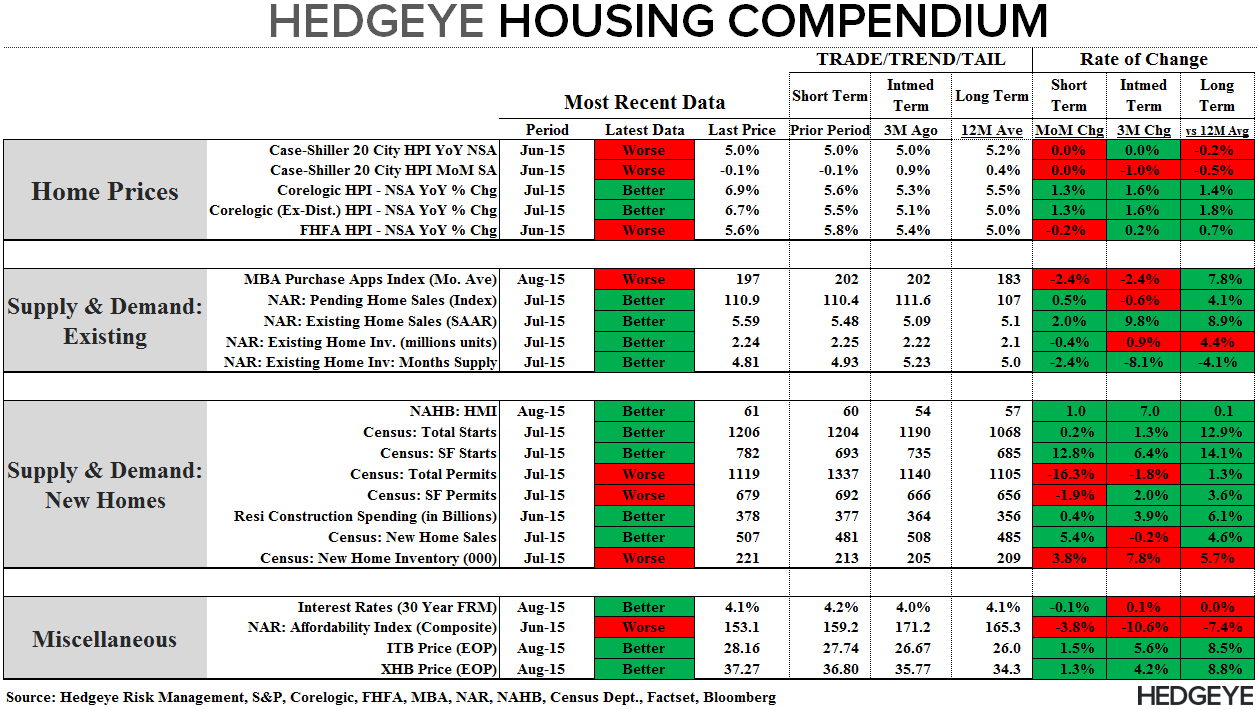

Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

Today's Focus: July CoreLogic Home Price Report

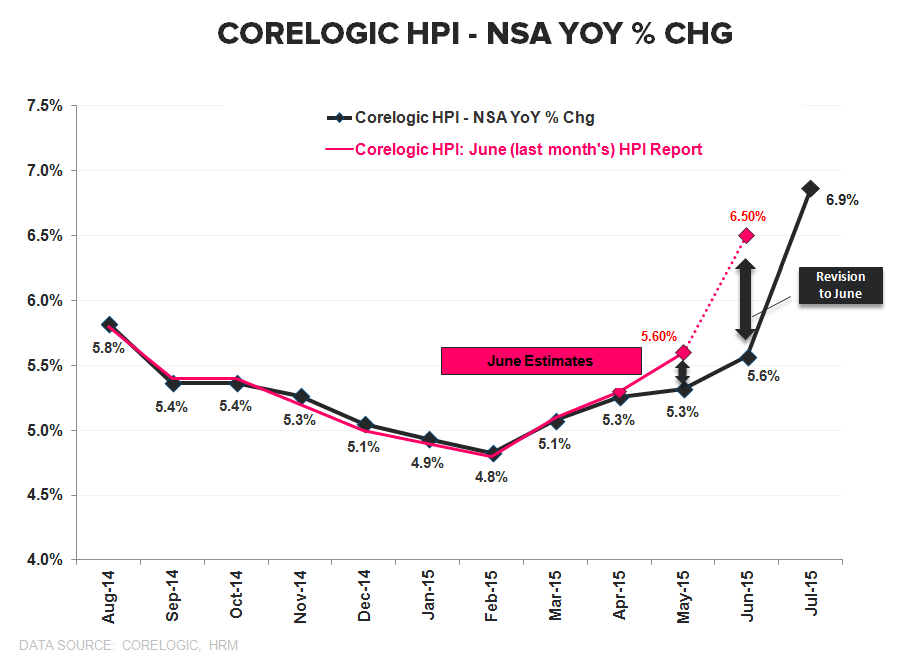

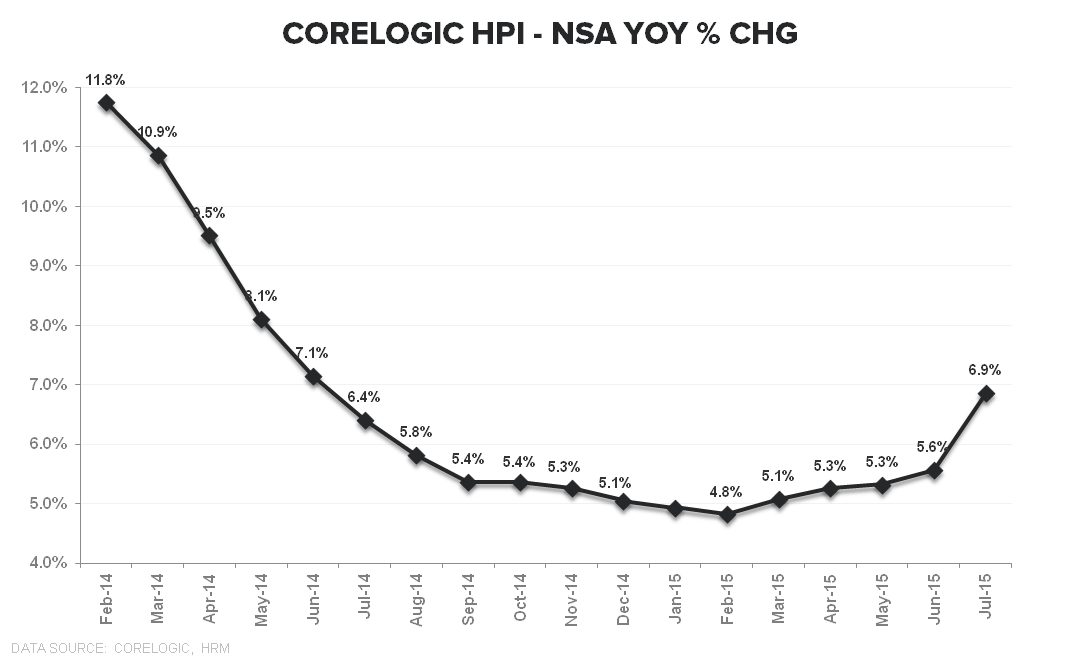

CoreLogic HPI: Home prices rose +1.7% month-over-month in July with year-over-year growth accelerating +130 bps sequentially to +6.9% - marking a 5th month of acceleration off the Feb ’15 RoC trough. Prices lag demand trends by ~12 months and rising TTM demand along with the prevailing tight supply environment argue for further acceleration in HPI over the nearer-term.

Revisions: Magnitude, Not Direction: Downward revisions to prior month estimates have been serial in the CoreLogic HPI series over the last ~12+ months. The August release continued that trend as the rate of change in HPI was revised lower by -30bps and -90bps in May and June, respectively (see 1st chart below).

In short, the recurrent trend in CoreLogic estimates has been this:

Initial estimates show a remarkable sequential acceleration in HPI ---> Subsequent downward revisions reflect only a modest acceleration ---> the direction of the 2nd derivative trend remains intact upon final revision but the magnitude of RoC improvement is significantly more muted than original estimates.

Given the prevailing trend, it’s likely the July figures see another downward revision while leaving the larger trend towards accelerating price growth in tact. The larger trend towards acceleration is the key takeaway as rising price growth supports higher ASP’s, builder margin expansion, and positive equity performance across the housing complex.

Further, it’s likely the trend across all three primary price series (CoreLogic, FHFA, Case-Shiller) becomes more congruent as the price trend matures. Specifically, we’d expect the Case-Shiller series - which is the most lagging and currently reflecting flat price growth – to play catch-up to the CoreLogic data on a lag and as the trend becomes more firmly entrenched. Historically, as can be seen in the 2nd chart below, the catch-up and overshoot dynamic has been typical of the Case-Shiller data over the last two decades.

About CoreLogic:

CoreLogic HPI incorporates more than 30 years worth of repeat sales transactions, representing more than 55 million observations sourced from CoreLogic's property information database. The CoreLogic HPI provides a multi-tier market evaluation based on price, time between sales, property type, loan type (conforming vs. nonconforming), and distressed sales. The CoreLogic HPI is a repeat-sales index that tracks increases and decreases in sales prices for the same homes over time, which provides a more accurate constant-quality view of pricing trends than basing analysis on all home sales. The CoreLogic HPI covers 6,208 ZIP codes (58 percent of total U.S. population), 572 Core Based Statistical Areas (85 percent of total U.S. population) and 1,027 counties (82 percent of total U.S. population) located in all 50 states and the District of Columbia."

Joshua Steiner, CFA

Christian B. Drake