Below are Hedgeye analysts’ latest updates on our fifteen current high-conviction long and short investing ideas as well as CEO Keith McCullough’s updated levels for each.

Please note we added RH (Restoration Hardware), XLU (Utilities Select Sector SPDR Fund) and LKND (LinkedIn) this past week.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

RH

Please note we added Restoration Hardware (RH) to Investing Ideas on Friday. Click here to read Hedgeye CEO Keith McCullough's explanation, a Stock Report detailing the fundamental view will be published later.

LNKD

We added LinkedIn (LNKD) to Investing Ideas earlier this week to read the full Stock Report click here.

LNKD continues its post-print sell-off following undue conservatism on its 2015 guidance. The issue is that LNKD is crying wolf two quarters in a row, and some are concerned that there is a bigger issue at work, or that management will continue to hamper the stock with undue conservatism. LNKD’s fundamentals remain solid, and we believe it salesforce investment will pay off in 2H15. More importantly, we suspect management has learned its lesson, and there won’t be any ambiguity on its next guidance update.

ZOES

We view ZOES as one of the best small cap growth names in the Restaurant category. The company is set-up for long-term success for the following reasons:

- Superior brand positioning

- Management philosophy and execution

- Unit opening geographic profile

- Early-stage average unit volumes and returns

FNGN

Financial Engines (FNGN) formalized the announcement of Wells Fargo providing their independent advisory services in their 2Q15 earnings presentation this week. While the deal had been speculated by a news outlet during the course of the quarter, the formal announcement adds a solid fundamental catalyst guided to come on stream by the "middle of 2016."

According to the most recent Cerruli retirement survey, assets under administration at Wells currently stand at $168 billion (this counts only 401K plans over $100 million). This would be +16% on the firm's current assets-under-contract of $1.04 trillion. Thinking about a 2 year conversion rate at 13.3% of future assets-under-contract to assets-under-management (at the firm's current realization rate and net margins), puts the Wells opportunity at $0.11 in earnings per share. The firm's TTM EPS is currently $0.93, putting the full potential at +11% accretion.

The market internals for the stock are still way too bearish in light of this announcement and with over 25% of the float short, we continue to see asymmetric upside. Historically, the 20% short interest level has been the buy signal in FNGN stock, which has remained the case throughout the course of this year. In addition, with trading volume having dried up over the past 90 days, the days to cover has now doubled this year to 40.2 days. We are valuing shares on an assets-under-contract opportunity of $1.3 trillion. With the new Wells announcement already getting us half way there, and the ongoing overly bearish market structure of the stock, we continue to see upside.

The Wells Fargo announcement this week is providing access to another $160 billion of 401K assets under administration to sell into for FNGN. Wells is currently the 5th largest 401K administrator, providing a solid opportunity for Financial Engines:

Historically, the 20% short interest level has been a good buying point for FNGN, a level where the 2015 ascent in the stock started again. The current short interest percentage is 25%, again a good entry for stock bulls.

HOLX

HCA had some potentially chilling commentary on their earnings call this week and introduced a new term, #ACATaper. The pace of growth in the U.S. Medical Economy has been on a tear as the newly insured rolled into physician offices and hospitals. We’ve been highlighting in recent weeks the transition from an #ACATailwind to #ACAHeadwind, or as someone on the HCA call named it, the #ACATaper.

In an analysis of the demographics of the newly insured, Pap testing, HPV, and mammography were at the top of the list of products that would be positively impacted by the ACA. As we reach the #ACATaper stage, will HOLX take a hit to their Diagnostic segment? It is possible, in our view, but so far a minor risk. As we learned last week from a lab operator, Qiagen is likely to continue to cede their 14% HPV testing share to HOLX. So while the #ACATaper appears to be finally here, there are offsets.

On a disappointing note, our 3D Tomo Tracker update for July came in at 24 facilities. Down sequentially from June, and down from a peak of 54 in May. Our forecast algorithm, which is based on these updates, remains unchanged. While 20 is low, it is probably a blip in the longer term adoption cycle. Also we analyzed the MQSA data (http://www.fda.gov/Radiation-EmittingProducts/MammographyQualityStandardsActandProgram/FacilityScorecard/ucm113858.htm) which strongly suggests facilities are purchasing ~2 mammography units each, which is above our current estimate.

