HOME FURNISHINGS BLACK BOOK

Slide Deck: CLICK HERE

Video Replay: CLICK HERE

Here's a quick summary of where we stand on RH, as well as links to our 90 page Home Furnishings Black Book and video presentation.

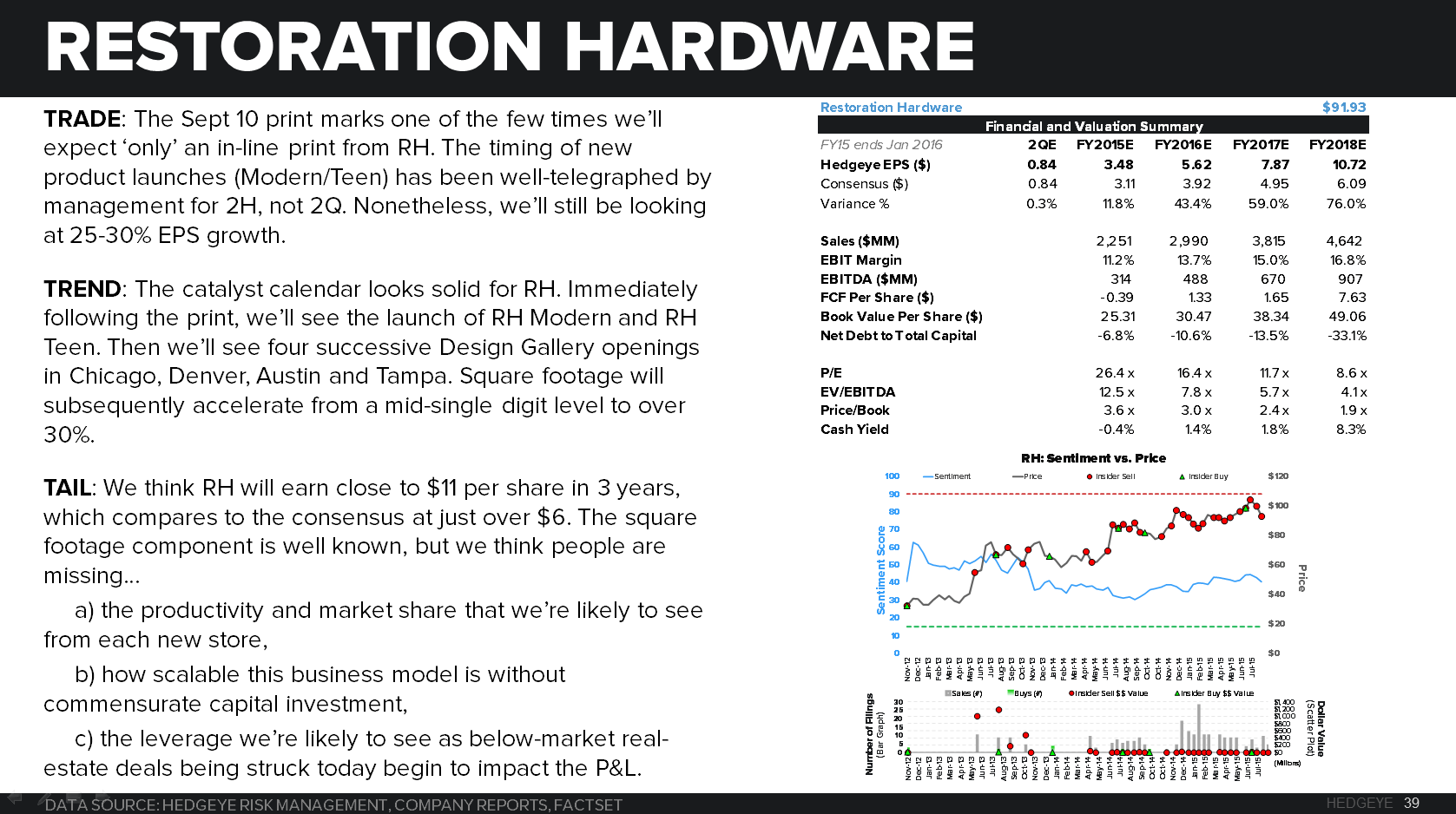

TRADE: The Sept 10 print marks one of the few times we’ll expect ‘only’ an in-line print from RH. The timing of new product launches (Modern/Teen) has been well-telegraphed by management for 2H, not 2Q. Nonetheless, we’ll still be looking at 25-30% EPS growth.

TREND: The catalyst calendar looks solid for RH. Immediately following the print, we’ll see the launch of RH Modern and RH Teen. Then we’ll see four successive Design Gallery openings in Chicago, Denver, Austin and Tampa. Square footage will subsequently accelerate from a mid-single digit level to over 30%.

TAIL: We think RH will earn close to $11 per share in 3 years, which compares to the consensus at just over $6. The square footage component is well known, but we think people are missing…

a) the productivity and market share that we’re likely to see from each new store

b) how scalable this business model is without commensurate capital investment,

c) the leverage we’re likely to see as below-market real-estate deals being struck today begin to impact the P&L.