaningfully turned a profit since 2008, and once people get visibility into 2016, we think that investor sentiment around its growth and profitability will turn up substantially. This is a name that could, and should double by the end of next year. KATE remains one of our top picks in retail.