Key Takeaway:

Here are the key things to keep an eye on:

Front Burner Disasters:

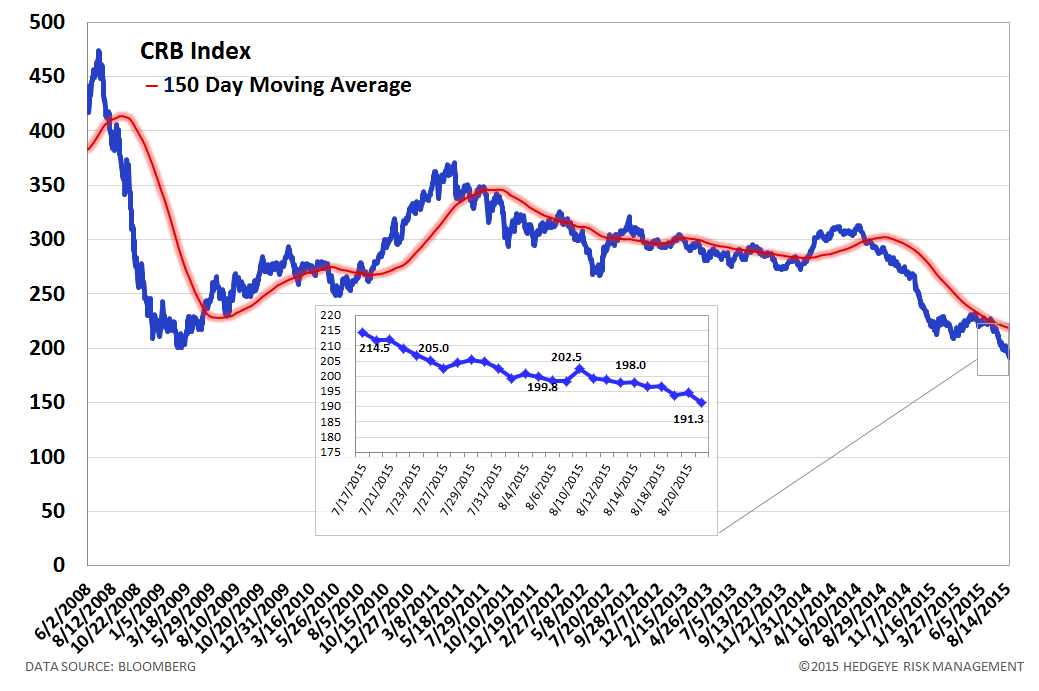

1. Commodities torched for another -3.7% W/W drop, bringing the M/M change to -6.7%

2. Junk Bonds rip another +19 bps W/W to 7.40% and are higher by +41 bps M/M.

3. Leveraged Loans shed 4 points to 1866 W/W and are down 18 pts M/M.

4. EM Sovereign Swaps: Russia +45 bps W/W to 420 bps. Brazil +25 bps to 330 bps. Indonesia and Thailand: +28 bps & + 22 bps, respectively.

Back Burner Simmers:

