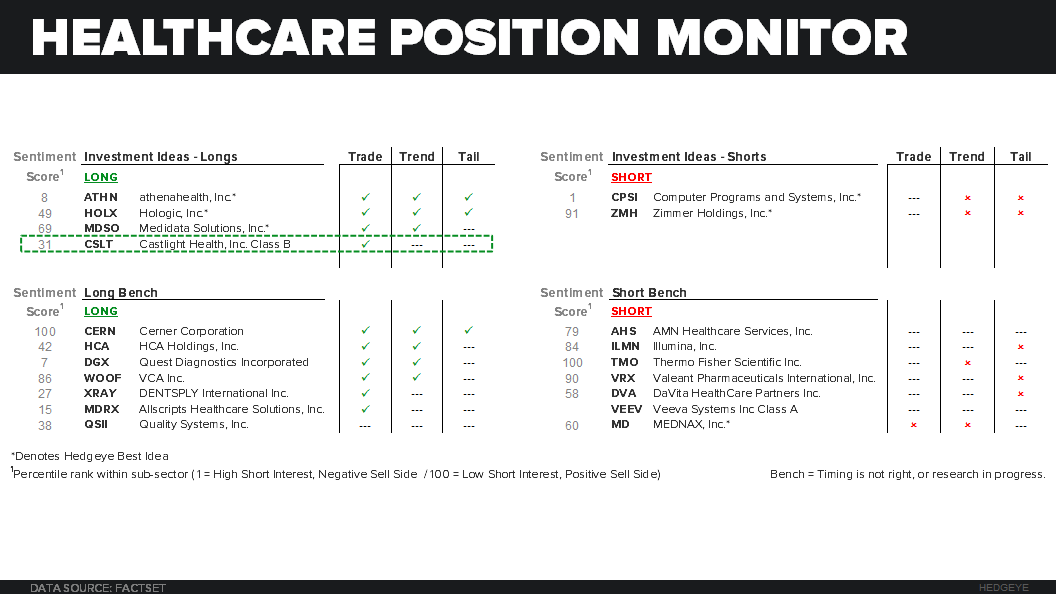

We added CSLT to our Investment Ideas list as Long earlier in the week (Click Here for Note) based on the steep valuation discount to its forward growth rate and data sharing agreement with UNH setting stage for strong bookings growth in the back half of 2015.

OVERVIEW

Castlight Health (CSLT) reported Q2 2015 sales of $18.5 mill, beating consensus estimates of $17.8 mill. Guidance for 3Q15 of 19.2-$19.5 mill (19.8 mill consensus) was a bit soft due to the implementation timing of sales to existing customers, which comprised a larger than expected portion of 1H15 bookings. For the full year 2015, management stated they are on track to hit the mid point of their initial 2015 revenue guidance range of $74-77 mill. With respect to profitability, subscription sales gross margin was 83.0% in 2Q15, a significant improvement compared to 69.6% in 2Q14, and supportive of management's long-term total gross margin guidance of 70-75%.

The guidance looks low, given the pattern of beats in recent quarters and our model. Based on the short interest at 31% and deeply discounted valuation, meeting or slightly beating estimates should translate as a significant positive.

bookings

On the new business front, CSLT's 2015 bookings year-to-date have come from cross-sells, which is a positive reflection of the company's R&D efforts. 25% of customers have purchased at least 3 products, with a few signing on for 4 to 5 products. The company only signed 7 net new customers in the quarter (down from 16 customers signed in 2Q14), bringing total customers signed to 181. Helping offset lower customer adds is a larger average deal size, with the company signing 3 Fortune 500 companies in the quarter.

We attribute the year-over-year decline in net customer wins to sales force disruptions as part of a broader reorganization effort that started at the beginning of the year. However, we continue to believe that the UNH data sharing agreement sets them up nicely for net new customer wins in the seasonally strong back-half of the year.

On the margin, management commentary on the sales effort sounded sequentially more positive on the 2Q15 call, in our view.

"Clearly on the new logo front, we saw less new logo addition than we were looking for in the first half of the year but not totally unexpected given the transition of the sales force, and we're really looking to the third quarter to accelerate customer adds and new logos. And we think we're in a good position to do that." - CFO Q3 Earnings Call

conclusion

Overall, it was a forgettable quarter with no big surprises. Attention will now turn to 3Q15, as it is typically the strongest quarter for net new customer wins. CSLT's success in driving new bookings growth for the remainder of the year will depend on how quickly they can get trained reps out in the field and how effectively they manage the sales force transition from here. With the stock trading at 46% discount to its sales growth rate relative to peers and 31% short interest, the hurdle is low and appears beatable. In the short term, we are willing to look past some of the weakness and instead focus on the long-term growth opportunity ahead.

Please call or e-mail with any questions.

Thomas Tobin

Managing Director

@HedgeyeHC

Andrew Freedman

Analyst

@HedgeyeHIT