Conclusion. KSS remains our top short. Do we think that the wheels will completely fall off the story with this Thursday’s print? No. But we don’t think we’ll see any notable upside, and we expect to see key metrics erode in support of our bigger call on the name that annual earnings are likely to never grow again. To put that into context, we’ve got numbers between $3.50-$3.75 from 2016-18. That’s 40% below the consensus, which has earnings marching over $6.00. The stock may appear cheap to some at an 11% FCF Yield (the most common bull case we hear). But we’d argue two things…1) while numbers are coming down, department store yields have gone well above 20% (just ask Dillard’s), and 2) our model has a lot less margin and cash flow, and only a 6.5% FCF Yield at $3.75 in earnings. Lastly, unlike with Macy’s and Dillard’s, there is absolutely no real estate play with KSS. So when all is said and done, we’d be short KSS into this print, and if the company throws the bulls a bone – as it does from time to time – then we’d get heavier on it. This is as much of a ‘core short’ as we can find in this market.

Here’s a summary of the key things we’re looking for in this quarter…

- The only way we expect to see the recent positive trend in store traffic to continue is if KSS gives it all back in lower merchandise margins.

- The only comp we’re likely to see will come by way of e-commerce, which is GM% dilutive by 1,000bp.

- Combining those two factors, we can’t reconcile how the Street could be looking for a 20bp improvement in GM% y/y.

- We’re also looking for growth in credit income (25% of EBIT) to continue to slow due to cannibalization from its Y2Y Rewards program, which should lead to contraction in its biggest profit center by year-end (without having to make a call on the credit cycle).

- There’s no real guidance one way or another with KSS, so it will be interesting to see how management handles Revenue expectations for 2H. The consensus is looking for an implied underlying comp acceleration from -1% to +3% over just two more quarters. That’s BIG for a company like KSS.

FULL DETAILS

Comps Get Tougher. The sales line should be the biggest ‘driver’ of this print on Thursday (with the caveat that earnings are really not growing). Expectations have come down considerably since 1Q where the buy side was looking for 4%+, and Consensus has walked numbers down from 2% (10bps lower then where it sat before the 1Q print) to 1.5% over the past month which helps explain the 5% sell off. The 1.5% seems achievable from where we sit, but assumes a positive 2yr comp -- something KSS has only printed once in the past 9 quarters (4Q14).

Then, comps get much tougher for the company with current consensus estimates assuming that the company accelerates sales sequentially on a 2yr run rate from the -0.9% number reported in the first quarter to 2.8% in the 4th quarter. We don’t believe that KSS’ current arsenal of sales drivers: personalization, loyalty, beauty, BOPIS is enough to reverse the 3yr trend of negative store comps.

If KSS has anything going for it this quarter, it’s that e-comm comps were extremely easy in the months of May and June (at 15% vs 30% in July). But, the company lapped the same benefit in the first quarter where comps were 12.4% and failed to realize the benefit. Traffic rank numbers which take into account both unique visits and page visits per user ended the quarter up in the mid 40% range, a slight acceleration from what we saw in 1Q. But, what we think is more notable is a) the accelerated ramp of JCP which is a big deal considering our works suggests that KSS was the biggest beneficiary of the JCP market share hemorrhage, and b) the relative underperformance of M compared to the group.