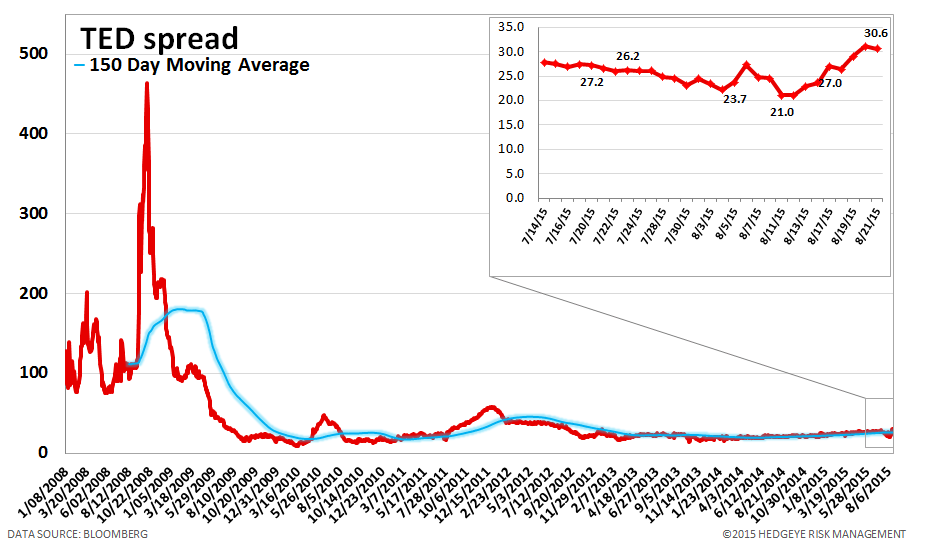

1. US TED Spread (US Interbank rate): +7 bps to 31 bps - biggest 1 week move in years.

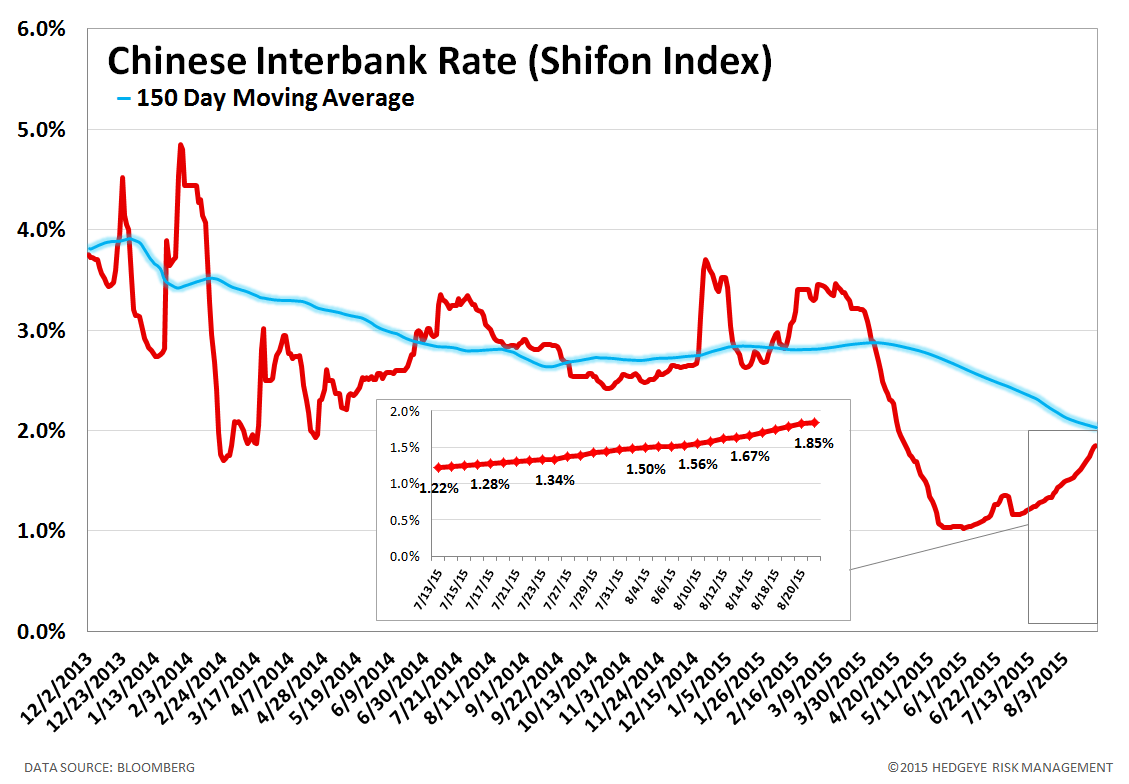

2. Shifon Index (Chinese Interbank rate): +18 bps W/W to 185 bps. Almost a double from mid-June lows of ~100 bps.

Last week, global markets roasted on concerns over Chinese economic growth and concerns over a broader Asian collapse. Most notably, CDS widened broadly, the price of oil hit a new low, high yield YTM blew out by another +19 bps, the TED spread spiked by +7 bps, and the Chinese interbank rate rose by +18 bps. As we show in the heatmap below, market risk is tilted heavily negative in the short and intermediate durations, while the long-term balance remains positive (for now).

Current Ideas:

We're adding BlackRock (BLK) to our Best Ideas Short Bench.

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 2 of 12 improved / 7 out of 12 worsened / 3 of 12 unchanged

• Intermediate-term(WoW): Negative / 3 of 12 improved / 8 out of 12 worsened / 1 of 12 unchanged

• Long-term(WoW): Positive / 4 of 12 improved / 2 out of 12 worsened / 6 of 12 unchanged

1. U.S. Financial CDS - Swaps widened for 18 out of 27 domestic financial institutions. The average change was +6 bps as concerns over Chinese growth shook global markets.

Tightened the most WoW: CB, ACE, ALL

Widened the most WoW: WFC, BAC, RDN

Tightened the most WoW: ACE, AXP, CB

Widened the most MoM: GNW, RDN, MET

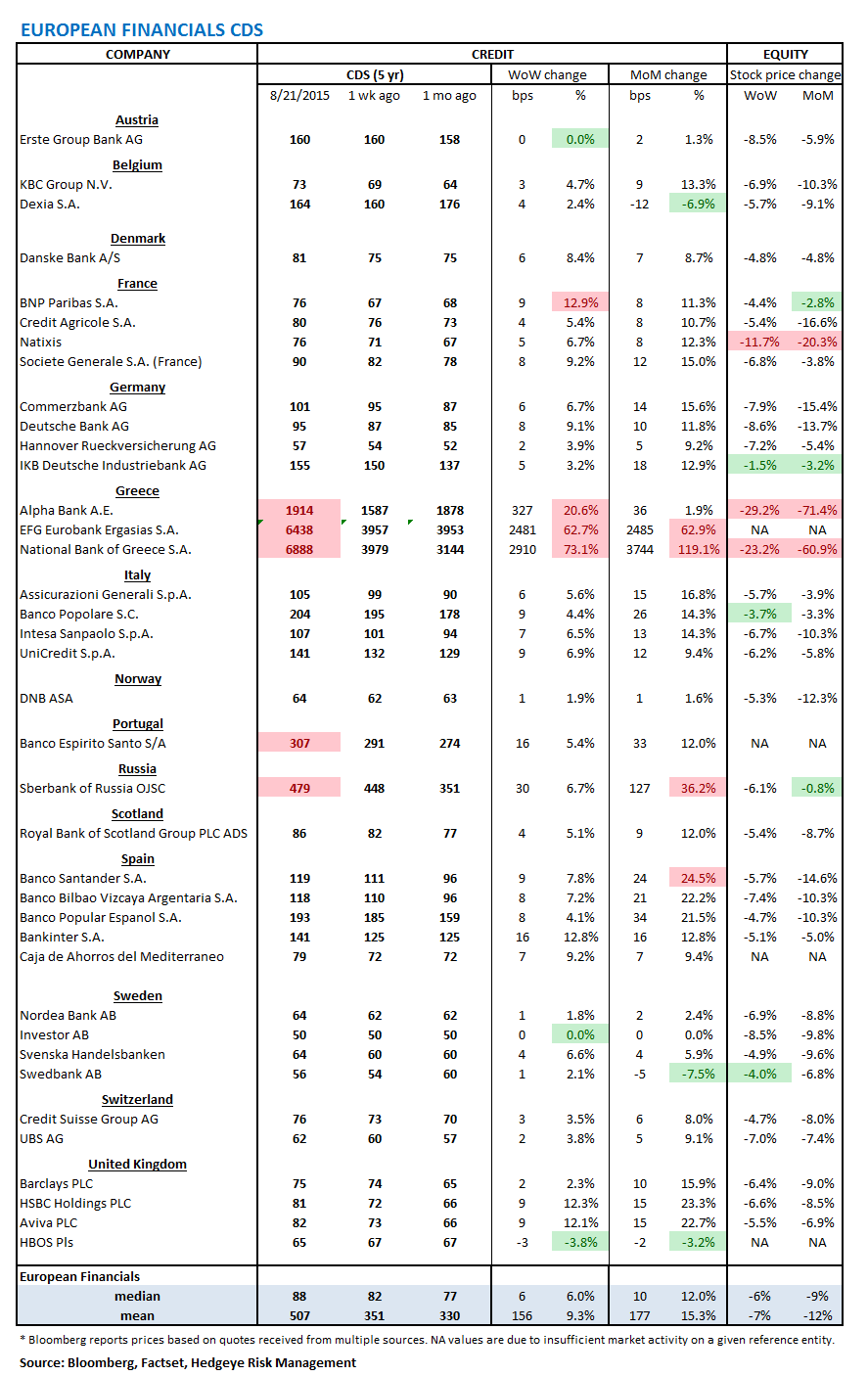

2. European Financial CDS - Swaps mostly widened among European Banks last week as global worries over growth in China rose. Russia's Sberbank swaps widened by +30 bps to 479 as the price of oil fell to $40 as of Friday's close. Additionally, with the political volatility of Greece's prime minister planning to resign, that country's banks' swaps widened between +327 bps and +2,910 bps.

3. Asian Financial CDS - While swaps across the region were mixed, last week's focus was growth concerns in China, where financial CDS widened between 11 bps and 12 bps.

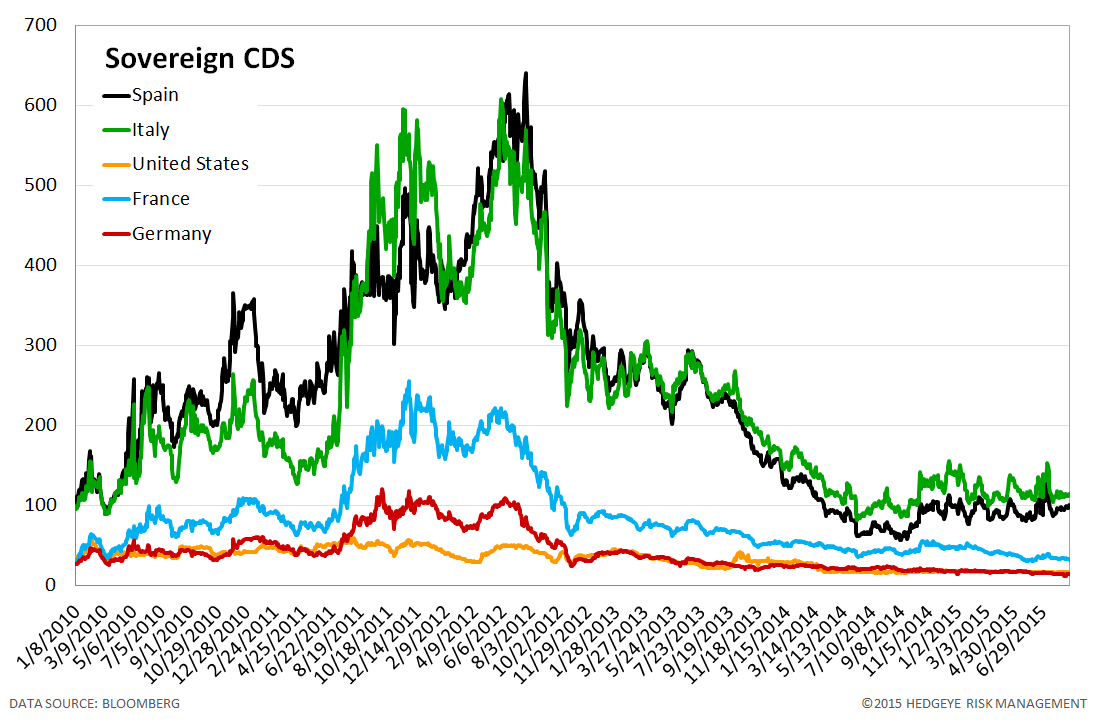

4. Sovereign CDS – Sovereign Swaps were largely unchanged last week. The largest moves (+/- 1 bp) came from French, Italian, and Japanese swaps.

5. Emerging Market Sovereign CDS – Emerging market swaps widened sharply last week. Russian sovereign swaps widened the most, by +45 bps to 420. Brazil was close behind at +25 bps to 330 bps.

6. High Yield (YTM) Monitor – High Yield rates rose 19 bps last week, ending the week at 7.40% versus 7.21% the prior week.

7. Leveraged Loan Index Monitor – The Leveraged Loan Index fell 4.0 points last week, ending at 1866.

8. TED Spread Monitor – The TED spread rose 7 basis points last week, ending the week at 31 bps this week versus last week’s print of 24 bps.

9. CRB Commodity Price Index – The CRB index fell -3.8%, ending the week at 191 versus 199 the prior week. As compared with the prior month, commodity prices have decreased -6.7%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by 1 bps to 10 bps.

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose 18 basis points last week, ending the week at 1.85% versus last week’s print of 1.67%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

12. Chinese Steel – Steel prices in China fell 1.0% last week, or 24 yuan/ton, to 2331 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread tightened to 142 bps, -5 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

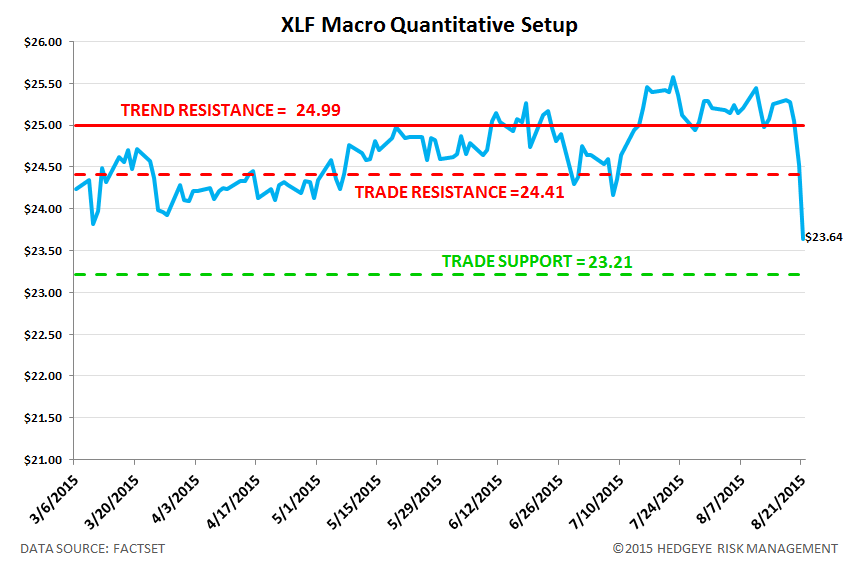

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows that Financials are now both broken TREND (intermediate term) and broken TRADE (short term). On a short term basis, there is 3.3% upside to TRADE resistance and 1.8% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT