“It’s one way in, it’s one way out.”

-Jake Owen

For those of you country music fans in the Hedgeye community (rock on Jumbo Cleaves!), you’re probably familiar with a hit song by Jake Owen called “Every Reason I Go Back.” That’s where you’ll find the aforementioned quote. It’s a #beauty.

Jake Owen, like me, can be considered a jock – or a knucklehead. We’re supposed to be subservient to the intellect of the establishment. But we’re not. And we like it.

Owen was an aspiring pro-golfer turned wake-boarder (turned blown-out knee somewhere in Florida). So he picked up the guitar, grew out the flow – and the rest is history. His 1st hit (#1 on the charts) was called Barefoot Blue Jean Night in 2011.

Back to the Global Macro Grind …

Gentlemen, do you wear jeans? How about jorts? Flannel? Flip Flops? Can you pivot between suits and tees? Or is it all about rocking the pocket scarf, all of the time? Ladies?

I personally don’t care what you look like. I couldn’t give a damn about what money you make (made) either. All I care about in life is who you are. You. The real you. The one who doesn’t change with money (or without). That’s character.

On our team, players who make excuses (when wrong) don’t make it. Something like this, for example: “We think much of the decline can be attributed to technical & systematic investors that are price-insensitive and largely indifferent to fundamentals..”

Really?

I didn’t hear you blaming your bull market returns on “systematic” chart chasing and bailout money printing. And how about those “fundamentals”?

Got #LateCyle, #Deflation, or Revenue/Earnings #GrowthSlowing? Even for a big time hedgie (you can look up who it is), solving for forward revenue and earnings growth is pretty fundamental (494/500 SP500 companies Q2 average rev/eps down -3%).

But I digress. After hearing about his “strategist” chirping my clients that “the market is going up from here” at ISI idea dinners throughout Q2, I had to call him out. It’s fine. He calls me out. He actually fired me for being right. And I liked that too.

In our risk management process, on the big stuff (growth and inflation), the cycles are both measurable and glacial. That means they take time to play out. It’s one way into a cycle peak, and only one way out. #Slowing

It’s really not that complicated. What complicates Wall Street’s narrative is the excuse making.

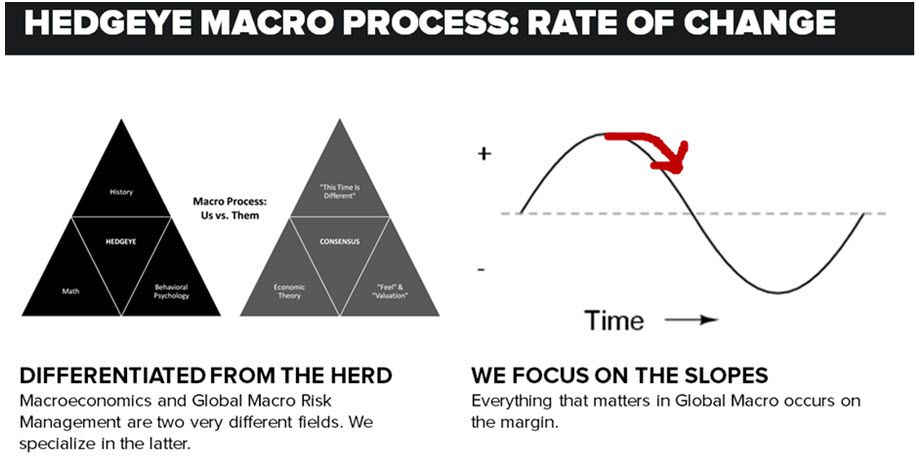

What always happens on the downslope of the cycle (see basic rate-of-change sine curve in today’s Chart of The Day) is that bullishly biased investors start to give you every reason why “stocks are cheap” (as both growth and earnings slow).

Then, as “cheap” gets cheaper, their performance starts to come unglued, their frustrations mount, and the excuse making accelerates. All I have to say about that is A) evolve (this is the 3rd #LateCycle slowdown since 2000) and B) stop whining.

Winning, not whining, is the name of this game – so let’s get back to focusing on that. I’m on my way to Chicago this morning and in bullet point form, this is what I see:

- Another bear market bounce based on HOPE for more central planning #COWBELL from Mario Draghi

- US stocks bouncing to lower-highs on DECELERATING volume (total equity market volume -8% vs 1mth avg)

- Russell 2000 and SP500 -11.5% and -8.5% from their #Bubble highs

- SP500 risk range remains wacky wide at 1 with TAIL risk resistance above that at 2048

- US Equity VOLATILITY (VIX) remains in a raging bull market with a wide risk range of 21.63-41.90

- Draghi #Cowbell speculation weakening the Euro, strengthening the Dollar, perpetuating #DEFLATION

- Beta Chasing going back to Biotech (IBB +3.9% yesterday) since Oil & Gas (XOP) got smoked by #DEFLATION

- GOLD correcting (again) into the ECB meeting as Down Euro = Up Dollar = Down Gold

- OIL still in a nasty bear market with immediate-term downside to $35-36 for WTI and OVX range = 45-57

- Bond Yields, globally, “off the lows” of last week, as they have been on no-volume equity market bounces

Oh, and literally every major macro equity market signal, from Japan and South Korea to Germany, Russia, Brazil, France, Canada, and … yes, the USA, continues to signal bearish from an intermediate-term TREND perspective.

I think much of the decline can be attributed to the cycle and complacent investors who have been largely indifferent to macro fundamentals.

Below you’ll see our immediate-term Global Macro Risk Ranges with our intermediate-term TREND views (in brackets):

UST 10yr Yield 1.99-2.22% (bearish)

SPX 1 (bearish)

RUT 1080-1183 (bearish)

DAX 9614--10222 (bearish)

VIX 21.63-41.90 (bullish)

USD 93.65-96.41 (neutral)

EUR/USD 1.09-1.15 (neutral)

YEN 117.70-124.81 (neutral)

Oil (WTI) 35.81-48.35 (bearish)

Nat Gas 2.61-2.76 (bearish)

Gold 1115-1165 (bullish)

Copper 2.21-2.33 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer