“The credit belongs to the man who is actually in the arena…”

-Teddy Roosevelt

After all, it is we, the men and women of the Global Macro gridiron, “who strive valiantly; who errs, and comes short again and again, because there is no effort without error or shortcoming”…

We might not get everything right. But we tend to not implode on the big risks when consensus does.. and, at a bare minimum, our place on Wall Street “will never be with those cold and timid souls who know neither victory nor defeat.”

Back to the Global Macro Grind…

Yep. That’ll fire me up on any Monday morning – never mind one in the arena of August heat. Your summer has been a relatively victorious one if you stayed clear of what many hoped was a “reflation” TRADE morphing into a legitimate TREND.

Here’s last week’s Currency/Commodity score, with a 3-month overlay to contextualize it:

- US Dollar Index flat week-over-week and +2.7% in the last 3 months

- Euro (vs. USD) flat week-over-week and -2.1% in the last 3 months

- Japanese Yen -0.1% week-over-week and -3.6% in the last 3 months

- Canadian Dollar -0.3% week-over-week and -7.7% in the last 3 months

- Russian Ruble -5.3% week-over-week and -16.3% in the last 3 months

- CRB Commodities Index -1.2% last week and -11.7% in the last 3 months

- Oil (WTI) -2.6% last week and -24.1% in the last 3 months

- Gold +0.8% last week and -7.6% in the last 3 months

- Copper -1.2% last week and -18.5% in the last 3 months

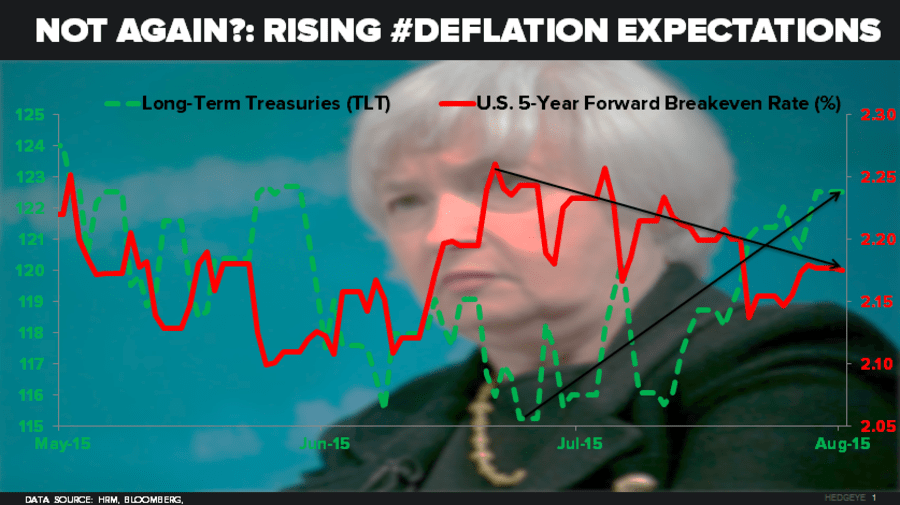

- 5yr UST Break-evens -3bps wk-over-wk to 1.40% (-38 bps in the last 3 months)

I know. Break-evens aren’t currencies or commodities, but since I like to play dirty sometimes I thought I’d slip that in there (mainly because that macro read-through on inflation expectations is highly instructed by FX and Commodity deflations).

The read-through to Global Equity markets was dominated by rising #Deflation expectations too:

- US Energy Sector (XLE) was the only one to close down wk-over-wk and is -16.1% in the last 3 months

- Emerging Markets (MSCI) and EM LATAM (MSCI) deflated another -1.8% and -0.7%, respectively

- Russian Stocks (RTSI) carried XLE-like negative alpha wk-over-wk (again) and are -16.6% in the last 3 months

Fortunately, I think the Fed gets this. That’s why the #1 change in their language last week was their concern on losing their almighty illusion of growth (inflated asset prices). That’s mainly why the doves took home the Low-Beta cake staying with the Long Bond too.

For those of you who took advantage of the correction in both Long-term Treasuries (TLT) and US Equities that look like bonds, well done. Oh my face was “marred by dust and sweat” (no blood) on that front. And I’m damn proud we stuck with the #process too.

Utilities (XLU) ripped higher into Friday’s month-end markup, taking their July absolute and relative gain vs. Energy (XLE) to:

- Utilities (XLU) +6.10%

- Energy (XLE) -7.69%

So, in terms of what happens next, this week’s US jobs report (Friday) should matter to what’s been working for the last week and month. Consensus is still looking for another > 225,000 (only because estimates anchor on what happened last time).

While the rate of change in Non-Farm Payroll gains has been slowing since FEB, pro-cyclical economists haven’t had to react to jobs prints that have looked as nasty as Texan deflation has. Alas, this is a cycle – give it time…

Away from capitalizing on #Deflation what else continued to work both last week and in July? From a Macro Style Factor perspective:

- BETA: Low-Beta was up another +1.9% last week (vs. the Dow +0.7% and SP500 +1.2%) and was +3.2% for July

- SIZE: Large-Cap was up another +1.5% last week and was +1.9% for July

- SHORT INTEREST: Low-Short-Interest was +1.3% wk-over-wk and +2.0% for July

In other words, if you were long something boring with non-cyclical cash flow, low-short-interest (2%), and a big market cap ($35B) like General Mills (GIS), you were up +1.9% on that in July. That’s not flashy, but it helped us achieve the goal – victory in the arena.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.18-2.28%

SPX 2067-2130

VIX 11.89-14.31

USD 96.58-97.96

EUR/USD 1.08-1.10

Oil (WTI) 46.05-48.69

Best of luck out there today,

KM