RECENT NOTES

8/10/15 WWAV | KEEP RIDING THIS WAVE

8/6/15 WWAV | EARNINGS PREVIEW & POTENTIAL ACQUISITION

8/05/15 K | IS CEREAL RESUSCITATING THE COMPANY?

8/4/15 BETR | It’s Already Popped

7/30/15 GIS TO BUY WWAV | IN SEARCH FOR TRANSFORMATIONAL GROWTH

RECENT NEWS FLOW

Friday, August 7

WWAV | Reported 2Q15 results, which were highlighted by robust organic top line growth of +9%, but missed on the top line slightly. In addition to the impressive quarter, WWAV also acquired the Wallaby Yogurt Company (view our note here)

POST | Reported 3Q15 results in which management mitigated all of the potential disaster Avian Flu could have brought on them, and surprised the street. Most importantly they had great things to say about cereal. Declines in RTE cereal are slowing, and they are beginning to see an upward trend. Management noted that their biggest over performance versus expectation was in the RTE cereal category. As the industry is cycling over easier comps, “leaders in the category [GIS & K] seem to be reinvigorating their spending behind the category and it seems to be working.” (click here for news release)

Wednesday, August 5

BETR | Tumbled in its opening day of trading, down roughly -7%, never trading above their IPO price of $18 per share (click here for article, or here for our note on the IPO)

K | Upgraded to buy from neutral at Citi, target increased to $80 from $66

Tuesday, August 4

HSY | Introduces latest BFY granola bar offering (click here for article)

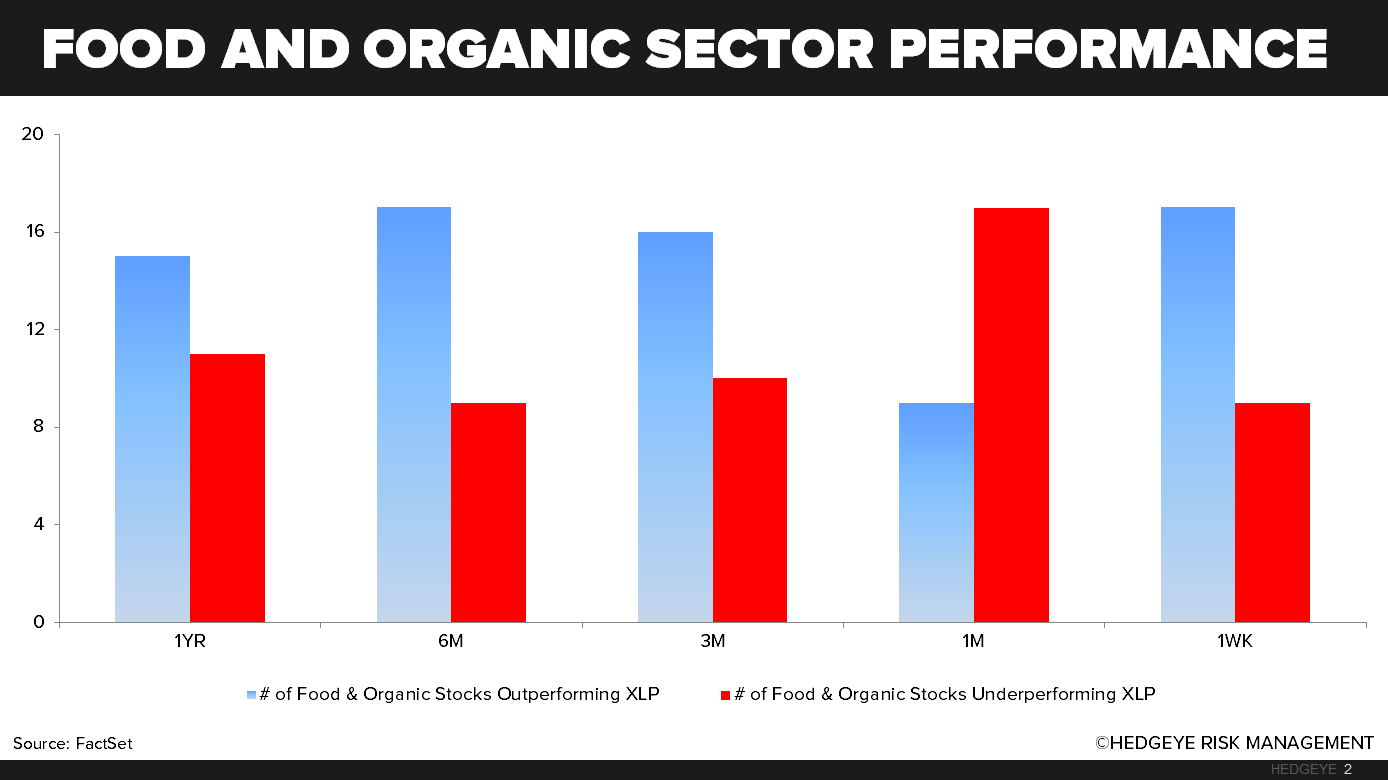

SECTOR PERFORMANCE

Food and organic stocks that we follow outperformed the XLP last week. The XLP was down -0.3%, the top performer from our list was Boulder Brands (BDBD) posting an increase of 11.3%, after announcing the engagement of William Blair to explore strategic alternatives for some of their brands. Worst performing company on our list was Amira Natural Foods (ANFI), which was down 21.7%.

QUANTITATIVE SETUP

From a quantitative perspective, the XLP remains bullish on a TRADE and TREND duration.

Food and Organic Companies