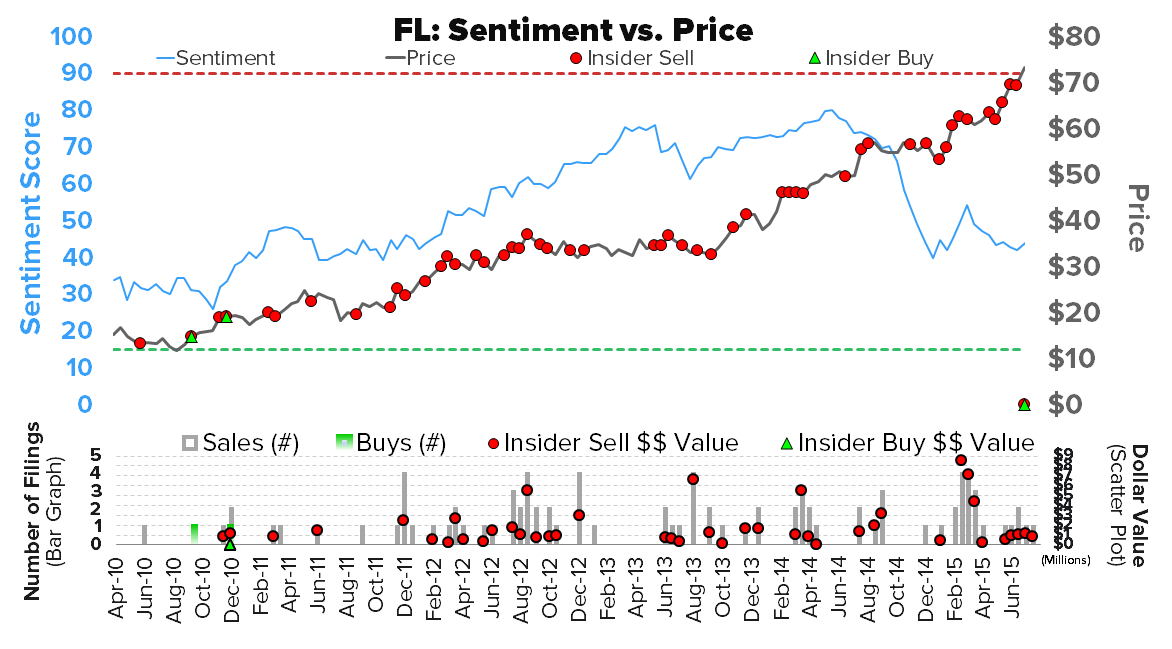

We’re adding FL to Hedgeye’s Best Ideas list as a short. Let’s be clear about something first…We’ve been actively talking about FL as one of our better short ideas since the start of the year. See our note below from March 4th. In other words, we thought it was a short $15 lower than where it is today – and were (too) early. The long-term (TAIL) call was crystal clear to us then, as well as the risks to the business model that are not being priced in to the stock. But we were less certain on near-term drivers to bridge the TRADE call with the TAIL. Now, however, we think the intermediate-term picture is much more clear, at least from where we sit, and we think that returns will head lower by the end of this year (retail stocks rarely go up when returns go down). All in, if we’re wrong in our analysis, we think the upside is $75 (15x $5). If we’re right, we think it can revisit $50-$55 (12-13x $4.00), at least 3 to 1 downside to upside.

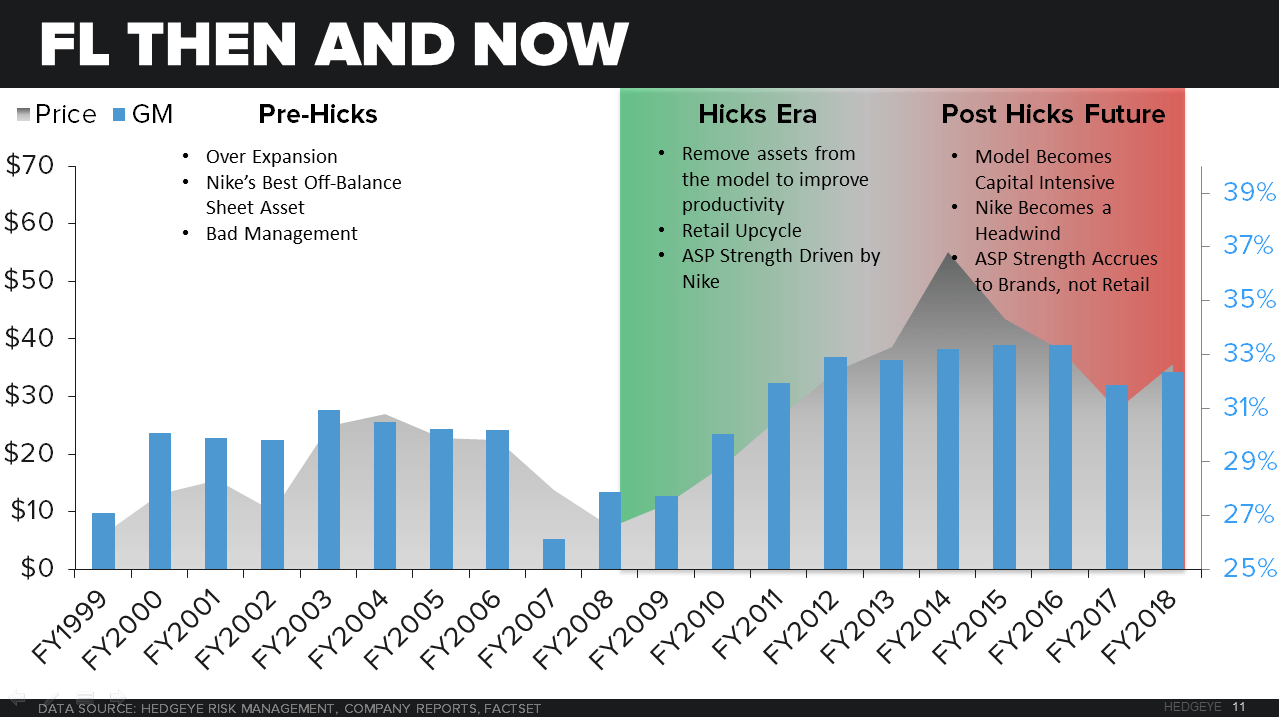

The best characterization of our FL call is that the company has done everything right over this economic cycle, such that it took net margins from -2% to +7%, and drove RNOA from 5% to 28%. As such, FL is sitting today at a peak multiple on what we believe to be peak earnings (and almost certainly peak earnings growth). The problem is the lack of runway in key earnings drivers, like a) changing up store banners, closing underperforming assets, and taking Nike up to 80% (from 60%). They were all tremendous profitability and margin enhancers. Unfortunately, they are irreplicable. There are almost no more stores left to close outside of the normal course of business, asset swapping opportunities between banners (Locker, Lady, Champs…) are few and far between, and Nike shifting above 80% of sales – already an exceedingly unhealthy level – is very slim. In fact, one could argue that FL is Nike’s best off-balance sheet asset.

To own FL you need to believe that the company can a) grow square footage (capital intensive and risky), b) comp mid-single digits for multiple years (unlikely), c) drive gross margin meaningfully higher (Nike won’t allow that, and FL’s .com business is not margin accretive), d) meaningfully leverage SG&A (but its’ sub-20% SG&A ratio is already the lowest in retail), and/or e) significantly boost asset turns (but capex is rising and management noted that inventory turns are ‘tantilizingly close’ to their goal).

This went from being an average company driving 20-30% EPS growth with less capital, to one that has to spend more just to maintain a 10% earnings growth rate. We think we’re right in between those two stages now, and the ownership characteristics are probably very different as we move from one to the other. That’s probably supported by today’s price reaction – with FL trading down despite an incredibly impressive 22% EPS beat.

Our Previous Note on FL from March 4

FL - Why We Think FL Is A Short

Conclusion: The biggest pushback, by a long shot, on our FL short call is timing, and how long we have to wait for it to play out. While FL is unlikely to completely melt down this week on the print, especially 2-weeks ahead of an analyst meeting, we definitely think that the building blocks of our thesis will be incrementally evident in the quarter to be reported on Friday (as well as in the meeting on 3/16). But this is a complex call with many layers that will peel off one at a time systematically as 2015 progresses, resulting in downward revisions and revealing a down year in 2016. Ultimately we think it will result in consensus estimates coming down meaningfully for the first time in six years, and we’ll see both lower estimates and multiple compression. We get to $20 downside, and $6 upside.

