Below are our analysts’ updates on our fourteen current high conviction long and short investing ideas. Please note we added Gold (GLD) and removed Japanese stocks (DXJ), REITs (VNQ) and the U.S. Dollar (UUP) this week. We also feature CEO Keith McCullough’s updated levels for each.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

gis

The update below was written by our Consumer Staples team.

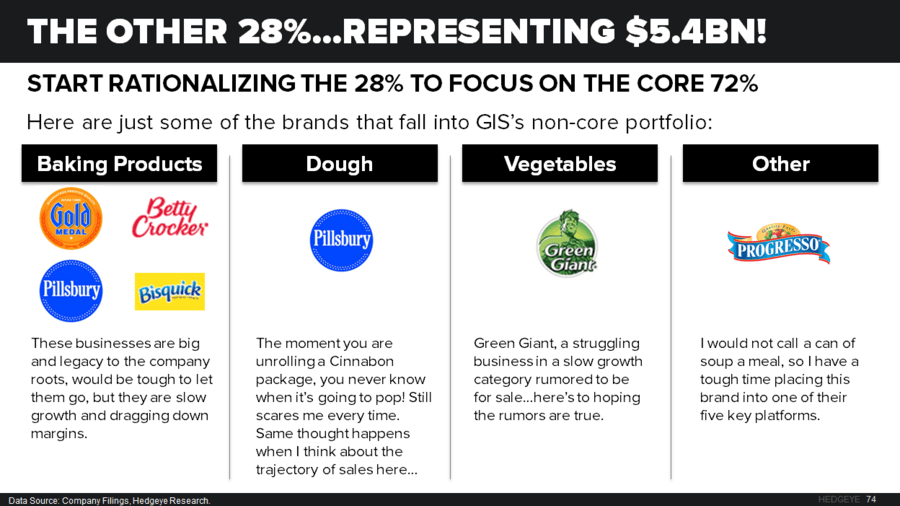

The widely rumored sale of Green Giant by General Mills continues to swirl. The latest is that B&G Foods (BGS) is taking a serious look into the asset. Frankly, we don’t care who buys it as long as it is a half way decent price. Our LONG bull call on GIS is partially dependent on them shedding non-core assets and acquiring high growth businesses. We believe this could be the first of multiple divestitures that GIS executes throughout the next couple of years. In our GIS Black Book we highlighted management identified non-core assets that could be up next.

The selling price of Green Giant is expected to be in the range of $600mm-$800mm pre-tax. We are expecting a hefty tax bill given the likely large step up in asset valuation that will need to occur. This will still give them the ability to reinvest further into growing the top line or buy a small snacking business. We have talked a lot about the potential snacking assets out there right now and we think this would be the best use of cash.

Talking with many industry professionals it seems as though sales are starting to stabilize. More specifically, cereal, something that everyone seems to think is all GIS has, (in reality its only 20-25% of net sales in any given year) will start to see growth return. The cereal category has bottomed and we feel that there will be a year-over-year increase in the category as GIS and the competition have invested heavily to revive the category.

At the end of the day, rumors are exactly that, rumors, but this sale seems to be coming to fruition, baring complete disconnect on price. To reiterate, this is the first deal of many that GIS has to execute in order to transform their portfolio for growth into the future.

We continue to view GIS as one of the best large cap companies in the staples space. They just announced that they will be releasing 1Q16 results on September 22nd before the market opens. We expect to see continued sequential improvement as they have cleaned up ingredient decks and streamlined the business.

fngn

The report below was written by Financials Co-Sector Head Jonathan Casteleyn.

We hosted a well attended investor lunch with the CEO of Financial Engines in New York City last week. The fundamental story is intact with the firm slowly executing on launching new products into the large and very profitable U.S. retirement markets. With more market share than the rest of its competitors combined, we still view the company as one of the best, unknown dominant players in financial services.

The best fundamental aspect of the firm’s positioning is that every two weeks, FNGN gets new inflows, as subscribers to their managed account services allocate part of their salary into their 401K which Financial Engines is managing. This is a far cry from the mature mutual fund industry which looks to garner new assets based on investor preference for risk which in this environment is on the decline.

The firm spoke a lot about new enhancements in its outreach program to get new subscribers in the door with more frequent campaigns and more digital points of presence to continue to push the message that a professionally managed 401K yields better results than investors that self-manage their retirement plans. Our research shows that over a longer period of time professionally managed 401K have yielded over +3% per annum in higher returns than self directed 401K plans.

This message becomes more valuable in times of market volatility as investors look to avoid losses. The stock remains on our institutional Best Ideas list as a long with a fair value of $52 per share.

