“I gotta have more cowbell.”

-Christopher Walker

As many of you know, every year central-market-planners descend from upon high to the Teton Mountains in Jackson Hole, Wyoming. This is where ideologies associated with being able to bend economic gravity live large. #TaxPayerVaca

Technically speaking, it’s illegal for members of various un-elected and inaccurate forecasting agencies to leak what will ultimately become breaking news (cuts, easing, devaluations, etc.), but I did get an exclusive peak at the after party last night.

Do not forward this to anyone. Here it is: https://www.youtube.com/watch?v=GCd0OjjCz88 Many thanks to our man on the ground, Will Ferrell, and his version of the Blue Horseshoe Oyster Band for bringing us the catalyst for the next bull market.

Back to the Global Macro Grind…

Not to downplay what appears to be the most ominous setup in my macro model since 2008, I think it’s important to start to analyze this tragedy using some humor. Otherwise, the sadness of the situation could very well overcome me.

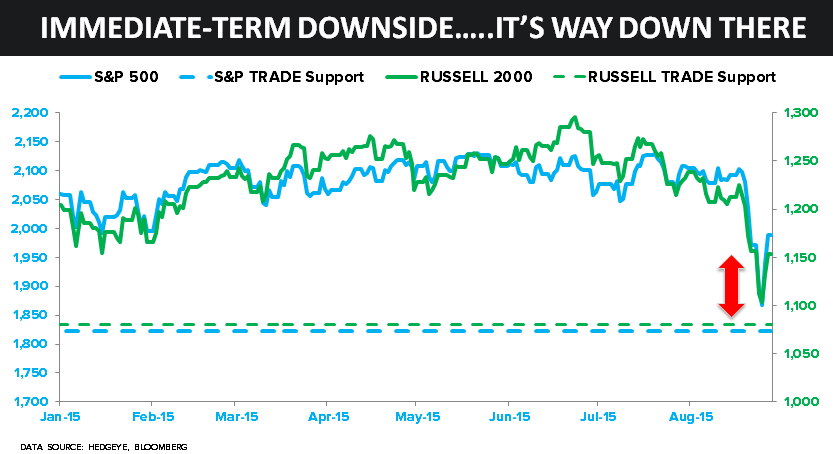

And I mean that sincerely. As I look at what I call the downside of the “probable range” in Global Equity markets this morning, for the first time in my career I don’t think I want to be right.

That’s a tough thing for me to write because the goal of the game is to be right. We’ve spent the last 7-8 years trying to evolve the Global Macro risk management #process to the point where many aren’t unprepared for this. Unfortunately, many are.

Rather than depress you with words, let me just show you the numbers my models showed me:

- SP500 has immediate-term downside of -8.3% to 1822

- Russell 2000 has immediate-term downside of -6.3% to 1080

- Germany’s DAX has immediate-term downside of -8.1% to 9506

- Japan’s Nikkei has immediate-term downside of -9.5% to 17304

- China’s Shanghai Comp has immediate-term downside of -19.3% to 2607

If I keep going, I’ll feel ill. And not for me. I mean for the many who have depended on the Fed, ECB, BOJ (and now Chinese) to bail them out of the idea of economic gravity slowing, deflating, etc.

But, but – GDP was +3.7% yesterday. Yep. In sequential (SAAR) terms vs. a sequential bomb of Q1 GDP. But the real bomb is going to be the Federal Reserve raising interest rates into a potential Q3 GDP print of 0.1%.

That’s right, 0.1%. We always model a high and a low range estimate in the Hedgeye Predictive Tracking Algorithm Model for any country’s GDP. And after updating the model for yesterday’s real-time data, here are those two scenarios:

A) HIGH: Q3 2015 GDP (E) 1.5%

B) LOW: Q3 2015 GDP (E) 0.1%

While we don’t think you should look at any country’s economic growth in Q/Q SAAR terms (year-over-year rate of change is a much more accurate representation of the cycle’s reality), you actually have to because both non-macro people and the media do.

My greatest fear is that the Fed doesn’t yet look at it the way we (and many of our Institutional Clients) do. My fear looks just like the SP500 did at its 1867 close on Tuesday. Imagine the Fed was raising rates into that?

And trust me, I get it. For God’s sake I’d write about why the Fed should have been raising rates during our #GrowthAccelerating call of 2013 just about every other Early Look. I also drove the #StrongDollar, Strong America thesis. But I also get that:

A) The Fed missed their window to raise rates

B) The modern day Fed has NEVER tightened into a slowdown

C) No one knows how low equity markets can go in that scenario

Reminder: my scenario includes:

- The Street LOW forecasts on Q3 GDP (we’ve had them all year)

- An expectation of pervasive #Deflationary forces

- Downside to Q3/Q4 revenue and earnings expectations

So I don’t expect to see consensus and/or the Fed to see what I see this morning.

I look at the models we have built to proactively predict the #LateCycle slowdowns of 2007 and 2015. They look at whatever they are looking at. And every strategist who has had growth and inflation wrong in 2015 is looking for more cowbell.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.98-2.19%

SPX 1

VIX 20.56-44.64

Oil (WTI) 37.55-43.74

Gold 1105-1168

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer