"How would you like a job where every time you make a mistake, a big red light goes on and 18,000 people boo?"

-Jacques Plante

Pure poetry from a man who made a living taking vulcanized rubber off the kisser. For those of you who are not familiar with Jacques, he’s got enough Stanley Cup rings to fill a full fist, a plaque in the Hockey Hall of Fame, the 6th most wins in NHL hockey history and 7 Vezina Trophies (during his time it was given to the goalie with the best Goals Against Average). While his resume and verbiage could rival that of Jordan and Poe by far his biggest contribution to the sport was the permanent introduction of the goalie mask to the NHL.

The story of the mask’s inception is entertaining in its own right, but the resistance to change might be the better proverb to share. Plante had lobbied his coach Toe Blake (2nd most decorated coach in NHL History) to wear the mask prior to the 1959 season, but failed to gain permission due to obstructed vision and bravery concerns. On November 1st while playing a tilt at MSG, Plante took a slap shot to the face that required a good amount of cosmetic work to fix, and refused to reenter the game (there were no backup goalies) without a crude looking piece of molded fiberglass to protect his face.

The Canadiens won that night and the next 17 tilts before Toe Blake had his way and forced Plante to remove the mask. The Canadiens lost that night, and the goalie mask has been a staple of goaltender paraphernalia ever since.

Back to the Retail Grind…

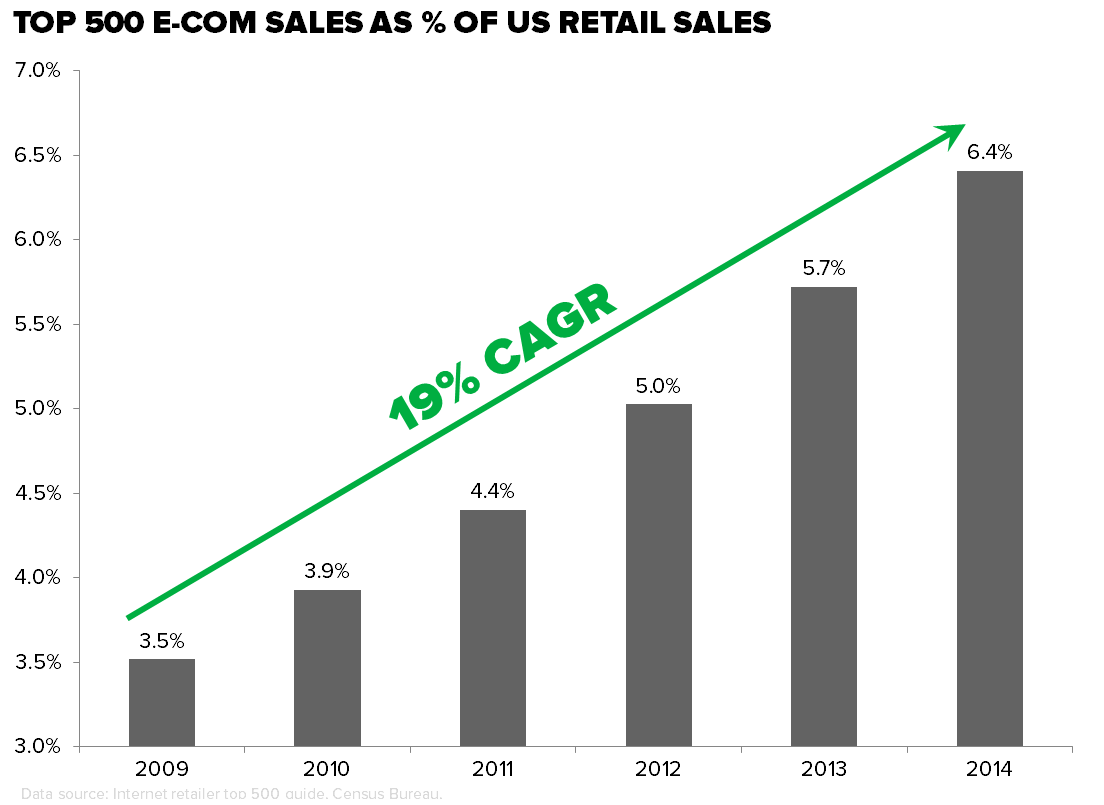

To borrow a Keithism – change happens slowly, then all at once. It was as true for Plante and the goaltending profession as it is for the retail industry. That’s never been more clear than it is today with the proliferation of e-commerce. To throw some numbers into the equation, the top 500 retailers on the internet generated $297 bil in sales in the US in 2014, almost 2.5x the $126 bil number posted in 2009. Good for a 19% CAGR. And it doesn’t appear to be slowing down as consumers continue to shift their spending behavior to the web.

That’s all well and good, but we have to say that we don’t envy retail CEOs who must now, like Jacques, sit in front of the ‘red light’ and navigate business models that were built for an entirely different generation of commerce.

The best example of that is our top short idea in the retail space – Kohl’s. The apparel retail concept was a cult stock back in the mid-90’s as the alternative to shopping at a regional mall. People could avoid the crowds as well as the 20-30 minute drive, and instead could drive 10 minutes to a local strip-center where they could buy decent brands at a decent price. The problem now is there is a new alternative and it’s called the internet.

The company has invested arguably too much capital to build a $2bil e-commerce business from scratch over the past 10 years for a business that a) has gross margins 1200bps below a traditional brick and mortar sale, and b) brick and mortar comps have been negative in 14 of the last 15 quarters as e-commerce has been anything but incremental. What’s the alternative? Lose market share at an accelerating rate.

We remain convinced that there are underappreciated risks (e-commerce is just one of them) to this model that will keep the company’s realized earnings power below $4.00 – pretty much forever. That’s notable when the Street is building up to a $6.00 EPS number over four years. If our numbers prove right then we’re probably looking at about an 11-12 multiple on $3 in earnings – or about $35.

As much as KSS is a loser, there are plenty of winners out there. Consider Restoration Hardware. While KSS is saddled with a legacy infrastructure built for an increasingly economically irrelevant generation, RH is recreating its store base for the next generation’s core spending demographic.

Yes, much of the growth profile of the company is based upon 30%+ square footage growth as the company blows out its real estate profile with 50,000 square foot stores as opposed to the legacy 8,000 foot stores (that were too small – only able to showcase 10% of the company’s product).

But answer me this…if a person buying a $3,000 sofa visits the showroom 3x, and then makes the purchase online – is it a store sale, or an internet sale? We really don’t care, and neither does Restoration Hardware. They call it profit, and we call it outsized stock performance. That’s why nearly 50% of its sales come through via internet – the highest in retail second only to Amazon.

By 2018, we’re looking at $11 per share in earnings for RH in 3-years’ time, which compares to the consensus at $6.00. Yes, we’re 80% above consensus. If we’re right, this should be a $300 stock. That’s why we won’t buy the argument that the stock is ‘too expensive’. It’s the same reason why we cringe when people say KSS is ‘too cheap’.

When all is said and done retailers who are able to build a scalable model harnessing the power of both brick and mortar and the internet while driving sales and profits won’t be hearing the boos.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.14-2.24%

SPX 2071-2107

VIX 12.31-14.81

Oil (WTI) 41.01-43.28

Gold 1081-1130

Copper 2.26-2.35

Best of luck out there today,

Alec Richards

Retail Analyst