Key Takeaway:

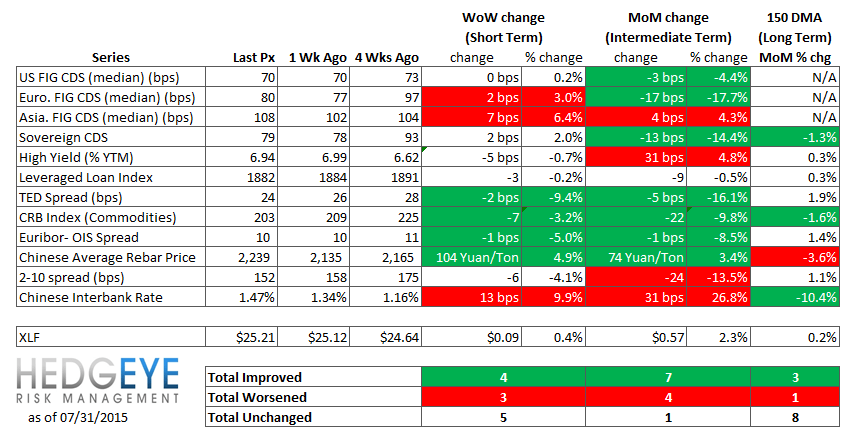

Our focus of late has been on China and the US high yield market. Last week saw both those areas put in small, counter-trend rallies. High yield backed off slightly last week, falling 5 bps to 6.94%. Meanwhile, China saw steel prices and soverign swaps both decline, albeit small. Our bearish view on both remains unchanged.

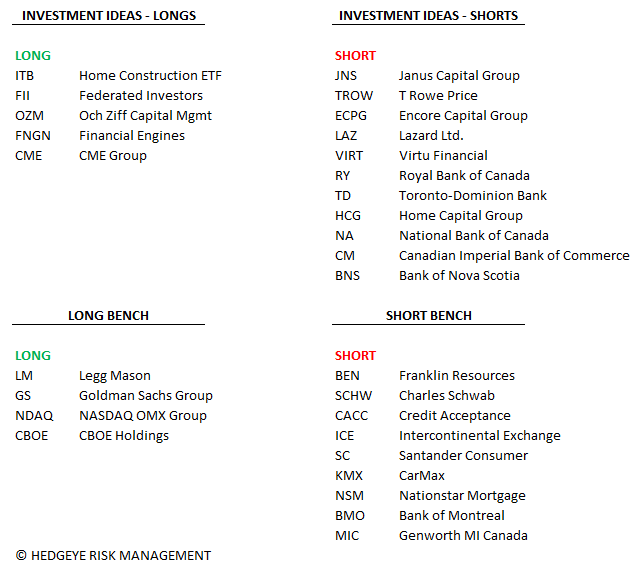

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 4 of 12 improved / 3 out of 12 worsened / 5 of 12 unchanged

• Intermediate-term(WoW): Positive / 7 of 12 improved / 4 out of 12 worsened / 1 of 12 unchanged

• Long-term(WoW): Positive / 3 of 12 improved / 1 out of 12 worsened / 8 of 12 unchanged

1. U.S. Financial CDS - Swaps tightened for 12 out of 27 domestic financial institutions. With the second quarter GDP reading coming in at 2.3%, within the range of economist estimates, and the Federal Reserve keeping interest rates near zero, swaps were unchanged at the median.

Tightened the most WoW: AXP, ACE, GS

Widened the most WoW: CB, MBI, GNW

Tightened the most WoW: ACE, ALL, AIG

Widened the most/ tightened the least MoM: MMC, MBI, SLM

2. European Financial CDS - Swaps mostly widened in Europe last week as Eurozone inflation was shown to be a minimal 0.2% in July and Eurostat reported increased unemployment in the region on Friday. After not trading for a number of weeks, swaps for Russia's Sberbank traded at +70 bps higher than their last mark given the Bank of Russia's cutting interest rates for the fifth time this year and citing economic risks.

3. Asian Financial CDS - Chinese banks saw their swaps widen by +2 bps to +7 bps on the week. Meanwhile, the Japanese and Indian banking complexes were generally flat to tighter.

