overview

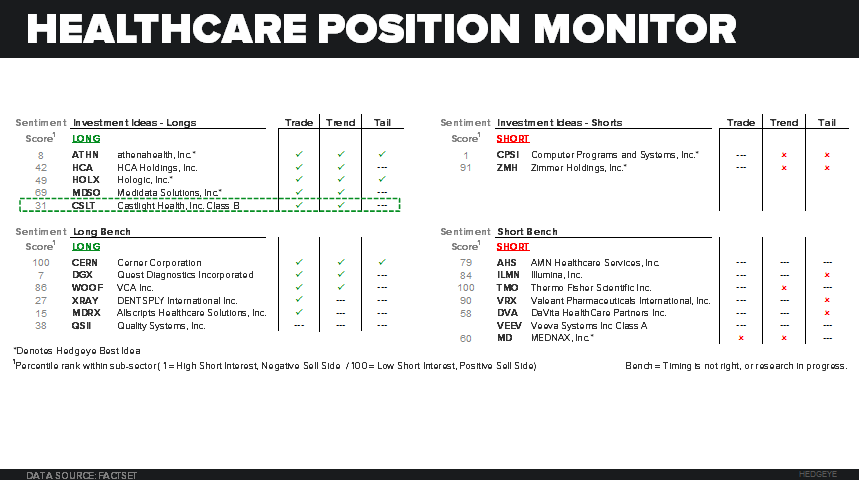

We are elevating Castlight Health (CSLT) from our long bench to our Investment Ideas List as a Long ahead of earnings on 8/5. We are not expecting any surprises going into the quarter, with consensus sales estimate of $17.8 mill in-line with our model. However, at 4.9x NTM EV/Sales, the stock trades at a steep discount to its growth rate relative to peers, implying only 18% sales growth for 2016. This compares to the 68% sales growth the company is on track for in 2015, and significantly below our 2016 estimate for +50% growth. Further, we expect the data sharing agreement with UNH to set the stage for strong bookings growth into the seasonally strong back half of the year. CSLT fits well within our theme of Healthcare Deflation and we can see +40% upside based on our growth estimates over next 12-months.

background

CSLT provides participants in self-insured health plans the ability to shop for healthcare using Castlight's cloud-based suite of products. The company is at the interchange between the employer, employee and managed care organization, aggregating data and providing analytics to help support the Enterprise. Their offering is built on price transparency and cost savings, which fits well into our Healthcare Deflation Theme.

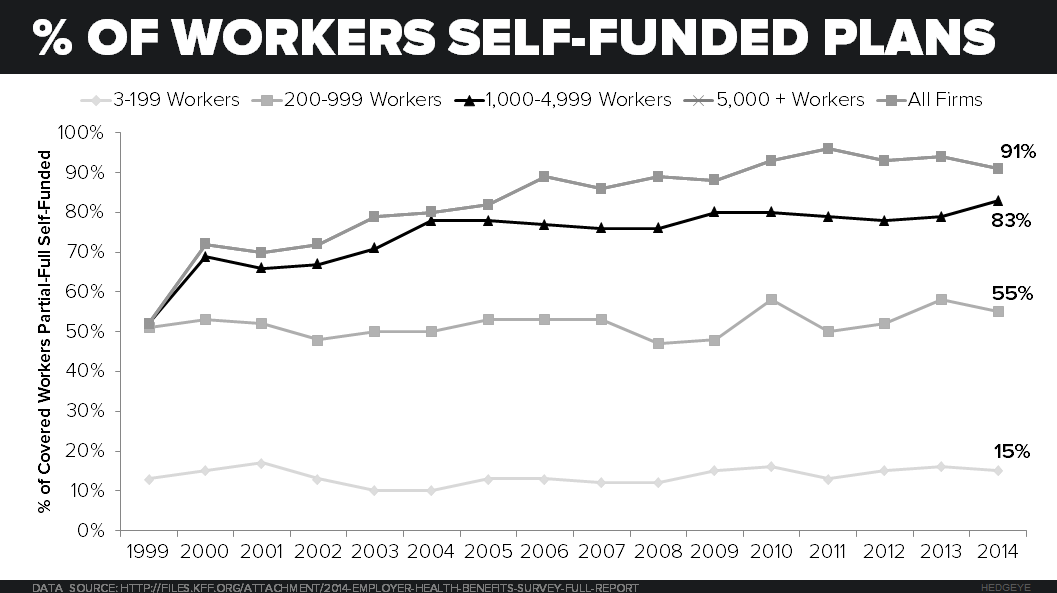

55% of covered workers in the United States are part of an employer self-insured health plan. In attempt to control rising costs, employers have shifted more of the premium expense onto the employee whether through Consumer Direct Health Plans (CDHP) or outright increase in annual contributions. Castlight is well positioned to capitalize on this trend as employers look for tools to reduce health costs and employees facing greater out-of-pocket expense begin to frame consumption decisions around value.

Castlight's value proposition comes in three major forms:

- Cost Savings to the Employee - Increase in high deductible plans and excessive premium growth continues to put pressure on consumers of healthcare. Castlight provides a platform for price transparency and quality information, which allows employees to frame medical consumption decisions around value.

- Cost Savings to the Employer - For self-insured employer health plans, cost savings to the consumer is cost savings to the employer. Castlight also provides educational tools to help avoid unnecessary visits to high cost care settings such as the E.R.

- Employer Control/Access to Information - Castlight provides employers with a dashboard and control system to monitor healthcare spending, identify areas of cost savings and implement employee benefit plans.

show me the data

Castlight relies on access to claims data from managed care companies for their pricing information. With every new data sharing agreement, the company has to build out the infrastructure to get access to this information. The last major hurdle the company faced was getting access to UNH's network, which they did earlier in 2015. Prior to that, the company was unable to target the customers of the largest managed care organization in the United States. We believe this will provide a nice tailwind to new bookings growth as we enter the seasonally strong back half of the year.

valuation

Castlight went public in March 2014 at an offering price of $16/share. The stock jumped +150% out of the gate, and at a price in the low $40s, was trading over 100x NTM EV/Sales. Since then, we have watched shares come down to earth and stabilize in the $7-9 range or 5-7x NTM EV/Sales. Short interest is currently 30%, and has been relatively stable over the last year (~9-10 mill shares sold short) when compared against fully adjusted available float (~30 mill shares).

Unlike many recent IPOs, Castlight is an early stage growth company working off small revenue base of $75 mill (2015 estimate). This provides a rare opportunity to get in on the ground floor of what is likely to be a multi-year growth story. We expect the company to grow sales by +50% in 2016, on top of the +68% revenue growth in 2015.

At 4.9x NTM EV/Sales, the company trades at a -46% discount to its sales growth rate relative peers. While it can be argued that the discount is deserved given the company's immature and unprofitable status, we believe it also represents an attractive margin of safety.

conclusion

Castlight Health fits well within our theme of Healthcare Deflation and we can see +40% upside based on our growth estimates over the next 12-months. At the same time, we recognize the risks embedded in the position given its small size ($658 mill market cap), short history as a public company (~1.5 years) and high short interest (+30%). We would also disclose that we don't have the same type of visibility as we do with our other top long ideas (HOLX, ATHN, MDSO), but we will be expanding our knowledge base as we continue to focus more intently on the name. However, we believe the risk/reward is in our favor given the valuation discount and data sharing agreement with UNH that sets the stage for strong bookings growth in the back half of 2015.

-------

Please call or e-mail with any questions.

Thomas Tobin

Managing Director

@HedgeyeHC

Andrew Freedman

Analyst

@HedgeyeHIT