FL

We’re coming off a six-year period where taking capital away from the business improved productivity and profitability. This happened while industry margins staged a massive recovery, and increased Nike allocations (now 73% of purchases and close to 80% of sales) drove FL’s ASP (Average Selling Price) higher. Sales, margins, ROIC all benefitted.

The athletic footwear industry’s 12-year ASP cycle is getting long in the tooth. If it continues, it is going to accrue more to the brands (Nike, Adidas, Skechers, Under Armour) – not the retailers. Now FL has to inject capital (largely through remodels), and hope revenue follows. Aside from gas prices, there are no more margin tailwinds. The Nike ratio can’t go much higher than 80%. Ken Hicks pushed the enhanced Nike agenda; seeing the positive Nike ASP/margin impact approaching peak likely played a role in why he cashed out.

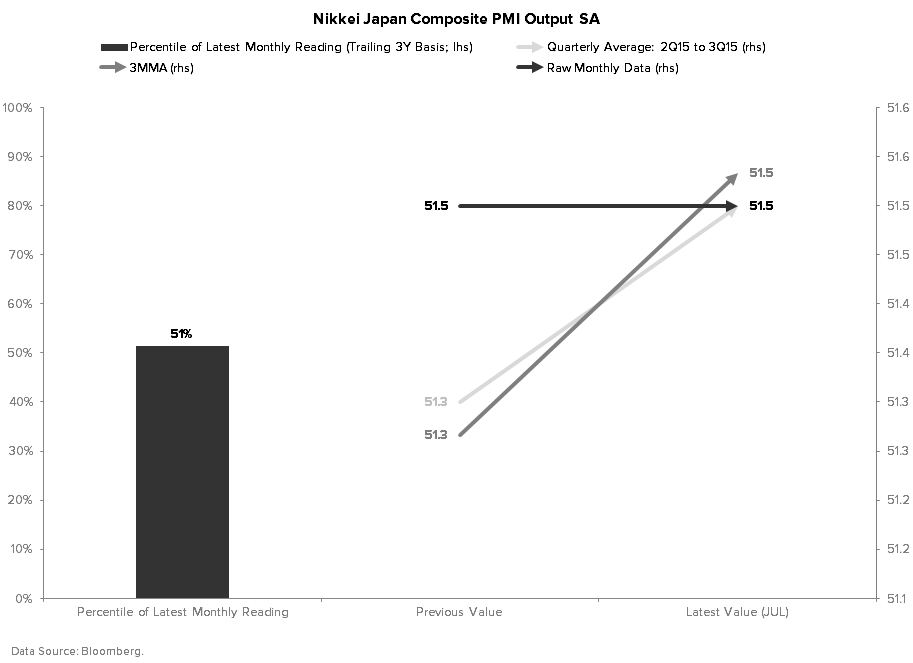

DXJ

In Japan, the key highlight (or lowlight, if you will) of the week was the BoJ’s decision to leave its monetary policy unchanged on Friday, as expected. The board also reiterated its optimistic outlook for the economy, as was also expected. Given the in-line nature of the event, there was little reaction in the market place following the release or Kuroda’s press conference.

Elsewhere in Japan, this week’s July PMI data came in mixed and highlights the uneven and fragile nature of Japan’s recovery. Specifically, the manufacturing/production/export side of the economy continues to hum along, while services/consumption economy peters out amid tepid wage growth – effectively netting out to stagnation.

All told, we reiterate our bullish bias on Japanese shares (DXJ) and expect QQE expansion by year-end/early-2016 as both reported inflation and inflation expectations continue to trend lower. We like the fact that Japan had been showing cyclical improvement, but the backstop of easier monetary policy is also supportive to the extent the rate-of-change in Japanese growth flat-lines.

VIRT

The short case on Virtu Financial (VIRT) started this week with an earnings miss and a sizeable decline in the firm’s important foreign exchange (FX) business. The company missed overall 2Q15 expectations by 10% on the top line and 15% on the bottom line in only the second publically traded quarter for the firm. The big eye sore in the release was the firm’s FX business which dropped -43% sequentially with daily revenue production hitting just $392,000 per day from $691,000 per last day quarter. While sequential machinations in trading businesses are quite usual, the flat year-over-year growth in FX (at 25% of top line revenue) is not enough to support the stock’s sky high multiple.