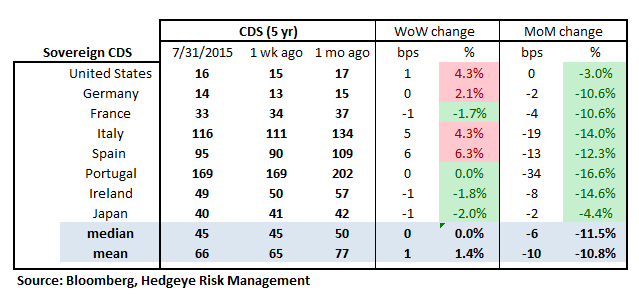

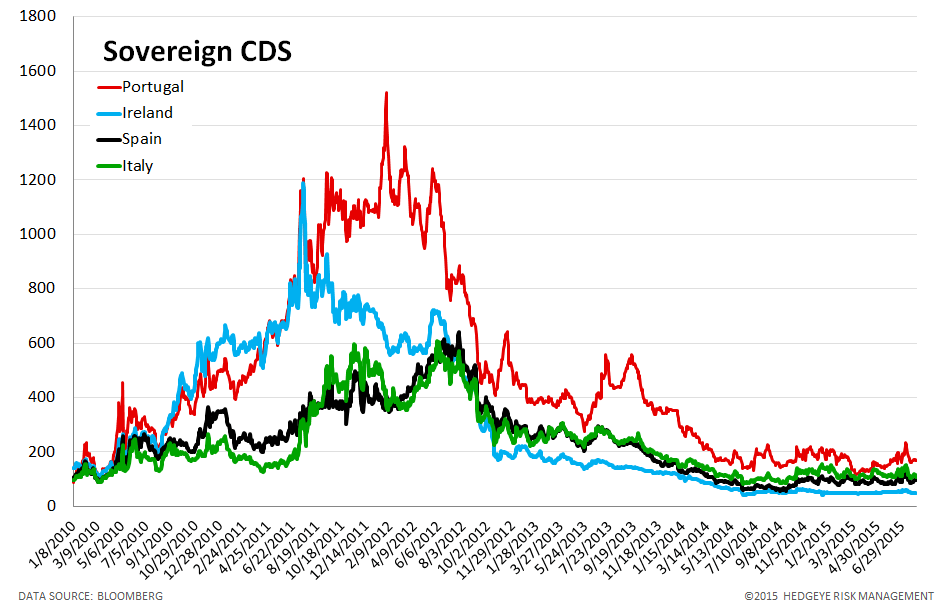

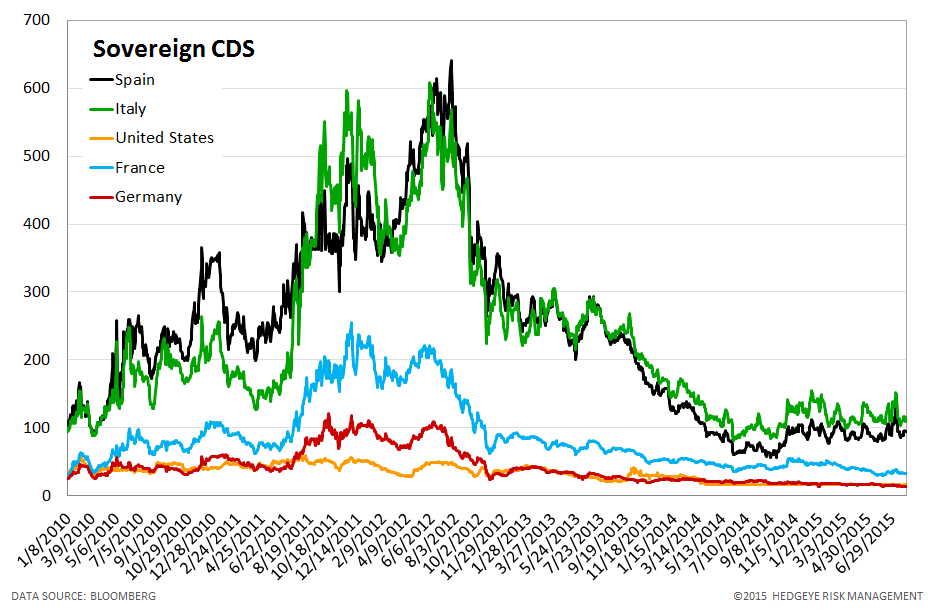

4. Sovereign CDS – Sovereign swaps mostly widened over last week. Spanish sovereign swaps widened the most, +6 bps to 95, followed by Italy, which widened +5 bps to 116.