The company arguably has one of the best growth trajectories in financials launching products into the very large retirement markets:

FNGN has one of the most dominant positions in financial services to boot with more market share than all of its main competitors combined:

virt

Jonathan Casteleyn has no new update on Virtu Financial this week.

lnkd

To view our analyst's original note on LinkedIn: CLICK HERE

We recently reviewed LinkedIn's 10-Q and spoke with IR; which collectively confirmed much of our thesis and takeaways from the 2Q15 earnings release. Most notably that its organic guidance cut was probably in excess of its fundamental prospects.

What's new is that we learned that LNKD ramped up its salesforce again in 2Q15, which we believe is a prudent move given what we see as an improving selling environment. Additionally, LNKD's recent Lynda acquisition may be growing faster than management initially led the street to believe when they announced the acquisition.

More importantly, we got the sense that management realizes that it really messed up by low-balling guidance two quarters in row. We don't think it will make the same mistake again on its next print. With the worst case scenario already baked into consensus estimates, we suspect the worst is behind them.

holx

The update below was written by our Healthcare Sector Head Tom Tobin.

As the final days of August turn to autumn, we are looking forward to our next two fundamental updates for Hologic here in Investing Ideas The global market's churn and worry has hit shares of HOLX. But with their business trends riding independent drivers, as long as the updates are solidly positive, we will be staying with our long.

First we will see the August 3D Tracker data. After three less-than-stellar months, we are expecting a solid rebound.

Second, the OB/GYN survey. We have been growing concerned about the impact of the #ACATaper, or the expected deceleration that will follow one of the biggest one-time expansions of insured medical consumers ever. Our survey has been signaling softness in some areas already. The one we are keyed on is Medicaid patient volume in states that expanded Medicaid under the ACA. But as always, we'll stay data dependent.

Look for updates from us next week on these two important items.

ZOES

The update below was written by our Restaurants team.

After the close yesterday, Zoe's Kitchen reported impressive 2Q15 numbers. If the street wants to point to one blemish, due to the continued success of the business and stock price appreciation, ZOES had to roll forward a few public company expenses as they are no longer labeled an emerging growth company under the JOBS Act. This is part of entering the big leagues. It is more a positive than a negative in our view.

ZOES reported revenue of $54.5mm a 30% increase YoY, narrowly beating consensus estimates of $54.0mm. Comparable restaurant sales increased 5.6% versus consensus estimates of 5.2%. The 5.6% was built up by a +1.3% increase in traffic, a +3.5% increase in product mix and +0.8% increase in price. ZOES had impressive performance all the way down the P&L leading to EPS of $0.05 beating consensus estimates by a penny.

ZOES opened seven new company-owned restaurants in the quarter, bringing the total company-owned restaurants to 148, with three franchised locations. Through August, they have opened seven additional restaurants bringing the total to 158.

Looking forward, management revised their guidance up slightly. Management is now projecting Restaurant sales between $220mm and $224mm up slightly from the previous $218mm to $223mm. Comparable restaurant sales growth is expected to be in the range of 5.0% to 6.0% bringing up the low end of previous guidance between 4.0% to 6.0%.

Listening to this management team talk makes us feel even more confident in the success of this company. They simply get it, the team environment cornered in everyone working toward the same goal together is culminating in great success. This story is nowhere near over and we expect to see continued strong performance from this company.

TLT | EDV | XLU | GLD

What a week.

As we outlined through various channels, we expect that high levels of volatility are here to stay for the foreseeable future.

Before we added exposure to Gold mid-week we had no allocation to U.S. equities or commodities. We decided to sit-out the 268 point round trip in the S&P 500.

The biggest shift this week that we’ll call out is a bullish to more neutral intermediate-term view on the U.S. dollar which is why we added GLD to investing ideas in replace of UUP.

To be clear, if growth continues to slow we want to be long of bonds (that view hasn’t changed in a year and a half).

For evidence, headline Q2 GDP was revised this week and macro tourists cheered on a big positive revision (based on the Q/Q SAAR number which is the incorrect way to view real growth in our opinion):

- On a Q/Q SAAR basis, GDP was revised higher to +3.7% Y/Y vs. +2.3% on the first print

- On a Y/Y basis, it was revised +40bps to +2.7% for Q2

The positive revision was due to higher Investment spending (NonResi + Inventories). Note that an inventory build contributing to GDP isn’t necessarily a great thing for the economy. The positive inventory change for Q2 only makes it a harder comp for Q3 (for that component of GDP) where Y/Y aggregate GDP comps get tougher also.

We look at GDP on a Y/Y basis. Any one quarter is compared to the 2 and 3 year average GDP prints in that same quarter. We now have the probable range of GDP for Q3 in the following range, and it’s ugly:

A) HIGH: Q3 2015 GDP (E) 1.5%

B) LOW: Q3 2015 GDP (E) 0.1%

Because the market is currently sniffing a dovish policy shift from the Fed, we decided to take down our USD exposure and add some gold. Remember, as we outlined 2 weeks ago, consensus was positioned for a rate cut (short gold and oil and long dollars). The risk embedded in a disappointment, which we called out, is now unfolding.

From an asset allocation perspective here is the set-up:

- Growth slowing: Long bonds and low-beta yield chasing sectors (TLT, EDV, XLU)

- Shift to more dovish policy: long of GOLD as the shift weakens the value of the USD

We re-iterate the same view we’ve had since the beginning of 2014:

Growth is slowing, and deflation remains a real risk (central bankers can’t solve this by talking down the currency). The fed will continue to push out the dots on “policy normalization.”

The picture below is a chart of the December 2015 Fed Funds futures implied rate. At the beginning of 2015, the market expected the mid-point of the fed funds upper and lower bound would be at 0.40%. Now the market isn’t expecting much more than no rate hike by December. That’s quite a turn around from the “June liftoff” talk in Q1.

MCD

To view our original note on McDonald's: CLICK HERE

We recently tried out the "Create Your Taste" experience at the newly remodeled McDonald’s location in Midtown East on the corner of 58th street and 3rd Ave. Walking into the newly remodeled MCD, we were greeted by the brand new self-order kiosks with attentive staff there to assist you. Customers were very interested in using the kiosks, and everyone using them seemed to be having an easy time with it.

The whole process from creating your own burger to getting your food was simple and seamless. The self-order kiosk is easy to follow, you can order from the entire menu and pay from the kiosk. We decided to build a custom burger, in which you scroll through different screens selecting from a wide variety of cheeses and toppings. I must note however that they were out of a select number of topping items, as they are working out the kinks since just starting the Create Your Taste two weeks ago. After paying, you take an electronic GPS enabled disk to your table so that the server can locate you within the restaurant. The ordering process was a pleasant experience and I would say will lead to increased checks as it is very simple to just click on additions rather than staring at the big board at the main register. As you can see from our receipt above, the total came to $10.88 definitely not the average check that a MCD customer is used to.

As we ordered we sprung up a conversation with a couple of staff members to get a read on how the staff likes the new system. The two people we talked to had overwhelming positive reviews of how the kiosks increase efficiency in the restaurant, specifically the kitchen, and allow for orders to be entered quicker. When asked specifically about the Create Your Taste, they said they love the concept and haven’t experience any major difficulties with it.

It was time to head to our table, we found a comfortable spot upstairs kind of in the corner to test out the GPS location ability on the disk we picked up at the kiosk. The server found us with no problem, total time from payment to food on the table was about 9 minutes, which is right in the middle of their 8-10 minute range. Although they didn’t fill up our drink as they said they would, everything else was presented very well. The food was still warm and everything tasted good.

For it being only two weeks into the process we were very impressed by the efficiency and mastery the staff is already displaying. We plan to head back to the same McDonalds location and check on their progress.

RH

To view our analyst's original note on Restoration Hardware: CLICK HERE

Williams-Sonoma (WSM) reported 2Q15 results on Wednesday. Here are the two most important read-throughs as it relates to our top long idea in the retail space -- Restoration Hardware -- which will report earnings in two weeks.

- Top line – though every concept decelerated sequentially on a 2yr basis except for PB Kids (flat) the company beat lowered expectations by 200bps or $19mm. 25-50% of this was due to the guided port strike revenue issues ($5-$10mm) which didn’t materialize during the quarter (sandbag?). That’s good news for RH who a) isn’t reliant like WSM on seasonal merchandise and b) product flow should start to normalize.

- West Elm continued to hum along with a 15.7% comp in the quarter. To be fair that was a 90bps deceleration sequentially in the underlying trend, but it’s been a fairly good barometer for RH over the past few quarters and the current consensus numbers assume that West Elm outperforms RH in the numbers the company will report in 2 weeks. West Elm has only outcomped RH twice since 2012 in 1Q14 and 2Q14 when the company changed up its source book strategy. We expect to see a bifurcation in growth trends as RH top line growth accelerates in back half of the year as it rolls out Modern and Teen.

FL

The update below was written by Retail analyst Alec Richards.

We have been actively talking about Foot Locker as one of our better short ideas since the start of the year. The long-term (TAIL) call was crystal clear to us then, as well as the risks to the business model that are not being priced in to the stock.

But we were less certain on near-term drivers to bridge the TRADE call with the TAIL.

However, now we think the intermediate-term picture is much more clear. At least from where we sit. And we think that returns will head lower by the end of this year (retail stocks rarely go up when returns go down).

All in, if we’re wrong in our analysis, we think the upside is $75 (15x $5). If we’re right, we think it can revisit $50-$55 (12-13x $4.00), at least 3 to 1 downside to upside.

PENN

Our Gaming, Lodging & Leisure team is going to furnish a new update following their recent meeting with Penn National Gaming's management. They note that the stock has held up quite well despite increased market volatility. The bullish thesis on shares of PENN remains intact. Regional revenues remain strong in addition to the 2-year growth story, etc. Stay tuned.