While the -10% drop in VIRT shares following the release is to be expected, we still see further downside. The company runs a cyclical trading business (proved out by this week’s results) on very thin levels of capital, on top of a multi-level shareholder structure (the newly public Class A shareholder group has just 11% economics of the business and only 2% voting power). The long term implication is that if there were ever a trading loss within operations the company would struggle with liquidity and the long term returns of stocks with multi-class equity structures is just half of single class structure. We see incremental downside of between -10-40%.

Long term returns of controlled companies have averaged just over half that of non-controlled companies:

Depending on how we toggle earnings power and the stock’s multiple, fair value is 10-40% lower (we already got a 10% move down this week):

PENN

PENN has emerged as the first domestic gaming growth story in 10 years with a new casino in Massachusetts this year and one in San Diego next year. Meanwhile, regional gaming trends have stabilized, providing near term earnings visibility and upside. Upcoming catalysts include the monthly release of State gaming revenues for July, including Massachusetts, and positive earnings revisions.

GIS

General Mills (GIS) remains one of our favorite names in the Consumer Staples sapce.

FY16 Hedgeye Guidance ―

Looking into FY16 we are excited about the possibilities. Management is working hard on their “Consumer First” initiative and making great changes to current product while also introducing new products. Below is not a comprehensive list but some of the biggest things that we are looking forward to this year:

- Yoplait in China

- Gluten-Free Cheerios

- No artificial colors or flavors in the cereal

- Granola innovation / Muesli

- Greek Plenti / Whips

- Original yogurt sugar reduction

- Renovation on Grain Snacks

- Strong push on Natural & Organic products

- Delivering Value to consumer on brands like Totino’s and Hamburger Helper

- Bringing U.S. innovation International

Bottom line is they are still struggling; we don’t want to shy away from that. But the core of the portfolio is growing and management seems to be working tirelessly on implementing changes to grow the rest of the portfolio, especially cereal. We also still believe that to have continued growth into the future a sizeable acquisition or divestiture would be beneficial to the business.

UUP

In the context of our #LateCycle slowdown thesis on the domestic economy, our bullish bias on the dollar continues to be centered on the structural divergence in G-3 monetary policy.

Specifically, with the Fed allegedly gearing up to make a policy mistake by raising rates in September (see: Atlanta Fed President Lockhart’s hawkish commentary), there exists a cavernous gap between Fed and BoJ/ECB monetary policy.

With key commodity prices taking another sharp leg down of late (e.g. the CRB Index dropped another -2% WoW and is down -8% MoM), the key development to highlight this week is the recent decline in inflation expectations globally (10Y breakevens):

- U.S.: -8bps WoW and -22bps MoM to 1.66%

- Japan: -1bps Wow and +1bps MoM to 0.95%

- Germany: -10bps Wow and -14bps MoM to 1.11%

- France: -10bps WoW and -18bps MoM to 1.20%

- Italy: -6bps WoW and -10bps MoM to 0.96%

- Spain: -6bps Wow and -12bps MoM to 0.96%

Going back to the policy divergence theme, it’s worth highlighting that the Fed is substantially closer to achieving its +2% inflation target than either the BoJ or ECB are to achieving theirs, which implies considerable scope for the BoJ’s QQE program and the ECB’s QE program – which remain ongoing, targeting LSAP of ¥80T/yr and €60B/mo, respectively – amid the Fed’s rhetorically hawkish bias (misguided as it may be).

From the perspective of foreign exchange market participants, the U.S. remains the “best house in a bad neighborhood” and we remain bullish on the U.S. dollar (UUP) as a result.

TLT | VNQ | EDV | XLU

Please note we added XLU (Utilities Select Sector SPDR Fund) to Investing Ideas on Thursday to read the full Stock Report click here.

Sometimes the macro rotation and allocation playbook is relatively straightforward. As growth slows and "reflation" deflates, you want to be buying A) Long-term Bonds and B) stocks that look like bonds. Bond proxies and defensive yield consistently outperform alongside the dual deceleration in demand and prices and Utilities and REITS remain the go-to sectors for growth slowing, defensive yield exposure.