5. Emerging Market Sovereign CDS – Emerging market swaps mostly widened last week. Turkish sovereign swaps widened by +11 bps to 236 while on the opposite end of the spectrum Mexican swaps tightened by -4 bps to 136.

6. High Yield (YTM) Monitor – High Yield rates fell 5 bps last week, ending the week at 6.94% versus 6.99% the prior week.

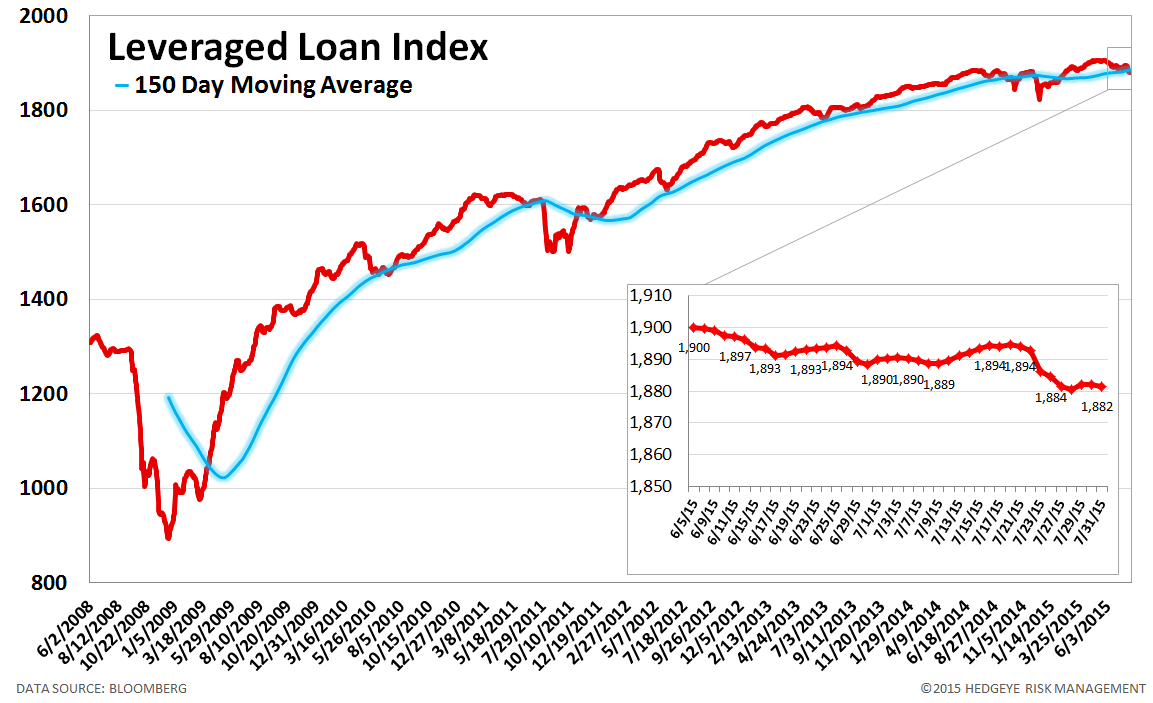

7. Leveraged Loan Index Monitor – The Leveraged Loan Index fell 2.0 points last week, ending at 1882.

8. TED Spread Monitor – The TED spread fell 2 basis points last week, ending the week at 24 bps this week versus last week’s print of 26 bps.

9. CRB Commodity Price Index – The CRB index fell -3.2%, ending the week at 203 versus 209 the prior week. As compared with the prior month, commodity prices have decreased -9.8%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