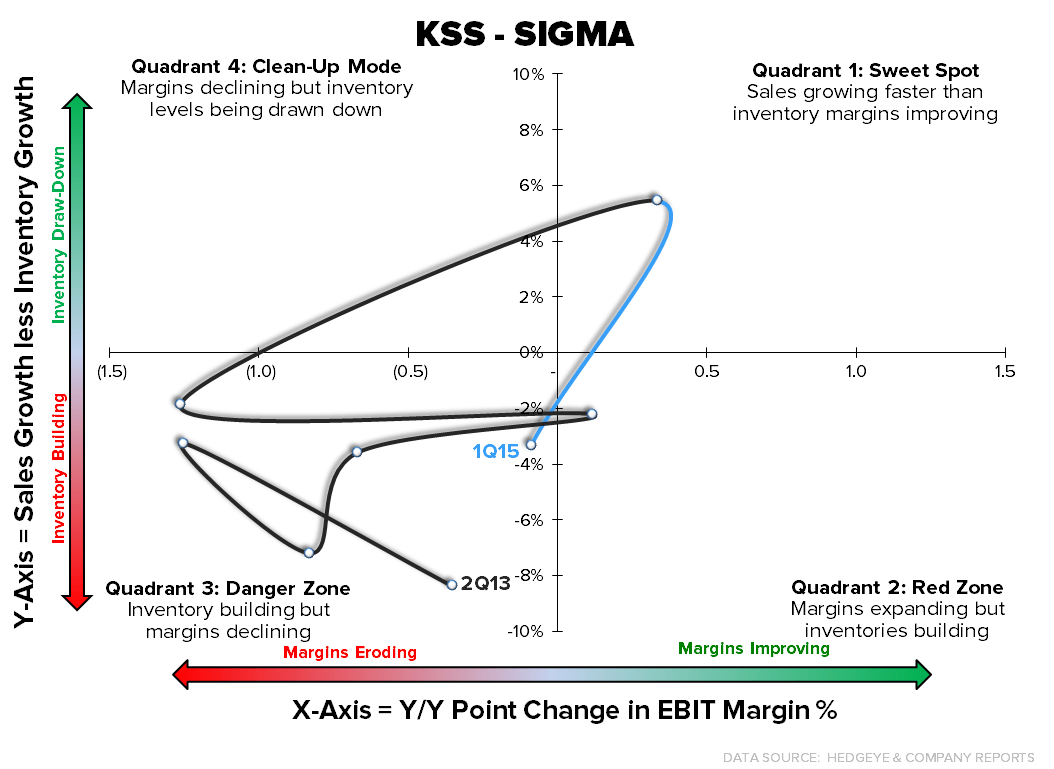

Gross Margin

Management’s bull case for this year was predicated on improving merch margins due to tight inventory management. That was well and good when the company entered FY15 with a sales to inventory at a favorable 5% (the first positive spread in over 3 years), but the SIGMA trajectory inflected in a meaningful way to the downside headed out of 1Q against the easiest comp of the year. That almost never equates to a positive gross margin event. Management tried to downplay the margin headwind of 5% inventory growth by calling out the growth in National brands which carry a higher AUR (units per store were up 1% vs. last year), but that also comes with its own margin pressure.

On the DTC front, e-comm caused 42bps of dilution in the first quarter, and assuming a 20%+ growth rate in the DTC channel (which the company no longer discloses) that amounts to 30bps of headwind for the year assuming of course that there is no further deterioration in e-comm gross margins. That’s a big hit for a company like KSS to handle especially when you consider that the company started this new rewards programs which equates to 5% cash back, National Brand penetration growing (a conservative 4bps to 7bps of headwind for every 100bps of mix shift), and the current inventory position of the company.

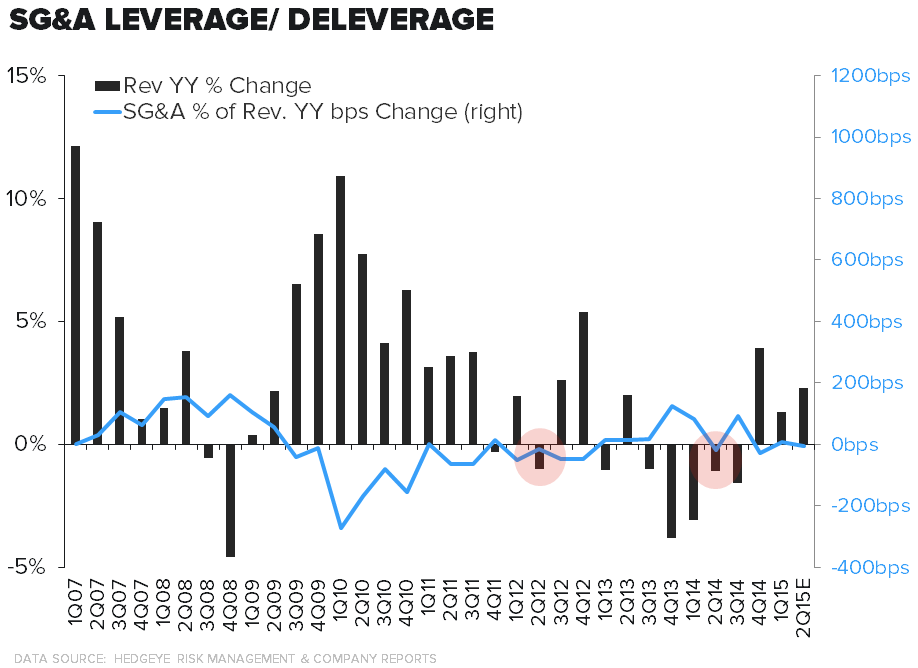

SG&A Comps

It’s tough to reconcile the company’s guidance of 3-4% growth for the quarter after management guided to 4%-5% growth in 1Q and printed 1.6%. But what we do know is that…

- Credit was a 13mm (70% of the dollar decrease) benefit in 2nd quarter of last year, that’s slowed over the past two quarters to 1mm and 2mm, respectively. We think that continues to march lower as the Yes2You rewards program continues to curb credit portfolio growth.

- 2Q14 was just the 2nd time in the past eight years that the company leveraged SG&A expense on a negative sales number.

- Employment costs are headed nowhere but higher. KSS management seems to be in denial about the added pressure from two of largest players in the retail space raising wages to $9, but the way we are doing the math by extrapolating the guided WMT cost pressure to the relevant number of KSS employees we get to 60bps of margin pressure and a $0.35 (8% hit) to earnings. That hasn’t manifested itself yet, and probably won’t until the retail hiring season kicks up in 3Q for BTS.

No Change To Guidance

No matter what the company prints on Thursday, it’s pretty clear that the company won’t make any material changes to its FY guidance. The company updated its guidance policy last year, and noted that it would only update its Fiscal year numbers once in the 3rd quarter.

Management

There hasn’t been a lot to like on the Management front at KSS over the past few months.

First, KSS ended its 14 month search for a new Chief Merchant when it decided to add responsibility to the plate of Michele Gass current Chief Customer Officer. With the entire global retail industry as a talent pool to source this position, Mansell picked the person who said very explicitly at the Analyst Day in October that 'love' would drive the business -- not once, or twice, but 19 times. Also, being a Chief Customer Officer (something that has no P&L responsibility or accountability) has nothing to do with being a Chief Merchant. This one will be hard for the bulls to defend.

And more recently, the company’s CIO, Janet Schalk, ended her 4 year tenure as CIO and jumped ship to Hudson's Bay citing a ‘great deal of uncertainty’ over the management transition taking place within the company centered around the hiring of a new yet to be named COO.