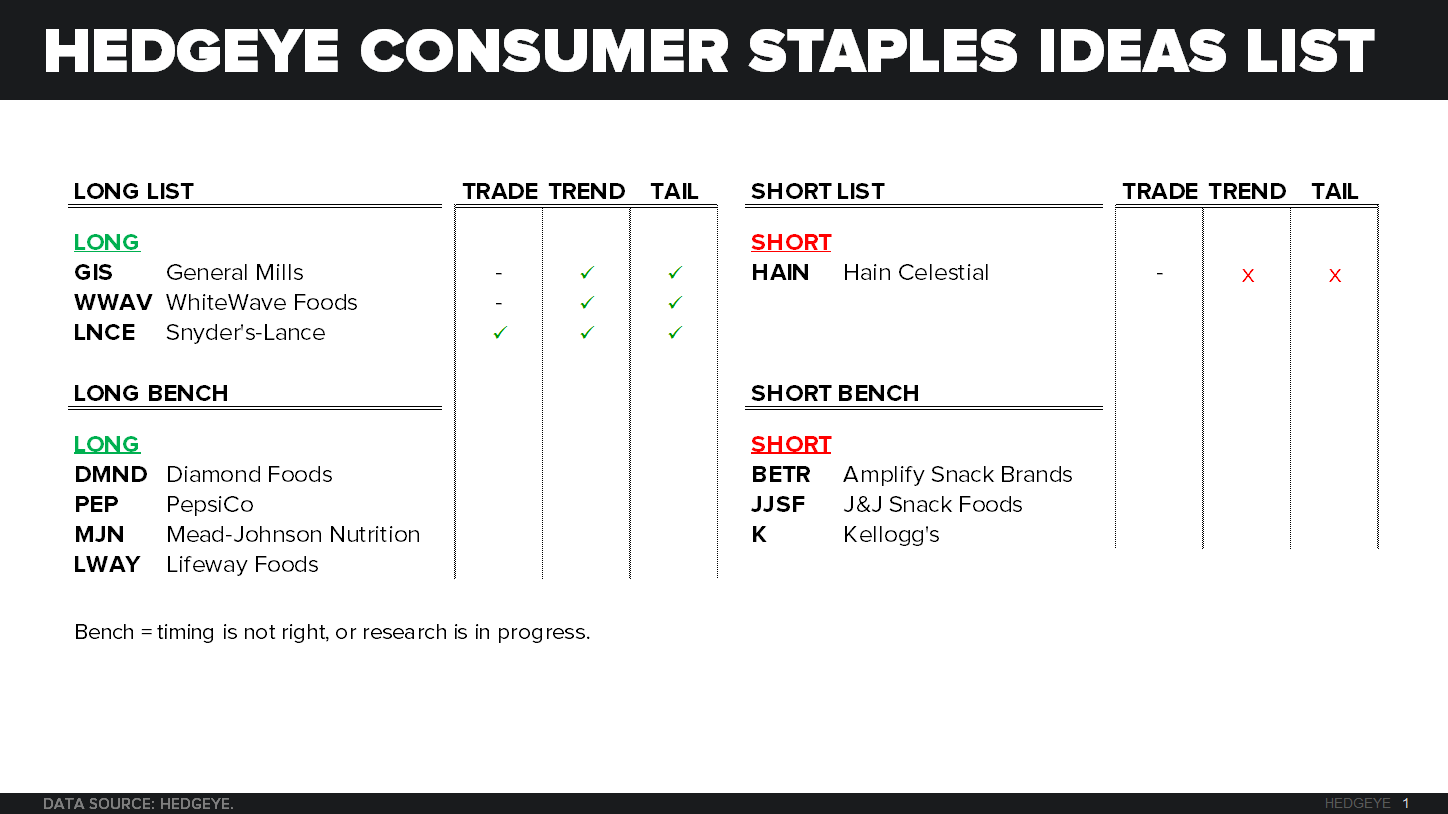

TAKEAWAY: We view LNCE as a high quality, small cap name in the Consumer Staples space. The company’s brands are well positioned in the snacking category to allow for sustainable volume growth and margin expansion for the next 3-5 years.

Snyder’s-Lance (LNCE) reported 2Q15 numbers yesterday after the close that beat the street on both the top and bottom line. As a result of this beat and a strong outlook for the next 12-18 months, we are raising LNCE up to the Hedgeye Consumer Staples Best Ideas list as a LONG.

We will dive deeper into this idea next Wednesday, August 19th at 11:00am ET when we present our Black Book on LNCE. Formal invite and details will follow later today.

