Two quick changes to our LONG bench we wanted to make you aware of, we removed MJN and added HSY. We will be releasing a note on these changes later today.

RECENT NOTES

8/31/15 HAIN | LOW QUALITY & INCREASED BUSINESS RISK

8/28/15 GIS | Time to Close this Deal

8/21/15 WWAV | DON’T PANIC, BUY MORE…HAIN | PANIC, SHORT MORE

8/21/15 UNFI | GOING AGAINST THE GRAIN

8/20/15 LNCE | Black Book Presentation Replay

RECENT NEWS FLOW

Monday, August 31

BETR | Initiated neutral at Goldman Sachs (underwriter of the IPO), price target $18. Current price is $13.31, we see downside from here and continue to have it on our SHORT bench.

Friday, August 28

GIS | Rumors continue to swirl around the divestiture of the Green Giant assets (click here for Hedgeye article)

Wednesday, August 26

THS | Upgraded to overweight from equal-weight at Stephens, target increased to $85 from $75. Treehouse seems to be the leader in the deal for the Ralcorp assets.

Tuesday, August 25

KHC | Recalled turkey bacon products (click here for article)

Monday, August 24

POST | Reinstated outperform at BMO Capital Markets, target is $72

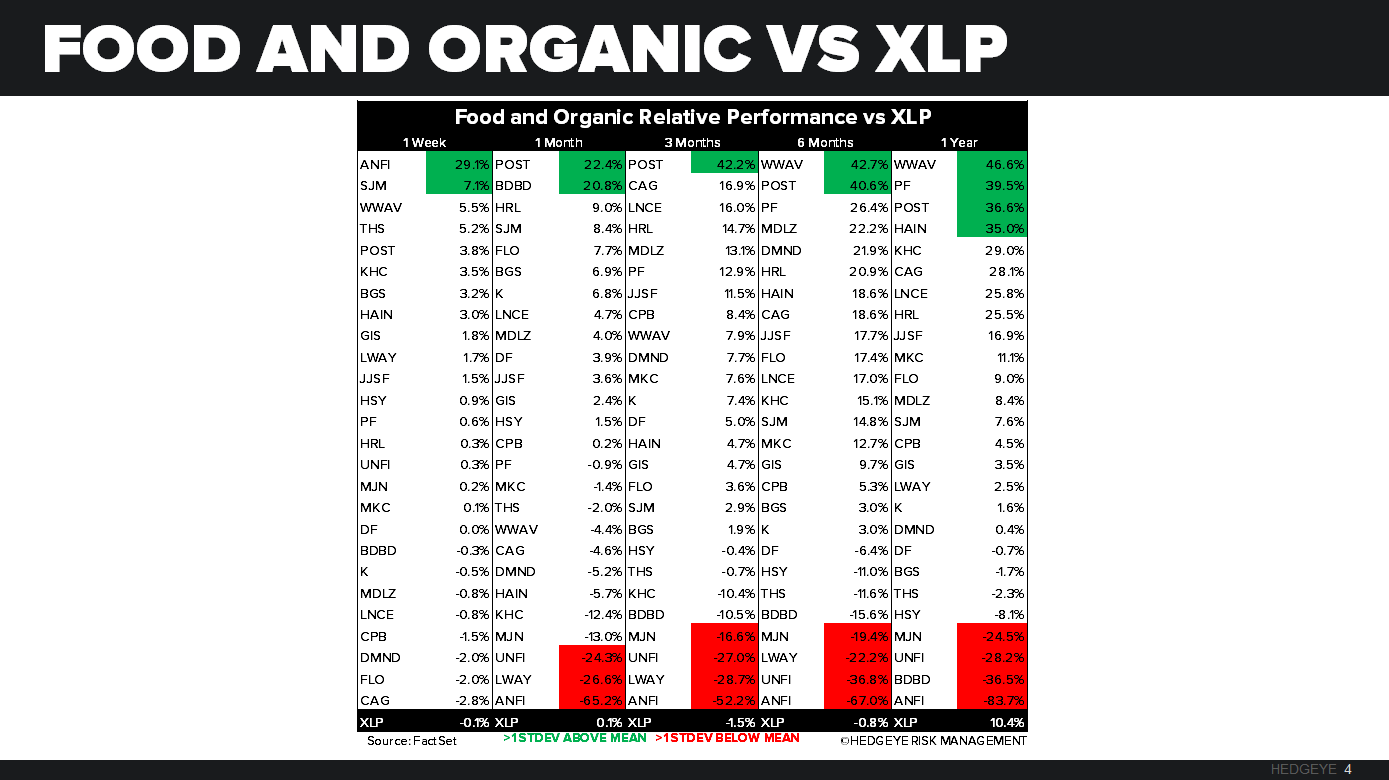

SECTOR PERFORMANCE

Food and organic stocks that we follow outperformed the XLP last week. The XLP was down -0.1% last week, the top performer from our list was Amira Natural Foods (ANFI) posting an increase of +29.1%. Worst performing company on our list was ConAgra (CAG), which was down -2.8%.

QUANTITATIVE SETUP

From a quantitative perspective, the XLP is bearish on a TRADE and TREND duration.

Food and Organic Companies

Consolidated Consumer Staples Valuation

After the volatile market last week, valuations remain near two standard deviations above the five year average EV/EBITDA multiple.

Keith’s Three Morning Bullets

- FEDERAL RESERVE – Fischer opted for dovish comments on Friday, making his Saturday comments more hawkish – I guess they look at the S&P Futures now before saying anything of consequence (today he’d be dovish); Fed Fund futures have ramped back up to 38% on a SEP hike probability – reminder: the Fed has never hiked into a slowdown

- COMMODITIES – dovish = commodity reflation; hawkish = commodity #Deflation – so the deflation TREND is right back on this morning w/ Oil, Copper, and Russia down -2-3%; WTI’s risk range blew out to $36.99-45.32 on Friday, all but ensuring that massive volatility remains in this asset class

- SP500 – still has the widest risk range my model has generated since 2008 at 1 with the more probable level being the downside one (-7.7% from Friday’s close), given that the Fed could be tightening into a 0.1% GDP environment here in Q3 (our low-end scenario with the high end being at 1.5% and the Atlanta Fed tracking 1.2%)

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst