Earlier today, CKR reported period 10 and fiscal 3Q 2010 same-store sales results. Comparable sales trends continued to decline on a 2-year average basis at both Hardee’s and Carl’s Jr. in period 10 and in Q3. Carl’s Jr.’s top-line performance continues to be extremely weak with period 10 and Q3 same-store sales -7% and -5.2%, respectively. On a 2-year average basis, these results represent a 155 bp sequential decline in period 10 and a 120 bp decline in the quarter.

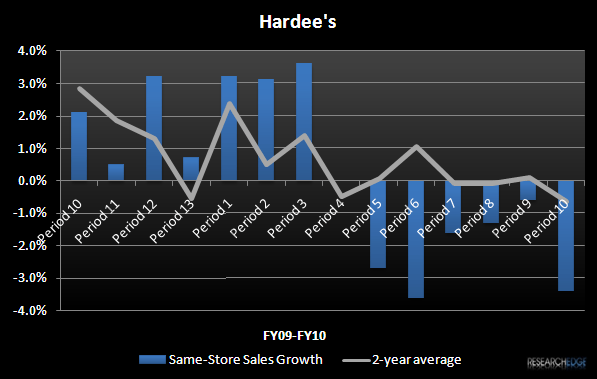

Trends at Hardee’s have slowed as well, though not to the same magnitude as Carl’s Jr. Same-store sales declined 3.4% in period 10 and -1.8% in Q3 with 2-year average results declining 75 bps on a sequential basis from period 9 and 55 bps from Q2. CEO Andrew Puzder again attributed the sales weakness to high unemployment and escalating industry discounting.

CKR also issued Q3 restaurant level margin guidance of 18% to 18.3%, implying 10 to 40 bps of YOY improvement. With blended same-store sales down 5.4% in the quarter, margin growth is impressive, particularly with depreciation expense as a percentage of sales expected to increase 80 bps YOY as a result of the company’s ongoing remodel program.

Lower food and packaging costs, which are forecast to decline 165 to 175 bps YOY as a percentage of sales, are helping to support margins in this tough sales environment. After Q3, CKR only has one more quarter of relatively easy food cost comparisons. In 4Q09, food costs as a percentage of sales were flat, but turned more favorable on a YOY basis in 1Q10 (down 60 bps). As this YOY food cost benefit moderates going forward, it will be increasingly more difficult for the company to maintain restaurant level margins with the current trajectory of sales trends. The first chart below shows how margins have continued to grow on a YOY basis despite the significant fall off in comparable sales trends (3Q10 YOY margin growth estimate reflects management’s 18%-18.3% restaurant level margin guidance). This is not sustainable. Positive sales growth will be needed to maintain margin growth trends.

Prior to Q3, lower YOY labor expense had helped to support margin growth for the last six quarters. This, too, was an unsustainable trend without eventual damage to the overall customer experience. To that end, I think it is encouraging that management is guiding to a 100 to 110 bp YOY increase in labor and employee benefit costs as a percentage of sales in Q3.