RECENT NOTES

8/21/15 WWAV | DON’T PANIC, BUY MORE…HAIN | PANIC, SHORT MORE

8/21/15 UNFI | GOING AGAINST THE GRAIN

8/20/15 LNCE | Black Book Presentation Replay

8/11/15 LNCE | GOING IN LONG

8/10/15 LWAY | Sitting on a Gold Mine with no Tools

RECENT NEWS FLOW

Friday, August 21

LWAY | Ramps up production at newly refurbished facility in Wisconsin (click here for article)

Thursday, August 20

SYY | Elects Nelson Peltz and Josh Frank to Board of Directors (click here for article)

MKC | Completes acquisition of Stubb’s (click here for article)

MDLZ | Ardent Mills acquires Mondelez Canadian flour milling facility (click here for article)

Wednesday, August 19

KO | Pays roughly $90mm for 30% stake in Suja, as the fresh juice craze continues (click here for article)

Tuesday, August 18

HSY | Announced pricing of $300mm 1.6% notes due 2018 and $300mm 3.2% notes due 2025 (click here for article)

CAG | Darren Serrao, Campbell veteran moving to ConAgra to newly created position, Chief Growth Officer (click here for article)

SECTOR PERFORMANCE

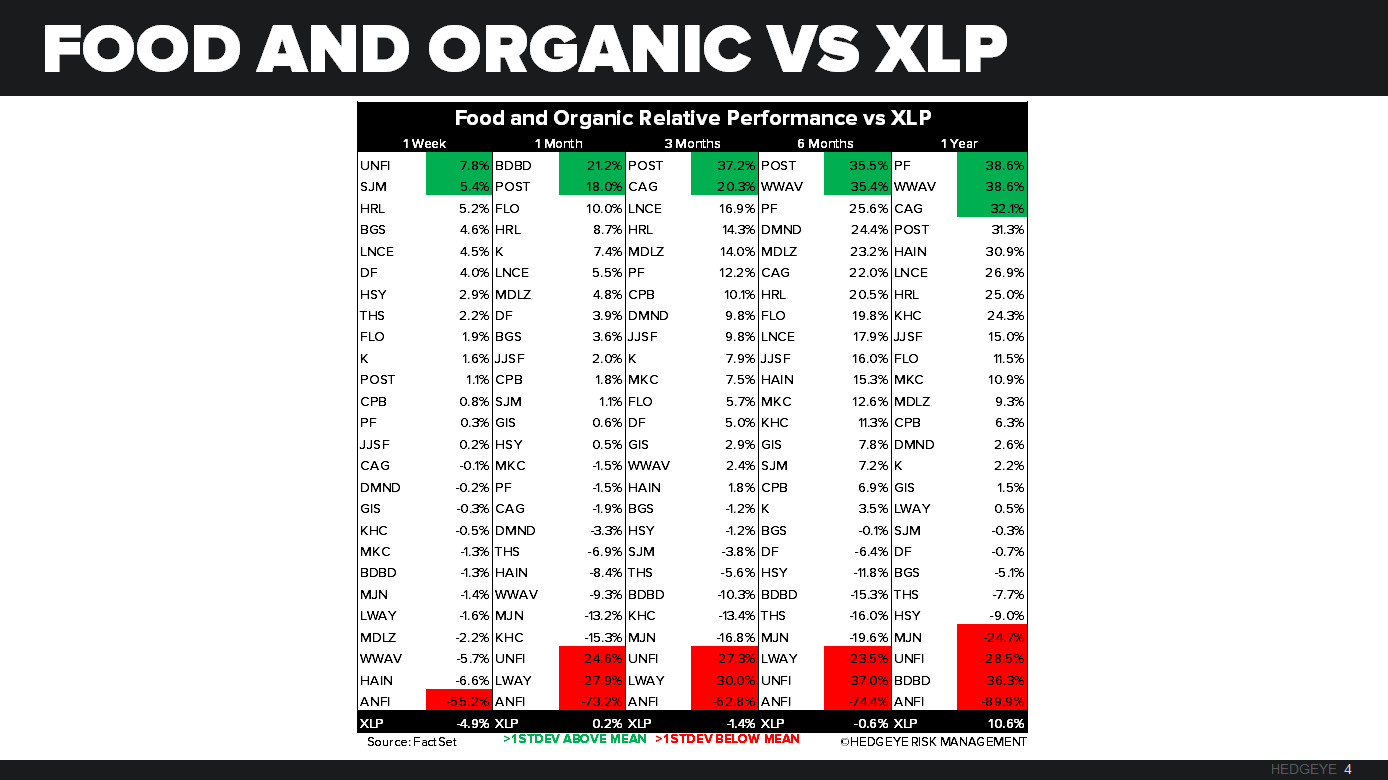

Food and organic stocks that we follow outperformed the XLP last week. The XLP was down -4.9% last week, the top performer from our list was United Natural Foods (UNFI) posting an increase of +7.8%. Worst performing company on our list was once again Amira Natural Foods (ANFI), which was down -55.2%.

QUANTITATIVE SETUP

From a quantitative perspective, the XLP is bearish on a TRADE and TREND duration.

Food and Organic Companies

Consolidated Consumer Staples Valuation

The stocks we follow in the consumer staples sector faired okay compared to the rest of the market last week. Valuations remain near two standard deviations above the five year average EV/EBITDA multiple. We are most likely in store for further correction in the space.

Keith’s Three Morning Bullets

- CRASH – not an inappropriate word to use given that on the 3-month duration alone, Oil (-37%), China (-31%) Emerging Markets (-26%), and Long-term Sov Bond Yields have crashed. This is a literal crashing of both US and Global growth expectations – we’re still at ½ of consensus forecasts

- HIKE? – oh definitely – they should hike. “It’s just 25 basis points, Keith” – yep. Have at it. Let’s see what happens. This risk of being too tight during both the cyclical and secular slowdown was only obvious to those who had the bearish growth and inflation views. Jackson Hole = Thursday

- VIX – the main challenge with modeling accurate risk management levels right now is that volatility is undergoing a major Phase Transition across durations – hard to explain in 140 characters or less but very easy to see the series of higher-highs going back 2yrs