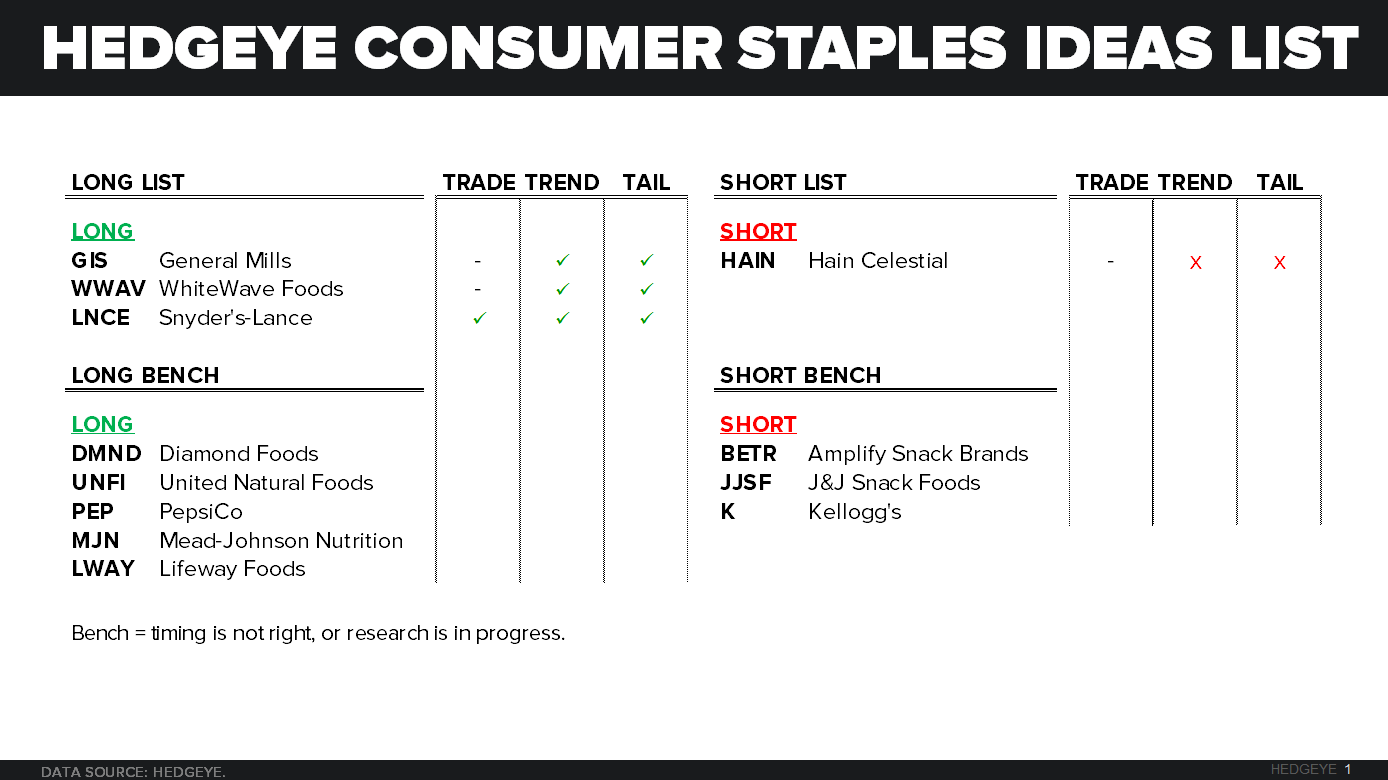

We are adding United Natural Foods Inc. (UNFI) to the Hedgeye Consumer Staples LONG bench. We intend to do a deep dive into this company over the next month, to get to the bottom of where we stand on it.

HEDGEYE’S EARLY LOOK

This stock has been beaten down way too far, due to an overreaction from the fallout of one big customer, Albertsons. The stock is down 42% from its 52-week high and down 24% over the last year.

Given the strong guidance for 4Q15 and the upbeat guidance heading into FY16 we are confident in the ability of this company to succeed. The thought that UNFI will continue to lose customers from competition is overblown and not very realistic in our minds. UNFI provides a high level service, offering a wide variety of over 80,000 products at industry leading prices. The industry is seeing continued growth in natural & organic, specialty, ethnic gourmet and fresh, all of which UNFI offers and can package together to provide retailers great value. Management is hinting towards positive results in the first two weeks of FY16, although only two weeks, it’s nice to hear of a marked sequential improvement.

UNFI has gone through a period of investment in capacity over the last couple of year. They are now past this, therefore capex with be falling down to more modest levels, about 0.6% - 0.7% of net sales. Free cash flow is going to start to ramp up as they invest less and leverage their assets more; this will lead to the possibility of doing bigger acquisitions.

Their main competitor, KeHe, recently was selected as UNFI’s replacement as the primary natural & organic distributor to serve Albertsons. It is our belief that KeHe is going to be busy integrating this business, therefore unable to go after any large contracts in the near future.

MANAGEMENTS ANNOUNCEMENT

On August 19, 2015, UNFI released preliminary 4Q15 and FY15 results as well as FY16 guidance (September 14th is the formal announce date). The company anticipates net sales in the range of $2.060 billion to $2.065 billion, versus consensus estimates of $2.051 billion. UNFI's diluted EPS for the fourth quarter of 2015 will be in the range of $0.72 to $0.73, which will match or exceed consensus estimates of $0.72.

Management also provided their FY16 outlook; the company expects net sales in the range of $8.51 billion to $8.67 billion, which represents an increase of 4% to 6% over FY15. Currently, consensus estimates for FY16 net sales are $8.596, so management is hinting at something slightly above that.

From listening to the pre-announcement conference call we get the feeling that they are leaving some in their pocket for a rainy day. There is a strong possibility of gaining new customers in the coming year, as well as acquiring a business or two as they hinted at in the call.

POTENTIAL UPSIDE

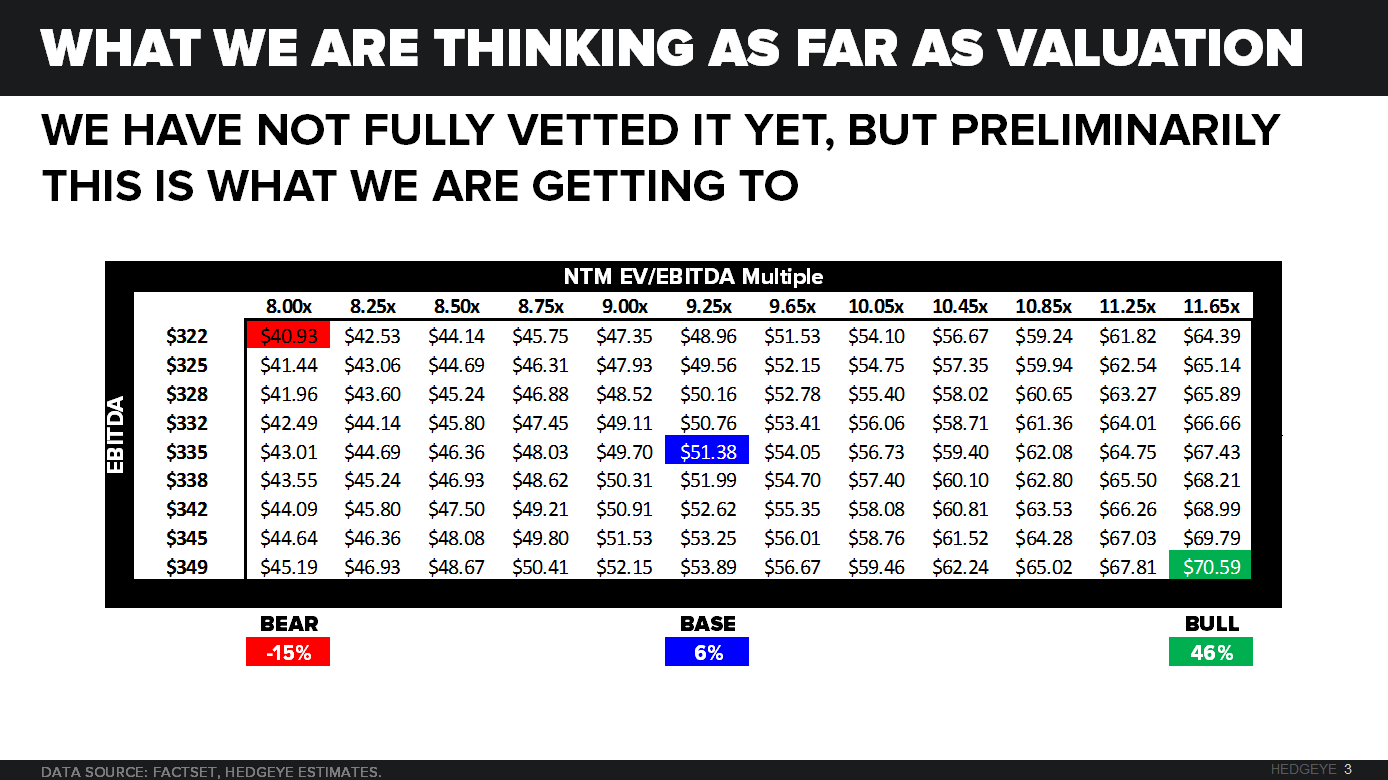

In early research, taking a conservative approach to multiple and EBITDA growth we are getting to a bull case of about $70/share or ~46% upside from here.

A lot more research to go through, but we are confident that the stock has bottomed, and has all negativity built in.

We will share pivotal information with you as we dig in here. Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst