Conclusion: The stock is at an all-time high for a reason – the company executes better than perhaps any retailer out there. That said, its ‘beat and guide down, and then beat again’ trend might come to an end sooner-than-later. Comps look fine – more than fine, actually. But the pressure on the cost side is simply unmistakable. With that staring us in the face along with a 21x multiple, we think there’s higher-quality growth elsewhere at a better price.

What We Liked:

- Tough to argue with a company that is printing accelerating comps in this environment. TJX doubled up the consensus number for the quarter at +6% which was a 150bps acceleration on the 2yr trend line. Every segment accelerated sequentially in the quarter on a 2yr basis except for Europe which held flat at 5.5%.

- Home Goods comps continue to rip at 9% for the quarter. While not a direct competitor to the RHs of the world, this coupled with the retail sales data which ticked up on both a 1 and 2yr basis in July gives us a lot of confidence in the strength of the home furnishings space (at least on the décor side of things).

- Guidance looks beatable. At least on the comp line. 3rd quarter guidance assumes a 200bps deceleration on the 2yr trend line similar to the what guidance implied in 2Q15. The company has beat guided comp numbers by a minimum of 160bps over the past 3 quarters.

What We Disliked:

- Cost pressures from both wage increases and incremental investments in the business led to the worst deleverage we’ve seen in a quarter since 2012. That’s just heating up for TJX and will continue to be a headwind – especially on the wage side – until it laps the $9.00 minimum wage it put into effect in June of 2015. Check out the table below – SG&A growth has gone from 3% to 11% in just 3 qtrs. Today we saw both WMT and TJX feel a considerable amount of pressure from wages – any other retailers operating in this space were officially put on notice.

- Guidance for 3Q leaves a lot to be desired. The $0.07 guide down implies -3.5% to -6% EPS growth on a 2-3% comp with 13 percentage points of growth being taken out due to Fx, wage inflation, incremental investments, and pension costs. That pushes growth expectations into the toughest comp of the year in 4Q. Comp guidance is likely conservative, but costs are what they are.

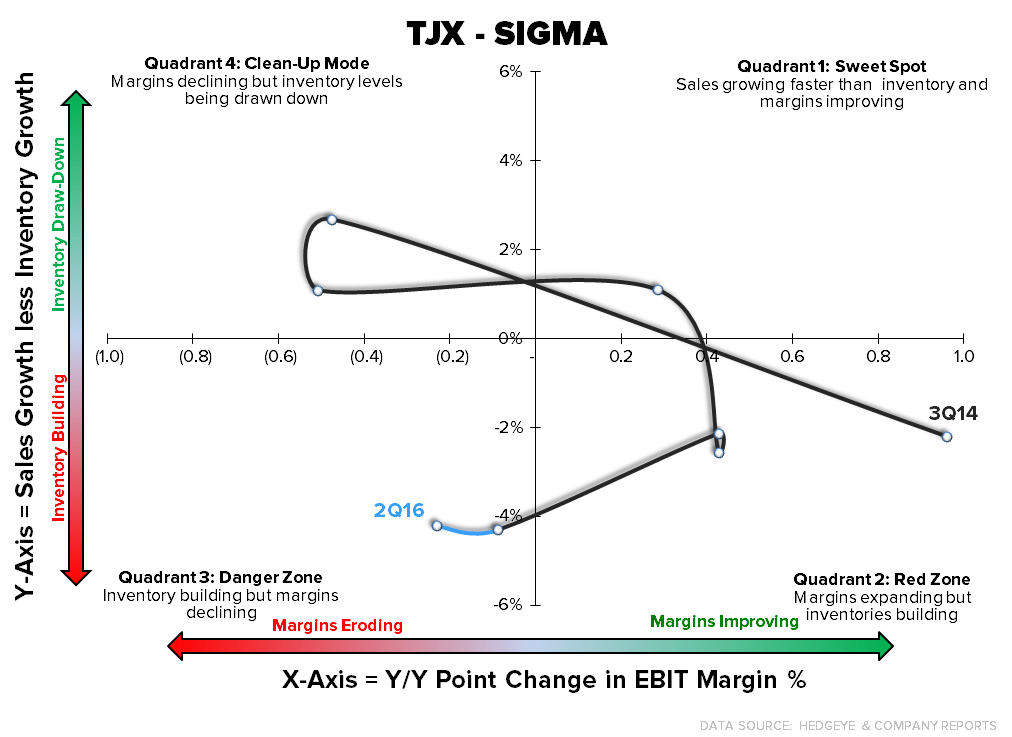

- The SIGMA chart, which triangulates inventories, sales and margins looked a lot like the department store group with margins eroding and inventory growth ahead of sales. That’s not a great set up for TJX if we believe the 2-3% comp guidance. Especially when you consider the cost pressure on the SG&A line. We know that TJX can manage through it, but we’re more worried about what happens if the department stores become overly promotional.