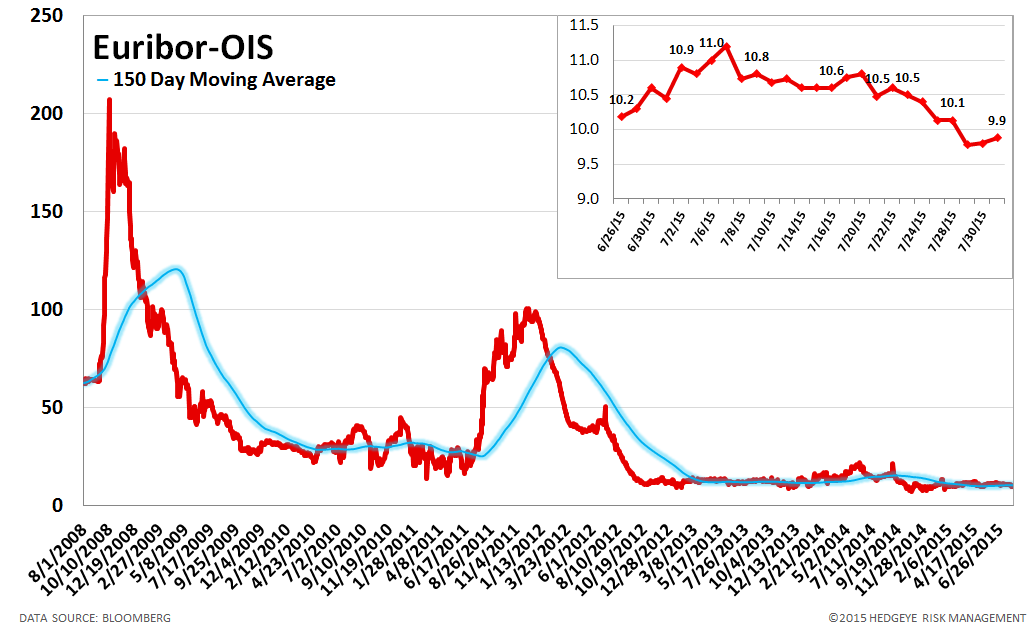

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by 1 bps to 10 bps.

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose 13 basis points last week, ending the week at 1.47% versus last week’s print of 1.34%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

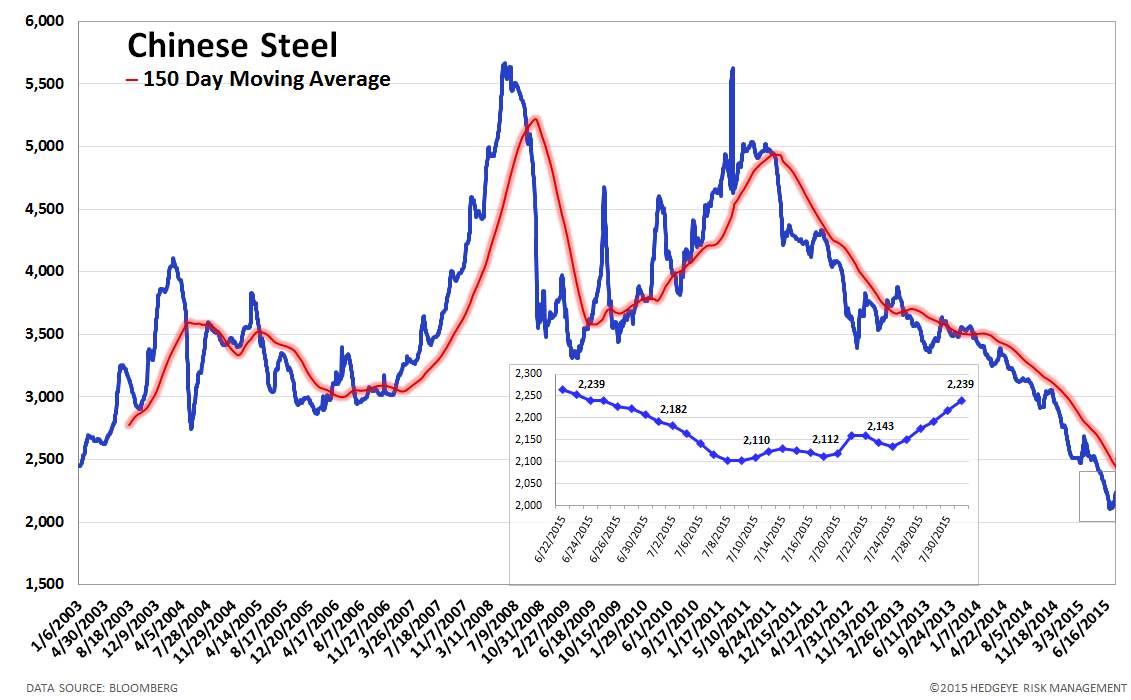

12. Chinese Steel – Steel prices in China rose 4.9% last week, or 104 yuan/ton, to 2239 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread tightened to 152 bps, -6 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 1.6% upside to TRADE resistance and -1.8% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT