Today is, of course, Veteran’s Day, which is the annual American holiday that honors military veterans. November 11th is the anniversary of the signing of the Armistice that ended World War I. This Armistice was signed on the 11th hour of the 11th day of the 11th month in 1918. World War I has been called the Great War due to its massive scale. More than 70 million military personnel were mobilized in World War I and, sadly, there were more than 15 million casualties.

In the global stock markets this year, there is a more symbolic Great War going on. This war relates to stock market performance in the year-to-date. Despite a S&P500 that is approaching year-to-date highs, the major indices are well behind in the stock market performance battle this year as many global markets are up 2 – 3x the broad U.S. market performance.

The S&P 500 six day winning streak ended yesterday. The S&P 500 finished slightly lower on Tuesday after a big up day on Monday. Both the MACRO calendar and the earnings calendar was very light yesterday. Although we are waking up to some positive news out of China. In October, industrial production and Retail sales rose 16.1% and 16.2%, respectively. The futures are higher on this news. So while China looks poised for another victory over the U.S. stock market based on this internal growth, unlike military campaigns, this is not a zero sum situation. A strong and growing China is positive for the global economy, and U.S. equity markets, as we are seeing in the futures this morning.

Yesterday, the VIX fell another 1.3% and the dollar index was slightly higher yesterday.

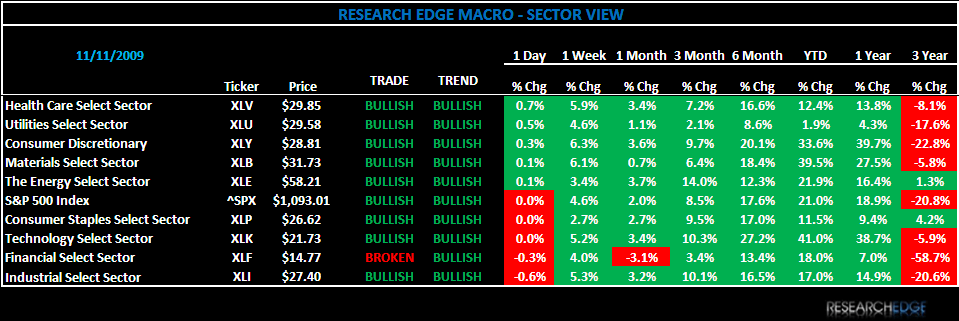

The three best performing sectors were Healthcare (XLV), Utilities (XLU) and Consumer Discretionary (XLY). The XLV was up 0.7% yesterday, the best performer on the day as defensive-oriented sectors found a bid. The Hospitals and Managed Care were among the best performers.

Within Consumer Discretionary, retail stocks finished higher for a fourth straight day. Priceline (PLCN) was the best performing stock in the ETF after reporting better-than-expected Q3 revenue and earnings. On the coattails of PLCN, Amazon and Expedia were also higher on the day

The worst performing sectors were Technology (XLK), Financials (XLF) and Industrials (XLI). While the XLF rallied at the end of the day, it was still the second worst performing index on the day. MBI was the biggest factor after reporting a loss of $3.90 per share, or $727MM. Not surprisingly, the continued pressures from a weak housing market are to blame. Regional banks were also weak on the day.

Today, the set up for the S&P 500 is: TRADE (1,070) and TREND is positive (1,034). The Research Edge quantitative models have 9 of 9 sectors in the S&P 500 positive on TREND and 8 of 9 sectors are positive from the TRADE duration. Financials are the only sector not positive on both durations.

The Research Edge Quant models have 1% upside and 2% downside in the S&P 500. At the time of writing the major market futures are poised to open up small to the upside.

The Research Edge MACRO Team.