KEY POINTS

- F1Q16 = LANGUAGE BARRIER: Mgmt failed to properly flag the financial impact of the suspension of its lottery business and the transfer of its SME business to Ant Financial. Collectively, these headwinds hampered total revenue growth by 8 percentage points, leading to F1Q16 revenue growth of 28% vs. consensus expectations of 33%. Note that we were also taken by surprise (covered Short) since we didn't understand the financial impact of the suspended lottery business either. These lapses in communication could become a recurring issue since BABA is a foreign company (less stringent reporting requirements) that doesn't provide financial guidance.

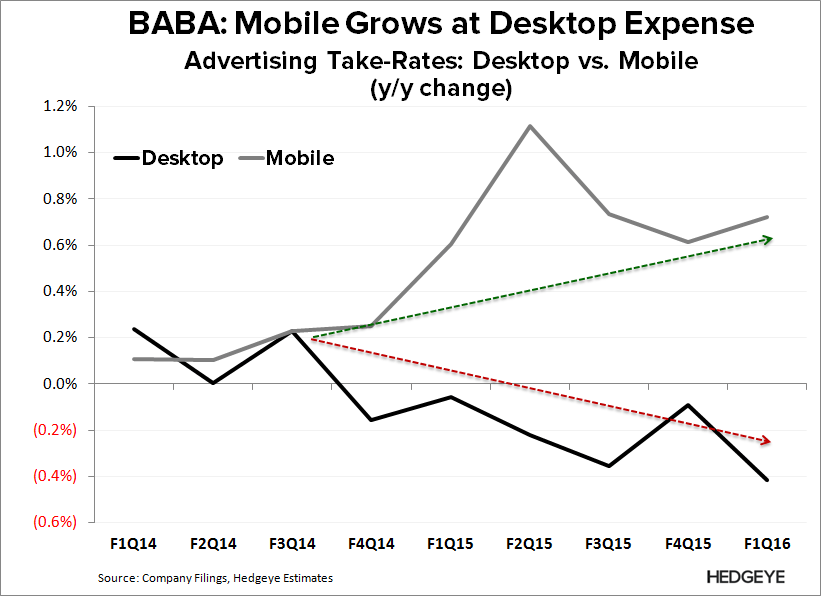

- FUNDAMENTALS STILL SOFT REGARDLESS: China Retail revenue growth still decelerated to 29% (ex lottery); below street expectations of 31% that we thought were light heading into the print. That compares to 32% and 39% in F3Q15 and F4Q15, respectively. GMV continued to slow, growing 36% y/y (ex lottery) vs. 40% and 49% in in F3Q15 and F4Q15, respectively. Take-rates also inflected lower on a y/y basis, with desktop take-rates declining at its sharpest y/y rate in BABA's reported history.

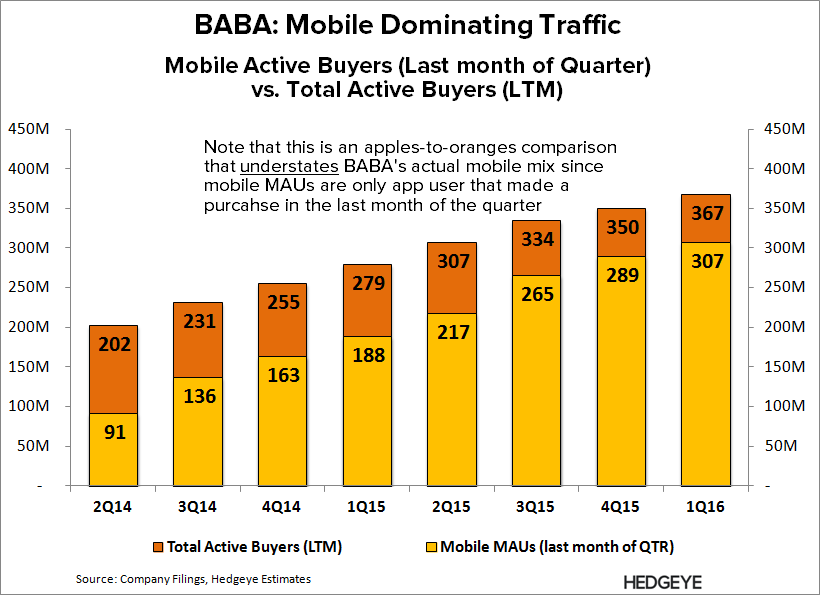

- MOBILE OR DESKTOP, NOT BOTH: We're referring to the mobile debate. The bull case is that mobile take-rates will ascend to desktop levels. Our bear case is that one grows at the expense of the other, and the two will most likely converge rather than meet up top since we believe that traffic mix is predominant driver of each (see note below for detail). We suspect mobile take-rates may start topping out with mobile traffic mix already at or above 85% (our estimate).

Let us know If you have any questions or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeInternet

BABA: Tactical Cover

07/16/15 08:46 AM EDT

BABA: The Mobile Debate

03/04/15 10:34 AM EST