HIBB already preannounced this one, though it threw out guidance for the back half that is anything but a slam-dunk. We still think there’s earnings risk this year, but more importantly we think that the end-game is margins getting cut in half, and about $1.50 in earnings in three years. That’s a pretty massive statement given that the consensus is at $3.85. What kind of multiple do you put on a name with shrinking earnings and 60% downside to consensus? Even if we generously say 15x a trough-ish EPS number, we’re talking about a $22 stock.

What We Liked

- It’s hard to find a lot to like in this print, but if we had to call out two positive changes on the margin it would be that a) HIBB realizes it has a merchandising problem and b) the company seems to have a timeline in place to get its e-comm business off the ground.

- As far as merchandising is concerned, we have a hard time reconciling management’s belief that its merchandise assortment is wildly out of whack with current trends. In light of the sales growth numbers being put up by NKE and UA in the US why wouldn’t HIBB benefit? We think it’s more of an issue with sales moving to the web (where HIBB has no presence) and poor allocations.

- We’ll characterize the e-comm launch schedule as a positive because it might ultimately help curb the market share loss by FY18. But, it’s going to be expensive to build (300-500bps of margin) before the company is even up and running and there is no guarantee that hibbett.com will be a destination for shoppers on the web when the selection is much better at a handful of competitive sites.

What We Didn’t Like

1. Comps were not a surprise given the preannouncement last week, but the composition of the quarter (negative comps in both June and July) leads us to believe that there is something more material going on with HIBB’s consumer group than it cares to admit. The long term trend in monthly comps is pretty clear and over the near term HIBB has a lot of wood to chop against mid/high single digit comps in the months of September through November. A 2% comp isn’t a heroic assumption for 3Q given the HSD comp to date fueled by the tax shift and the weight of August for the quarter at 4%. But, that means the company would have to print something in the 0.5% range in 4Q to get to flat for the year and that implies a 170bps acceleration on the 2yr trend line. We’d argue that the comp trend chart below is one of the ugliest in all of retail.

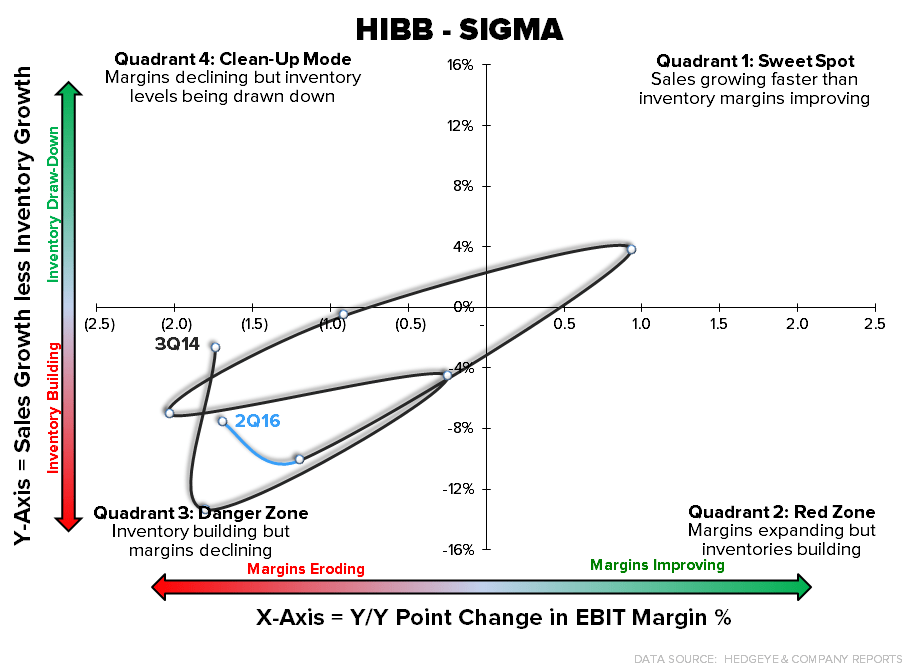

2. Gross margins have been down in 9 of the past 10 quarters and we think there is still room to move lower as the company continues to delever on the occupancy side with negative to LSD comps. The company needs at least a 3% to leverage on the gross margin line and we don’t have any confidence that the company can consistently deliver anything close to that number. Plus the inventory level is still far too high with the sales to inventory spread at -8% with merchandise that management clearly stated hasn’t resonated with customers.