FL remains one of our top short ideas, but it is also perhaps the most complex. It’s not just about Nike, or about Ken Hick’s leaving, or about e-commerce threats. It’s about this company just having come off a six-year run that was driven by a ‘perfect storm’ (the good kind) of …

a) Margins: economic expansion and margin tailwind,

b) The Hicks Era: a new stellar CEO taking capital out of the model while simultaneously taking productivity and margins to new peaks, and adding 2,000bp to RNOA (RNOA to 25% from 5% pre-Hicks),

c) Nike Penetration: FL taking NKE to 70% of its inventory purchases from 56% – which has meaningful positive implications for gross margin,

d) ASP Cycle: Nike driving a 12-year ASP cycle which accrued to the retailers (like FL) just as much as it did NKE.

e)e-Commerce: Growth in e-commerce without meaningful brand competition.

But today, those factors have changed for the worse... (Here’s the links to our recent Black Book deck and audio presentation where we outline these factors in more detail.)

Call Replay: CLICK HERE

Materials: CLICK HERE

a) Margins: The post-recession margin tailwind is over. We need raw top line growth and productivity improvements to boost margins.

b) The Hicks Era:

1. Ken Hicks is gone. His team is still there. But we think that one of the highlights of the analyst meeting on March 16 will be how the company will be spending to grow. That’s fine, but keep in mind, it has just come off a period where it grew without spending and boosted returns by 2,000bps. Big difference – especially when it’s still sitting at a peak 15x p/e.

2. Also, there’s no more capital to pull away from this model. We outlined in our Black Book how the fleet is largely optimized, and perhaps with the exception of some Lady Foot Locker stores, there’s little left to close or ‘rebanner’.

c) Nike Penetration: Is the next move in Nike as a percent of total higher, or lower? It’s lower. And, quite frankly, it’s HEALTHY for Nike to be a smaller percentage. It’s just probably less profitable. We actually have people tell us “I called Nike and they said the Foot Locker is a really important customer – and that your thesis is wrong’. That’s what Nike HAS TO say. They fight their battles in private, and win where it matters -- on the P&L and the balance sheet. At a minimum, Nike not going higher as a percent of total sales is a negative, as the tailwind that’s existed for half a decade has been underappreciated.

d)ASP Cycle: We’re in a 12-year ASP cycle. Chances are, there will be a year 13. And probably a year 14. This is a space where the tail wags the dog. As the brands spend up in R&D, they drive prices higher. But the difference is that we’re at a point where the higher prices will start to accrue disproportionately to the brands. They (especially Nike) finally have the infrastructure and the product tiers in place to grow their DTC businesses aggressively.

e)e-Commerce: And we’re already seeing this part of the story play out. The charts below show the yy change in reach for FL vs NKE (reach spread is defined as the percent of people using the internet that are using Footlocker.com/Nike.com today versus last year). This will accelerate. What this does is maintains the mid-upper price business for the retailers, but allows Nike to dominate the $160-$225 business on its own site. That’s a problem for FL as its ASP increase has not been broad based. It has been because the retailer added a better mix of shoes at extreme price points.

The biggest pushback we get on any of this is “yeah that’s great guys, but am I going to have to wait another three years before seeing this? Show me the near-term catalyst and roadmap.” Fair question (and trust us, it comes from 80% of the people we talk to). When all is said and done, though FL is unlikely to melt down this week, we definitely think that parts of our thesis will be evident in the quarter to be reported on Friday. But this call has many layers that will peel off (usually) one at a time systematically as 2015 progresses, and ultimately result in consensus estimates coming down meaningfully for the first time in six years.

We’re about in line for the quarter at $0.91 and 6% comp, but are 5% below the consensus for 2015. And by the time we look toward 2016, we’re at $3.46, 17% below the Street.

So what’s this worth? Not 15x earnings, we’d argue. But we’re not going to make a multiple contraction call. But the call we will make is one for lower earnings and growth, and once that is apparent to the Street, the multiple will follow. We think that 12-13x $3.60 in EPS by year end 2015 is realistic as the story plays out, or a $45 stock (20% downside). Looking into 2016, and the likelihood of a down year ($3.46 despite the Street's $4.17) we think we're looking at 11-12x $3.46, or a stock in the high $30s. All in, we're looking at about $20 downside over the next two years, with about $10 per year.

That's about 4.9x EBITDA and a 8% FCF yield, which seem fair for a zero square footage growth retailer with earnings that are shrinking. If we're wrong, we're looking at about $4.25 in EPS power. Keeping today's peak 15x p/e, that suggests a $64 stock. That's about $6 upside versus $20 downside. We think the path of least resistance is on the downside.