HEDGEYE OPINION

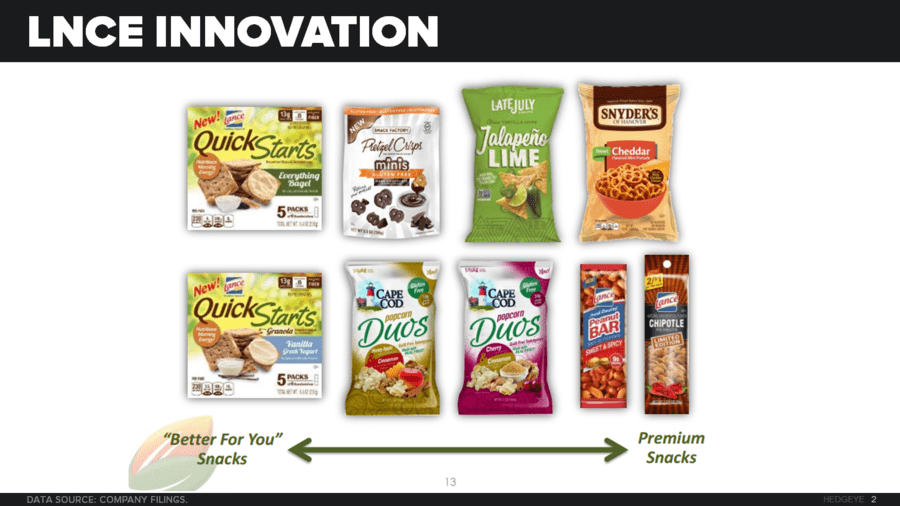

Snyder’s-Lance is a leader in the snacking category, their portfolio of brands is something that actually brings people to the center-of-the store. It is exciting to see the innovation they are implementing across the top brands as well as driving growth through increased distribution. There is still plenty of white space out there that LNCE can fill as they expand their operations. In early analysis we see 25%+ upside in the name, as we are confident the team can continue to grow organically, as well as acquire fast growing snacking brands to plug into their DSD network.

EARNINGS

As previously noted LNCE beat the street on both the top and bottom line. Reporting net sales of $431.4mm versus consensus estimates of $430.2mm and operating income of $32.3mm versus consensus of $31.0mm. In the quarter, management improved their operating margin by 50bps, as they leveraged the manufacturing footprint and continue to streamline operations. Moving down to EPS, LNCE beat the street by a penny, posting $0.27 versus estimates of $0.26. The great financial performance was coupled with impressive share gains by all of the core brands, which include; Snyder’s of Hanover, Lance, Cape Cod, Pretzel Crisps and Late July.

INNOVATION & EXPANSION

Innovation is a key source of growth, and they are showing their brands can expand well across categories. Cape Cod’s early days in RTE popcorn are proving to be positive, and they are spreading innovation across better for you snacking all the way to premium snacks. Seeing these actions shows they are most likely casting a wide net across the space when looking at possible M&A targets. At first thought, Popcorn Indiana, Angie’s, KIND Snacks, Justin’s and thinkThin jump to mind as possible targets.

In 2Q15, LNCE’s core brands net sales grew an impressive, 9.1%, with volume up 10% and increasing market share across the board. But there is still plenty of more room as they enter different channels. LNCE just recently entered e-commerce, it is growing well for them and expanding as their products cater well to this platform. Drug channel and C-store are also areas to improve as they are in most location but sometimes with just Lance or just Cape Cod, and management’s goal is to get broad distribution across all brands.

INVESTMENTS IN THE BUSINESS

From 2012 to 2014 LNCE spent $227mm on capital expenditures to update the manufacturing footprint and streamline the business. This was ~72% more than the previous three year period, as it was time to update manufacturing lines and infrastructure to improve efficiencies. Now that this spend has begun to taper off, they can focus their cash on growing the business. For starters they have updated their packaging across the core brands to increase consumer appeal on the shelf. They have also ramped up marketing spend both digital and media, to get in front of the consumer and drive awareness and trial of new products and old staples.

PORTFOLIO SHIFT

Just about one year ago on June 30, 2014, LNCE closed the deal to divest their private label business, which included two manufacturing facilities in the U.S. and Canada. Shearer’s Foods a subsidiary of Wind Point Partners purchased the business for $430mm. The private label business accounted for $287.8mm in net revenue in FY2013, 16.4% of the companies then $1.76bn in total net revenue. This was an important step for LNCE management, which allows them to focus 100% of their attention on the branded portfolio. Freed up cash to be put to better use on innovation and expanding the core branded portfolio of brands. As LNCE is lapping the one year mark of divesting this business the company is looking stronger than ever, very focused on growth and innovation.

MANAGEMENTS GUIDANCE

Management did not change guidance for 2015, they are still shooting for net revenues for the full year of $1.69 to $1.72 billion. The earnings per diluted share estimate range also remains at $1.11 to $1.19 and capital expenditures to be between $60 and $62 million.