WhiteWave Foods (WWAV) is on the Hedgeye Consumer Staples Best Ideas list as a LONG.

HEDGEYE OPINION

WWAV continues to impress us with their robust high-single digit to low-double digit organic growth rate. This quarter, in addition to their robust organic growth, WWAV also acquired the Wallaby Yogurt Company, an organic Greek and Australian style yogurt and Kefir beverage company. This is a continuation of their string of pearls approach, to adding top brands to their portfolio. WWAV continues to be a top company on our list for their future growth prospects both organic and through M&A as well as their possibility of being acquired. The stock traded a little weak through the day after earnings, but this company is still in BEAST MODE, no need to think anything different.

PERFORMANCE

On Friday August 7th, WWAV reported a strong 2Q15, featuring robust organic growth, as well as a new acquisition. Reported revenue rose 10% to $924mm, slightly below consensus estimates of $927.2mm, organic revenue grew to $911mm, up 9% YoY. Operating income beat estimates, reporting $84.9mm versus consensus estimates of $83.1mm, representing a 20% increase YoY. WWAV beat the street estimates on the bottom line by a penny, reporting adjusted EPS, excluding the China JV of $0.26 versus consensus estimates of $0.25, representing an 11% increase YoY.

This robust growth was slightly hampered by a slowdown in the America’s Fresh Foods segment. The segment experienced tough crop conditions in the quarter in which they weren’t able to harvest a large amount of their fruit supply. All said and done, the segment sales were down -1%, but operating income was up 11%, as they continue to streamline the manufacturing process and exit lower margin business. Since the supply issues on organic salad last quarter, the team has worked diligently on regaining distribution and are seeing strong results.

Horizon Organic sales were up 15% in the quarter driven entirely by price, as organic milk supply continues to be constrained; consumers don’t seem to care about the rising prices. Horizon center-of-store products are meeting the increased expectations set out in the last call, and are well positioned heading into the back to school season.

The European Foods and Beverages segment is growing at an unbelievable 23% on a constant currency basis. This growth is purely volume driven across all markets and product lines. This is the 4th consecutive quarter of 20%+ growth for this business and they are still expanding into new countries. Just recently entering France, and although in its early stages results are positive. Alpro is also working on new products such as drinkable yogurts that are coming out towards the end of the year.

Management is pushing costs out of the business. In the quarter they delivered 75bps of margin expansion, and are expecting to deliver that or more on a full year basis. Increased volume going through the system has been a key driver of cost savings as they further leverage their assets. In addition, the company is looking to invest in expansion, building out packing and manufacturing lines, warehouse space and further automating operations to increase efficiency.

ACQUISITIONS

In the quarter WWAV completed the acquisition of Vega, for $550mm. The brand has $100mm in sales over the LTM ended June 2015, experiencing 60% constant currency sales growth year-to-date June 2015. Management and Hedgeye are very excited about WWAV adding this brand to the portfolio. Management spoke to its vast expansion capabilities across the U.S. as well as international growth possibilities, such as tacking it onto the Alpro distribution network in Europe. Most importantly this is a margin enhancing, accretive acquisition to WWAV.

In addition to the completion of the Vega deal management also entered into an agreement to acquire Wallaby Yogurt Company for $125mm. An organic Greek and Australian style yogurt & Kefir beverage Company. Along with the great brand and growth prospects, as part of the deal WWAV also receives their yogurt manufacturing facility in the on the west coast. Now with their prior facility in Pennsylvania and the newly acquired one in California, they will be able to expand distribution rapidly. Please view the below case study for greater detail:

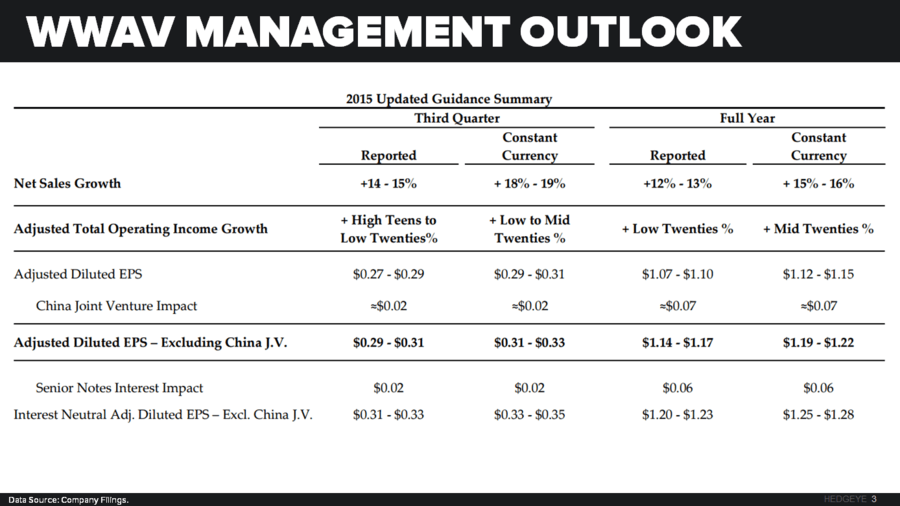

MANAGEMENT GUIDANCE

After increasing full year guidance coming out of 1Q15 earnings, management is increasing guidance again. They now project reported net sales growth to be +12% - 13% versus prior projections of + low double %, and an organic growth rate of +10%. Increasing adjusted EPS excluding China JV to $1.14-$1.17 from $1.10-$1.14.