KEY POINTS

- 2Q15 = INORGANIC CLOUDS: LNKD handily beat 2Q15 estimates, which were depressed by its low-balled 2Q15 guidance. But what looked like a massive beat was partly fueled by inorganic revenues that mgmt didn’t properly guide to ($18M vs. $3M guidance), with $15M of its $32M revenue beat coming from Lynda. Still, organic trends remain solid, with Talent Solutions recovering from the account transition, and interestingly, much of its upside surprise coming from Marketing Solutions (next point).

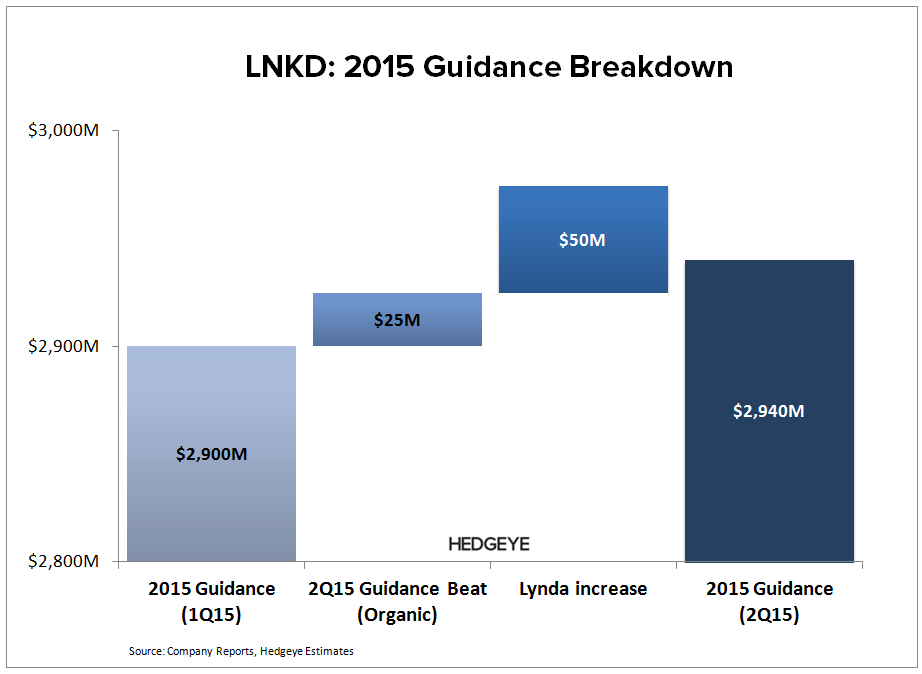

- CRYING WOLF…AGAIN: We were concerned that LNKD may guide light for 3Q, but mgmt took it one step further. LNKD raised 2015 guidance, but cut its organic guidance by ~$35M, citing pressure in its display business (Marketing Solutions). However, we estimate that display contributed roughly $48M in 1H15 revenue (based on mgmt commentary). That said, guidance now implies that display basically goes to $0 overnight, which obviously doesn't make sense, especially since display was flat q/q. In short, LNKD just wanted display revenues out of its guidance.

- BUT NOT AN EXCUSE: We do appreciate that LNKD is concerned with managing expectations, but it can’t cry wolf two quarters in a row. We can’t help but wonder if something else is going on, or LNKD is just being overly cautious. But either way, situations like this prevent the mob from chasing the print the next time around, or worse, trains the sell-side to take guidance less seriously. LNKD remains a Best Ideas Long, but we're not pounding the table since we're not sure what mgmt will do the next time it sees its shadow.

2Q15 = INORGANIC CLOUDS

LNKD handily beat 2Q15 estimates; it was actually its biggest beat since 2012. But much of that came off of depressed expectations off its low-balled 2Q15 guidance. Further, much of that beat was partly fueled by inorganic revenues that mgmt didn’t properly guide to ($18M vs. $3M guidance), with $15M of its $32M revenue beat coming from Lynda.

There was no real cause for concern in its organic trends. Our long thesis centered on its Talent Solutions segment, which came in above consensus estimates. Net LCS customer growth accelerated off a weak 1Q15 print, which suggests that the 1Q15 investment in its salesforce is starting to pay off, or at a minimum, suggests the account transition was a transitory issue.

The one blemish was the deceleration in its Talent Solution ARPA, which is what we're keying in on since this is where both the bulk of its TAM and current opportunity exists. ARPA diverged from our tracker in 2Q15, which we don't want to overreact to since it's just one quarter, but obviously something to monitor.

CRYING WOLF…AGAIN

We were concerned that LNKD may guide light for 3Q, but mgmt took it one step further. LNKD raised 2015 guidance by $40M, but actually cut its organic guidance by $35M after considering the cumulative $75M in tailwinds from its 2Q15 guidance beat and incremental revenue from its Lynda acquistion.

However, the math doesn't make sense. The $35M organic cut was due to incremental pressure around display advertising. But according to mgmt commentary, we estimate that display represented roughly $48M in 1H15 revenue. By cutting guidance by $35M against $48M in 1H revenue, mgmt is suggesting that display advertising will evaporate in the back-half, which is odd since management commentary also suggests that display remained flat q/q in 2Q15 . More likely than not, mgmt just wants display revenues out of its guidance.

BUT NOT AN EXCUSE

We do appreciate that LNKD is concerned with managing expectations, but it can’t cry wolf two quarters in a row. We can’t help but wonder if something else is going on, or LNKD is just being overly cautious.

But either way, situations like this prevent the mob from chasing the print the next time around, or worse, trains the sell-side to take guidance that less seriously. LNKD remains a Best Ideas Long, but we're not pounding the table since we're not sure what mgmt will do the next time it sees its shadow.

Let us know if you have any questions or would like to discuss further. See note below for incremental detail and analysis on our long thesis thesis.

Hesham Shaaban, CFA

@HedgeyeInternet

LNKD: New Best Idea (Long)

07/14/15 08:00 AM EDT