“Mr. Worldwide to infinity, you know the roof on fire”

-Pitbull

Since this morning isn’t going to be fun for anyone but Long Bond bulls (TLT), I thought I’d start my morning with a McCullough Clan household favorite and try to change the mood up a little:

“We gon’ boogie oogie oogie, jiggle, wiggle and dance”

My 19 month-old girl can cut a rug to #Fireball like you wouldn’t believe (she calls it “Ball, ball”). And if you didn’t know that the roof of global growth expectations is on fire, you haven’t been reading my rants for the past 3 months. Markets are crashing.

**Keith is LIVE on The Macro Show at 9am ET this morning. Click here for access.

Back to the Global Macro Grind…

Crash? Yep. In big macro stuff, this slow-moving train wreck of willfully blind US and global growth expectations has been very obvious. You should not be surprised, whatsoever, by the following this morning:

- Oil crashing (down another -3% this morning, -38% in the last 3 months)

- China crashing (down another -8.5% overnight, -31% in the last 3 months)

- Emerging Markets crashing (-21.3% on MSCI and -23.4% LATAM in the last 3 months)

Oh, and Bond Yields (on the long-end of the curve) have crashed (again) in the last 3 months too. From 2.54% on the 10yr UST Yield to 2.01% this morning as inflation expectations crash (5yr UST Break-Even collapses to 1.14%, -52bps in 3 months).

But the Fed should definitely raise rates, eh? “It’s just 25 basis points, Keith.” Yep. I know. Have at it … and let me know how that goes for everything that’s rate sensitive now that … you know, everything else is like “the roof on fire”!

#Fireball!

I sincerely don’t mean to make fun of the situation market’s are in. But I do. I haven’t heard this many “it’s different this time” narratives since the 2000 and 2007 cycle tops.

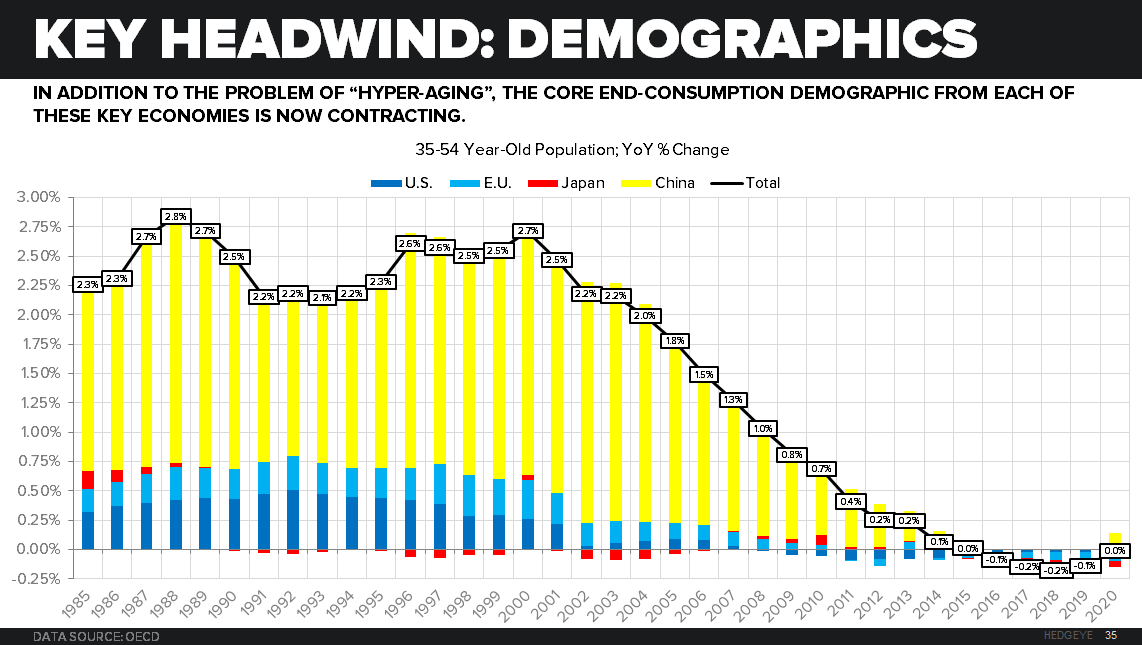

And the last two cycle tops didn’t have this mother of all demographic secular slowings (which actually makes it different, for the worse – see Chart of The Day for the demographic tail wagging this global demand dog).

Oil, Chiner, EM – yep. You get that. But who gets #EuropeSlowing? Last week alone, here was the European Equity score:

- Euro Stoxx 600 Index -6.5% and -11.4% in the last 3 months (plus what it’s down this morning)

- Germany’s DAX down another -7.8% last week and -14.7% in the last 3 months

- Russian Stocks (RTSI) down another -8.7% last wk and -27.2% in the last 3 months

Germany and Russia slowing, at the same time? Probably just another glitch in a chart or something. “Don’t pay so much attention to the data” in Europe, ok? The secular (demographic) headwinds there are even stronger than USA’s.

Back to the US story, ex-long-Energy (XLE -8.4% wk-over-wk and -21.1% in the last 3 months) here’s what Style Factors in the SP500 got crushed the most last week:

- High Beta Stocks -7.8% on the week and -15.6% in the last 3 months

- Top 25% Sales Growth Stocks -6.4% on the week and -8.2% in the last 3 months

- Top 25% EPS Growth Stocks -6.4% on the week and -8.7% in the last 3 months

In other words, with the SP500 -5.8% last week and -7.6% in the last 3 months, the aforementioned “Growth” Style Factors underperformed the market’s beta… and the question remains whether or not being long “growth” starts to look like being long “value” (i.e. #Deflation Risk) has for the next 3 months?

As a reminder, the base effect (comparative period, year-over-year) for US GDP growth gets tougher in the 2nd half of 2015 vs. the 1st half. That means, if you held all other risks equal, the probability is higher that growth slows in Q3 and Q4 than Q2. That’s one of the biggest reasons why our US GDP forecast is ½ that of our top macro research competitor for Q3.

Not that “the data” or being right matters, but what happens if we continue to be right on growth and inflation AND the Fed decides to “tighten because it’s time”? While I’m praying they don’t make that policy mistake, anything can happen – and if they do, “we gon’ drink drinks and take shots until we fall out, like the roof on fire.” #Fireball

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.01-2.14%

SPX 1

VIX 20.80-31.51

EUR/USD 1.11-1.15

Oil (WTI) 39.01-41.93

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer