“Disenchantment, whether it is a minor disappointment or a major shock, is the signal that things are moving into transition.”

-William Bridges

That’s a quote about life. But it fits my risk management framework for not only proactively preparing for Phase Transitions in markets, but for having the patience and #process to see those transitions play out.

Patience? It’s a word “long-term investors” seem quite amenable to using, other than when explaining why one of the lowest-beta, high return, positions during a slower-for-longer phase in both the Global and US economies, is the Long Bond.

We’re most bullish on Treasuries and Gold here. Others still like stocks. Will they be disenchanted with the selloff we’ll see to start September? Yes. How many others reworked and reset their risk parameters for causal risk factors that changed? We’ll see.

Back to the Global Macro Grind…

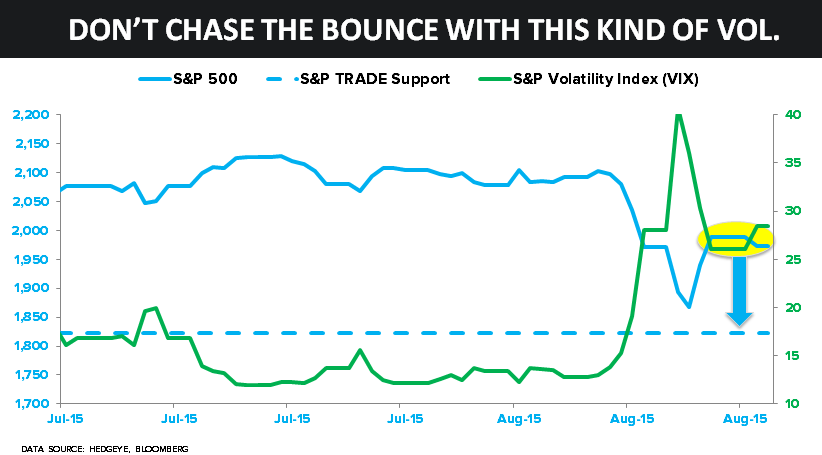

Selling into a bounce (on decelerating volume) should be a lot easier than selling into the all-time highs. That said, when you seek a bullish confirmation bias, that risk management exercise can be trying.

To review: Hedgeye didn’t add the SP500 to our Best Short Ideas until we released our Macro Themes Deck for Q3 in July. I won’t rehash the many interconnected macro reasons for that this morning, as I think I’ve been as clear as I can be.

At -6.3%, August of 2015 was the worst August for the SP500 since 2001. From a Sector Style perspective, Financials shocked the most amount of people at the most inopportune time (XLF -7.1% on the month) as consensus continued to bet on “higher rates.”

Other Sector Style callouts were:

- Utilities (XLU) outperforming early in the month, then getting slammed into month-end to close AUG -3.5%

- Healthcare (XLV) underperforming for most of the month, closing AUG -7.96%

- Energy (XLE) outperforming at the end of the month, closing AUG -4.3%

So, I guess, the new bull case from my competitors is “higher gas prices is clearly bullish for back-to-school.” Or something like that. But in all seriousness, this is getting serious – and there’s no value in debating Old Wall’s perma bull marketing ways.

It’s serious (and unnerving) because it appears that consensus is now LONGER (net) than they were last time the SP500 tested 1930. And since I have no support to 1, I think you should seriously think about that risk (the crowd) if it continues to manifest.

Another way to think about risk isn’t so much about depending on the market telling you where volatility adjusted “levels” of probable risk are (see my draw-down risk levels from my Friday Early Look note). It’s to overlay those signals with research.

Research, in rate of change terms, should go both ways. When undergoing a bullish (growth) to bearish Phase Transition, I like to think of the “research call” (different than the daily quantitative flow of the call) in three phases:

- Taking a non-consensus position early, but not too early (in July, Long Treasuries, Short Stocks)

- Staying with the short call after the 1st big “bounce” until your research catalysts play out

- Getting out of the call once something like #LateCycle + #Deflation becomes priced in as consensus

Currently we’re in Phase 2. And a lot of people are still trying to figure out what Phase 1 was all about (hint: it wasn’t just “China”).

While I suspect that Phase 2 can take some time (6-18 months, for starters – and we’re 3 months in), market history suggests that there’s nothing typical that maps out the “pricing in” of big top-down risks.

#EmbraceUncertainty

Volatility certainly has. And I’m not just talking about US Equity VIX ripping through 30 (again) this morning. Cross-asset-class volatility was a Phase Transition call we made in our 2014 Q3 (July) Macro Themes deck. So maybe that one is 12 months in!

Look at Oil, for example.

- BREAKING NEWS (on Bloomberg yesterday): “Oil Enters Bull Market”

- Lol

- Oil Volatility (OVX), meanwhile was making a 3-month high at 54!

Now what?

- Hedgeye’s long-term TAIL risk level of resistance for Oil (WTI) remains overhead at $60.74

- Oil’s (WTI) immediate-term risk range (the quantitative signal) = $35.74-48.93

- With Oil down -2% this morning, it could drop -25% (crash) from here, with no surprise

No surprise to our #process, that is. But I’d say that would probably be a tad disenchanting to whoever covered their Chesapeake (CHK) shorts into the close yesterday. We waited and watched and sent out another SELL signal on that into the close.

Contrary to popular “long-term” marketing beliefs, timing does matter; especially when in a Phase Transition. And our goal isn’t to rub that in our competition’s face. It’s to pound it into the keyboard so that it finds some place in your process.

Whether it is a minor disappointment or a major shock, our goal as a risk manager is to help you during transitions. After the last two cycle tops (2000 and 2007), we’re thinking your clients want to see that you’ve evolved your process and don’t have to make excuses.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.99-2.22%

SPX 1

DAX 9604--10272

VIX 20.82-42.50

Gold 1111-1165

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer