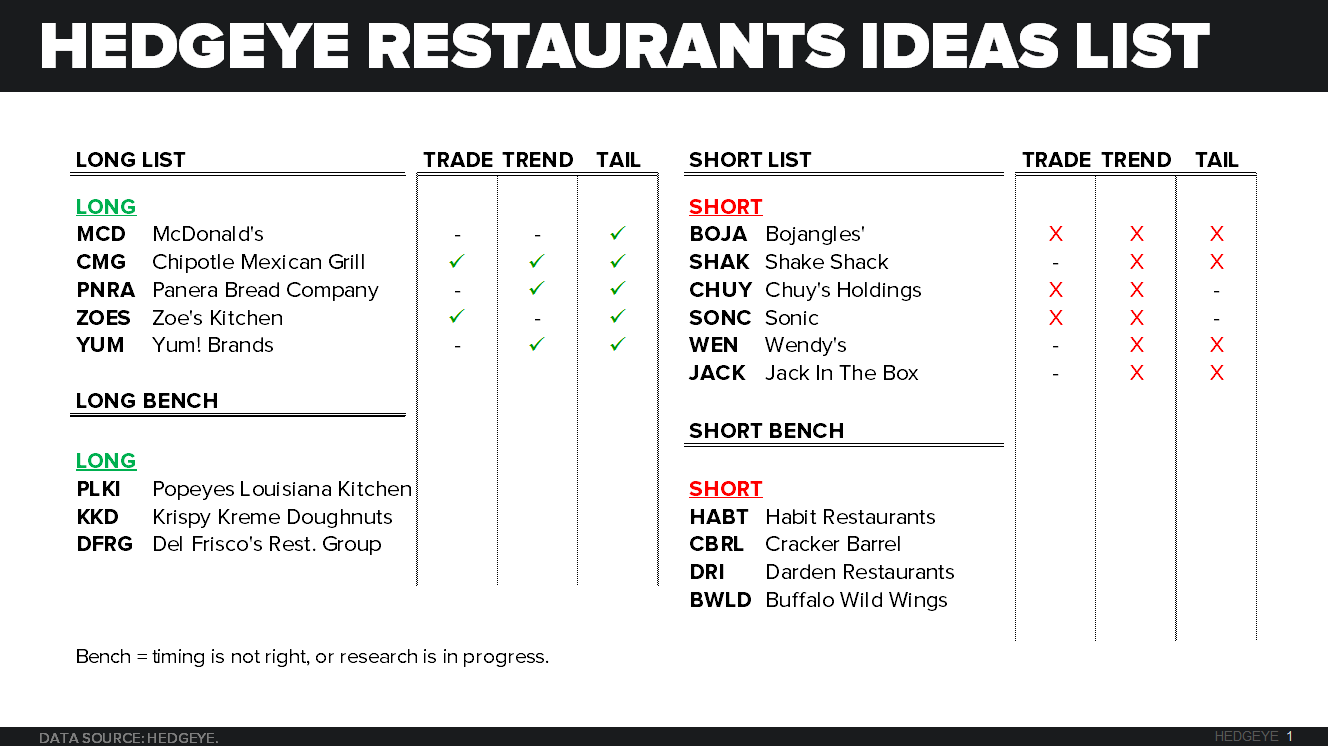

McDonald’s (MCD) is on the Hedgeye Restaurants Best Ideas list as a LONG.

The franchisees voted YES on the proposal last week to launch All Day Breakfast nationwide at all 14,318 U.S. locations. The vote confirmed on Tuesday, September 1st by the franchisee leadership council. This is a very important and monumental move by CEO Steve Easterbrook, and will define his legacy as the CEO that changed McDonald's and the rest of the industry for many years to come.

With this move we are also moving JACK and WEN from the bench to the Best Idea SHORT list. In 2016, if MCD (with all day breakfast and an improved value message) can drive same-store sales up by 5%, the system will generate $1.9bn in incremental system-wide sales. Needless to say, a healthy McDonald’s will make life difficult for a number of others in the QSR space.

As noted in our survey we released on July 27th it is evident that All Day Breakfast (ADB) will be a game changer for MCD. Breakfast is the single most requested item by McDonald’s customers, and listening to the customer is a tried and true way to succeed.

MENU

Menu changes are coming as part of this initiative. MCD will have to remove some items from the previous menu to make way for ADB. They have already announced the removal of certain sandwiches and snack wraps and the simplification of the drive thru menu, but expect more to come on a region by region basis. The company has said that they will be offering at minimum the Egg McMuffin, Bacon, Egg & Cheese Biscuit, Sausage Burrito, Hotcakes, Hash Browns and Fruit ‘N Yogurt Parfait.

KITCHEN CHANGES

As part of this move, operators will need to purchase separate grills and toasters. The grills will sit on rolling carts which will carry utensils used just for eggs to ensure the raw eggs do not contact any other food. The required investment will range from $500 to $5,000 per restaurant, depending on what equipment franchisees already have. We would not be surprised to hear that corporate is helping to support the franchisees making this investment.

TURNAROUND OUTLOOK

All Day Breakfast has the potential to be the “silver bullet” MCD will need to drive same-stores sales higher in 2016 and beyond. This will undoubtedly drive incremental traffic, probably even from people that don’t normally go to McDonald’s. The momentum that they gain from this must be harnessed to turnaround customer perception. This is their time to shine and we are confident the system is ready to show off its bountiful improvements to bring back their lost customers and continue to serve their loyal ones. ADB is coming sooner than we had thought, and we look forward to the November 10th analyst day in which we will assuredly be getting an early read on All Day Breakfast performance.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst